03/01/2019

Futures Recap

| Futures Month | Class III 02/22 | Class III 03/01 | Change | Cheese 02/22 | Cheese 03/01 | Change | Dry Whey 02/22 | Dry Whey 03/01 | Change |

| Mar-19 | $14.90 | $15.20 | $0.30 | $1.518 | $1.560 | $0.042 | 42.250¢ | 40.425¢ | (1.83¢) |

| Apr-19 | $14.80 | $15.13 | $0.33 | $1.512 | $1.552 | $0.040 | 41.300¢ | 39.925¢ | (1.38¢) |

| May-19 | $15.08 | $15.20 | $0.12 | $1.542 | $1.560 | $0.018 | 40.300¢ | 39.800¢ | (0.50¢) |

| Jun-19 | $15.52 | $15.52 | $0.00 | $1.590 | $1.596 | $0.006 | 40.000¢ | 39.000¢ | (1.00¢) |

| Jul-19 | $16.01 | $15.98 | ($0.03) | $1.638 | $1.648 | $0.010 | 40.275¢ | 39.300¢ | (0.98¢) |

| Aug-19 | $16.21 | $16.13 | ($0.08) | $1.666 | $1.665 | ($0.001) | 40.000¢ | 39.500¢ | (0.50¢) |

| Sep-19 | $16.42 | $16.33 | ($0.09) | $1.682 | $1.680 | ($0.002) | 39.500¢ | 39.600¢ | 0.10¢ |

| Oct-19 | $16.37 | $16.30 | ($0.07) | $1.685 | $1.681 | ($0.004) | 38.750¢ | 39.325¢ | 0.58¢ |

| Nov-19 | $16.33 | $16.24 | ($0.09) | $1.680 | $1.675 | ($0.005) | 38.750¢ | 39.025¢ | 0.27¢ |

| Dec-19 | $16.15 | $16.14 | ($0.01) | $1.670 | $1.670 | $0.000 | 38.750¢ | 39.025¢ | 0.27¢ |

| Jan-20 | $15.80 | $15.85 | $0.05 | $1.655 | $1.655 | $0.000 | 37.000¢ | 37.175¢ | 0.17¢ |

| Feb-20 | $15.80 | $15.75 | ($0.05) | $1.655 | $1.658 | $0.003 | 37.000¢ | 36.750¢ | (0.25¢) |

| 12 Mo Avg | $15.78 | $15.81 | $0.03 | $1.624 | $1.633 | $0.009 | 39.490¢ | 39.071¢ | (0.42¢) |

| Futures Month | Butter 02/22 | Butter 03/01 | Change | Class IV 02/22 | Class IV 03/01 | Change | NDM 02/22 | NDM 03/01 | Change |

| Mar-19 | $227.05 | $228.00 | 0.95¢ | $15.92 | $15.86 | (0.06¢) | 98.500¢ | 97.400¢ | (1.10¢) |

| Apr-19 | $229.10 | $230.93 | 1.83¢ | $16.10 | $16.05 | (0.05¢) | 100.000¢ | 98.075¢ | (1.93¢) |

| May-19 | $229.75 | $232.13 | 2.38¢ | $16.30 | $16.24 | (0.06¢) | 102.250¢ | 100.000¢ | (2.25¢) |

| Jun-19 | $230.85 | $231.75 | 0.90¢ | $16.52 | $16.44 | (0.08¢) | 103.800¢ | 102.025¢ | (1.77¢) |

| Jul-19 | $231.60 | $232.73 | 1.13¢ | $16.68 | $16.63 | (0.05¢) | 105.775¢ | 104.100¢ | (1.68¢) |

| Aug-19 | $232.43 | $233.03 | 0.60¢ | $16.90 | $16.71 | (0.19¢) | 107.125¢ | 105.850¢ | (1.28¢) |

| Sep-19 | $233.25 | $233.03 | (0.22¢) | $17.00 | $16.77 | (0.23¢) | 108.500¢ | 107.000¢ | (1.50¢) |

| Oct-19 | $233.55 | $232.35 | (1.20¢) | $17.10 | $16.93 | (0.17¢) | 109.500¢ | 107.775¢ | (1.72¢) |

| Nov-19 | $231.60 | $231.88 | 0.28¢ | $17.05 | $16.88 | (0.17¢) | 109.750¢ | 108.500¢ | (1.25¢) |

