01/31/2020

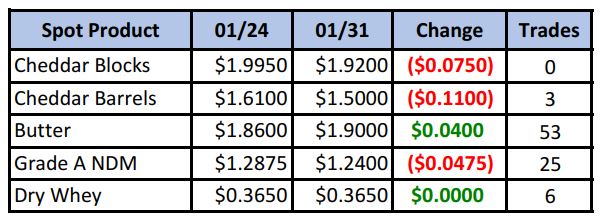

Following contra-seasonal gains last week, spot cheese was put back in its place as buyers retreated to the sidelines, allowing offers to walk prices lower all week. Just 3 loads of barrels exchanged hands while no one was willing to take on any blocks. The block/barrel spread has been pushed again to near record levels at 42¢ premium to blocks. Butter was the star this week, trading a whopping 53 loads and gaining 4 cents in the process.

Spot Market Recap

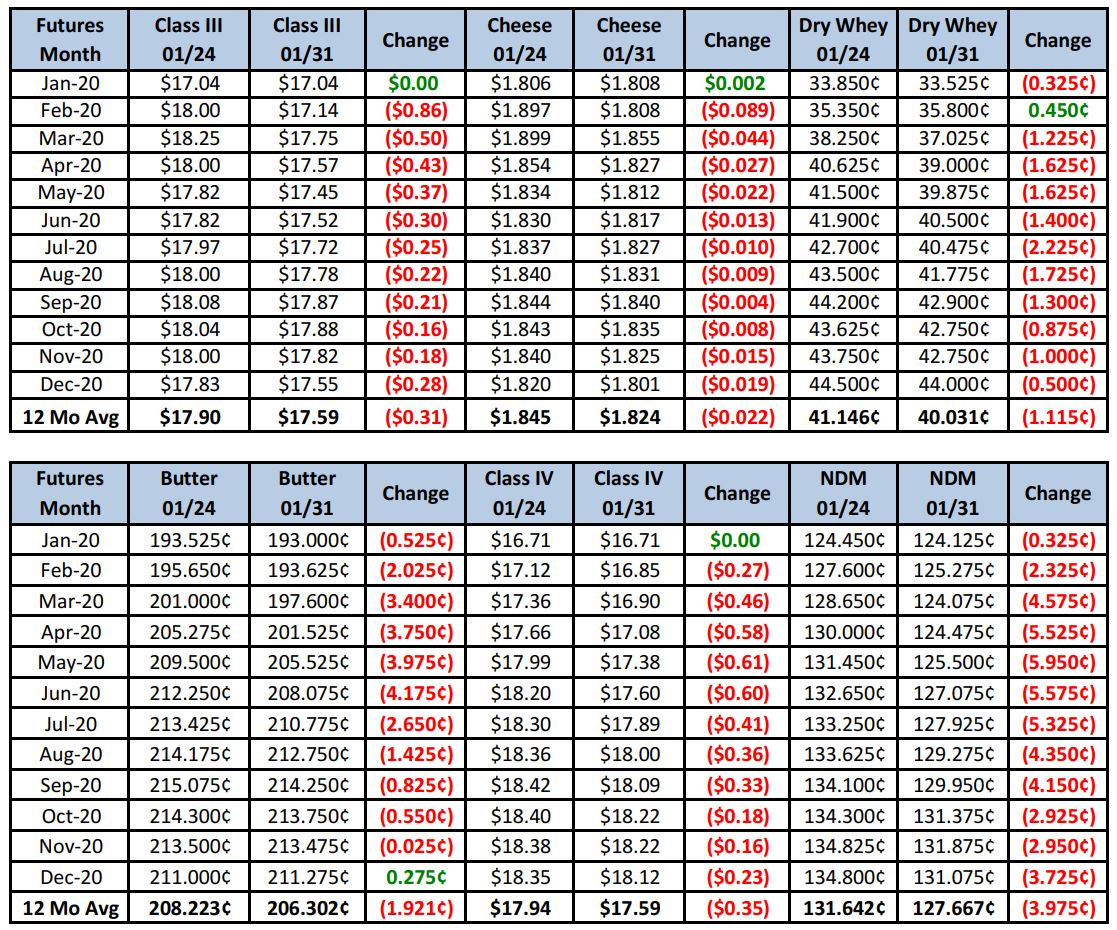

Futures Recap

After finishing the week up 57¢ last week to close at $18.00, Feb Class III futures were sucker-punched the other way this week, leading to an even larger 86¢ loss. The exponential spread of the coronavirus (see graph below) has led to concerns over what the economic impact might be. While some would rightfully point out that deaths from the common flu far outnumber those from coronavirus, the fact that cases are still growing exponentially and that China has effectively locked down 50 million people, is bound to have an effect on the global economy.

Number of Confirmed Coronavirus Cases

China passed Japan in 2010 as the second largest economy in the worlds, and by some measurements, was set to pass the U.S. as the #1 economy in 2020. The phrase, “When the U.S. sneezes, the world catches a cold”, can now be applied to any of the largest economies. The stock market this week had its worst weekly performance since September, with the Dow plunging more than 650 points at one point on Friday, with several investment firms warning that economic growth could get stalled in the first quarter. Commodities were not immune, with everything from energies, to grains, to dairy being impacted by the prospect of lowering demand. Markets often overreact, and perhaps this is one of those times. If the number of new cases begins to level off, watch for the markets to recover. If not, the current “risk off” mentality is justified.

From a fundamental standpoint, things look better than they did at this time last year. Sure, we’re heading into spring flush, but demand has held up very well post holidays. Cheese stocks at USDA-selected storage centers are down 7% (4.9 million lbs) over the period Jan 1 through Jan 27, a time when we usually start to begin building stocks. Cheese appears to be moving well, with 2020 sales off to a great start, according to some manufacturers. Indeed, a plant we spoke to this week was content to continue making higher