| Dec-19 | $229.75 | $229.63 | (0.13¢) | $16.90 | $16.75 | (0.15¢) | 109.625¢ | 107.750¢ | (1.88¢) |

| Jan-20 | $222.00 | $222.00 | 0.00¢ | $16.65 | $16.65 | 0.00¢ | 109.750¢ | 109.750¢ | 0.00¢ |

| Feb-20 | $222.00 | $222.13 | 0.13¢ | $16.65 | $16.58 | (0.07¢) | 109.750¢ | 109.625¢ | (0.13¢) |

| 12 Mo Avg | $229.41 | $229.96 | 0.55¢ | $16.65 | $16.54 | (0.11¢) | 106.194¢ | 104.821¢ | (1.37¢) |

Spot Market Recap

| Spot Product | 2/22 | 3/1 | Change |

| Cheddar Blocks | $1.5950 | $1.6100 | $0.0150 |

| Cheddar Barrels | $1.4050 | $1.4100 | $0.0050 |

| Butter | $2.2600 | $2.2875 | $0.0275 |

| Grade A NDM | $0.9975 | $0.9850 | ($0.0125) |

| Dry Whey | $0.3475 | $0.3600 | $0.0125 |

Spot Market Trade Volume

Fluid Milk Output

Balancing plants in the Northeast are nearing capacity as milk production is increasing in the region. Sales for both Class I and III are relatively flat, while Class II sales are up a bit. That is leaving plenty of milk available for any manufacturing needs. Milk output is up slightly in the Mid-Atlantic, and less milk is being shipped to the Southeast. As a result, balancing plants in the region are receiving more milk. Milk production in the Southeast is relatively flat this week. Many schools are closed for spring break, so Class I sales are lower. Manufacturing plants are thus receiving more loads of milk than last week. In the Central region, milk output is about unchanged from last week. However, a growing number of Midwest cheese plants are taking fewer to no spot loads of milk as they attempt to lower cheese output and control inventory. Some milk haulers are scrambling far and wide to find a destination for their milk. Spot loads traded as low as $2 under Class this week. Late winter freezes in the southern part of the region are causing hay supplies to tighten in some parts. Cold, wet weather in California is keeping milk output flat. A mechanical failure at one processing facility resulted in some milk being dumped. In Arizona, better weather has milk output rebounding from prior weeks, while output in New Mexico is increasing seasonally. The volume of milk heading in to cheese plants is down substantially, as some manufacturers try to minimize their inventory. Milk production in the Pacific Northwest is steady to higher, and readily available for most processing needs. Cream is abundant in most of the West, to the extent that butter manufacturers do not have capacity to handle the extra loads of cream.

Butter

Cream supplies are readily accessible in the East. Spot offers abound, but demand is soft. Production is strong due to the large volumes of cream being processed. As a result, inventories are increasing. That said, manufacturers are preparing for spring holiday orders from numerous customers. Cream is also widely available in the Central region. But demand is picking up ahead of the spring holidays. Both salted and unsalted varieties are selling at premiums, and though inventories are plentiful, contacts are comfortable ahead of rising seasonal demand. Churns are full in the West, and some of stopped buying additional loads of cream due to being a capacity. Supplies are plentiful and stocks continue to increase on stable sales.

Dry Whey

The market continued to soften this week in the Eastern region. Spot loads are trading at lower prices than a week ago, but buyers have yet to return to the market. Both output and inventory remain stable, but spot loads from other regions are competing on price. The Central dry whey market is mixed, with some preferred whey trading in the $0.40’s, while interchangeable whey is offered in the mid-$0.30’s. Cheese output has slowed as managers try to control inventory, but dry whey is still available. Some contacts feel prices are near the bottom and getting ready to rebound. In the West, some industry contacts report dry whey production has picked up and inventories are robust. Contracted whey continues to move well, but concerns remain over trade issues and African swine fever, which would continue to put a drag on demand.

Nonfat Dry Milk

Cheese

Cheese plants in the Northeast are taking in heavy milk volumes as production in the region continues to climb. Manufacturers are running on heavy schedules, keeping inventories steady to building. A growing number of cheese plants in the Midwest are reporting a seasonal slowdown in demand. As such, some are attempting to slow production down in order to manage inventories, which remain long. Few if any manufacturers are buying spot loads of milk, and some barrel producers are trying to sell extra loads of milk back in to the sport market. Prices for spot loads of milk traded as low as $2 under class. In the West, cheese output is at or near capacity. In order to control inventories, some manufacturers are putting more cheese into aging programs, while others divert more milk into barrels. Inventories remain heavy and demand is described as “mixed”. Current contracts are moving well, but any extra business is hard to find, though there are reports of a few export channels showing strength.

International

Spot cheese demand in Germany is rarely filled, due to limited stocks. A number of manufacturers have had to draw down aging programs to keep up with commitments. Cheese output is steady, but the combination of strong domestic demand and export interest is putting upward pressure on prices. Sellers are negotiating higher premiums for future contract orders. Butter, on the other hand, is seeing weaker prices. Many potential buyers are comfortably covered, so are taking a wait and see approach to buying. Both the dry whey and SMP markets in the EU are steady this week, as supply and demand are in balance. However, export interest for SMP is growing, with the strongest interest from Asia, the Middle East and North African countries.

Moving to Oceania, Australian dairy producers continue to shrink their herd size in order to deal with a water shortage and extreme heat. July-Dec milk output fell 5.1% vs. 2017. Financial stress is resulting in less purchased feed, continued herd reductions and less milk produced. In contrast, New Zealand milk output in Jan jumped 8.7% vs. a year ago. Favorable weather and more output per cow account for the increase, while pay prices above break-even have producers feeling confident. Oceania cheddar prices firmed this week, driven by good demand. Buyers are becoming more earnest in finalizing contracts. This week, cheddar cheese averaged a U.S. equivalent $1.72/lb.

Commentary

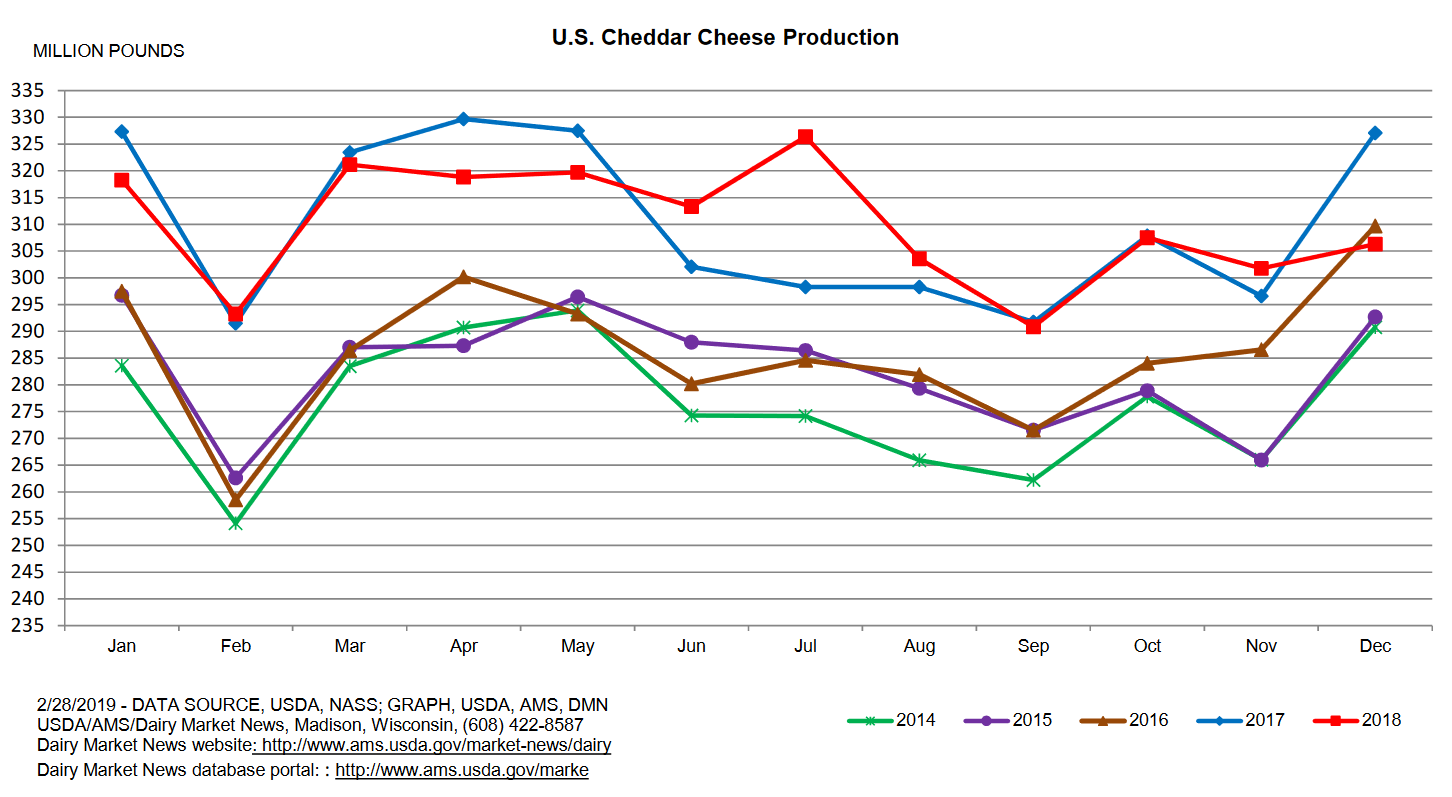

Things are falling. This week’s Dairy Products Report indicated December total cheese output declined 1.2% vs. Dec ’17, while cheddar cheese output was down an even stronger 6.3%.

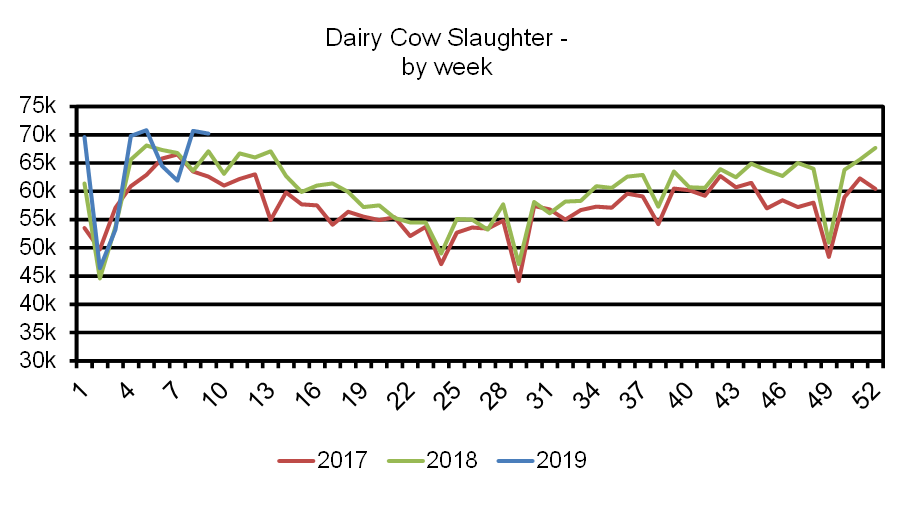

Cow numbers are continuing to fall as well, due to more aggressive culling. USDA’s most recent data showed the the last two weekly dairy cow slaughter totals at levels not seen since 2013. They averaged 7.8% higher than the same two weeks in 2018. YTD, 577,100 dairy cows have already gone to slaughter, up 19,000 head from last year.