value Italian varieties, even though the Cheddar price peaked near $2/lb. Fluid milk output is climbing across the country, but discounts in most areas range only as low as about $1.50 under class, compared to much greater discounts a year ago. Cream is abundant and butter makers are active, but the switch from old crop to new crop butter is closing and buyers were active this week in the spot market. Demand for NDM has kept inventories in check, with spring baking needs and strong sales to Mexico supporting prices.

On the international side, EU milk production in Nov was up 0.9%, but cheese stocks are reported as low, due to strong international and domestic orders. Hay and feed remain tight in Australia. Disappointing milk production has led to increased Australian demand for New Zealand cheese. Oceania cheddar averaged a US equivalent $1.85/lb this week. New Zealand milk production in December was down 0.5% by volume, though milk solids were up 0.2%. However, the incremental gains is leading to tighter SMP supplies, while concern is growing over the dry conditions currently being experienced in the country. Milk output is also declining in key dairy basins of South America. High summer temps are reducing cow comfort, while drought is diminishing pasture quality. Higher beef prices are encouraging some dairy operations to cull more aggressively, shrinking the size of the milking herd. Total milk volumes are less than adequate to meet processing needs and cream supplies are very limited.

Despite a longer term bullish view, the uncertainty in the near term is driving this sell-off, and we once again need to respect price action. With Feb Class III’s more than giving up last week’s gains, the momentum and trend is still to the downside in the near term. Hopefully many of you have already hedged Q1 and Q2 at higher prices. We would hold off selling anything July-Dec at this point. In fact, the current move lower does create an opportunity. Consider buying courage calls to make future sales. For example, the May 18.50 Call settled at 21¢. Try to buy it at 20¢ or lower, and then enter orders with your co-op/plant/broker to sell at $18.30 or higher. May settled at $17.45 today, so that’s not out of reach on a market recovery. If the market rallies much higher, you would miss out on 40¢ of upside, but would capture further gains as high as the market wanted to go. Similar strategies could be used for the surrounding months. Give us a call and we’ll help you put a strategy in place!

Have a great weekend!