Globally, production issues in Australia and some parts of the EU are helping put a floor under milk prices. Cheese is tight in Western Europe, cheddar prices are rising in Oceania, and powder buyers from Southeast Asia and the Middle East are getting more aggressive. The supply / demand equation IS getting rebalanced. However, we are heading in to peak production season in the U.S. Despite the loss of many dairies, especially in the Midwest, there will still be plenty of milk this spring. There’s plenty of milk now. Processors in most parts of the country are running on full schedules, cheese inventories are generally long and demand is slowing. A good many folks (including us) were scratching their heads on the most recent strength in Class III prices. Yes, a recovTery looks likely longer term, but not in the near term, as we’ve just pointed out. Our past few recommendations suggested targeting specific retracement levels on Q2 contracts. Those levels were reached, meaning, orders would have filled. Barrel sellers returned to the spot market this week, taking some of the wind out of the rally. Both NDM and dry whey sellers also unloaded a lot of product in the spot market. Class III’s initially looked like they wanted to move higher early in the week, but then began selling off. At $15.28, the Q2 average has now fallen below both retracement levels we suggested as targets.

That’s not to say next week it couldn’t rally again and make a new swing high, but the momentum is now heading down. Our best guess would suggest the milk market will make another run lower as supplies overrun demand heading into and through spring flush, followed by a reversal towards stronger prices heading into the second half of the year. Producers should consider additional sales of Q2 milk on any price strength. Have a great weekend!