02/22/2019

Futures Recap

| Futures Month | Class III 02/15 | Class III 02/22 | Change | Cheese 02/15 | Cheese 02/22 | Change | Dry Whey 02/15 | Dry Whey 02/22 | Change |

| Feb-19 | $13.97 | $13.95 | ($0.02) | $1.400 | $1.397 | ($0.003) | 46.000¢ | 45.900¢ | (0.10¢) |

| Mar-19 | $14.53 | $14.90 | $0.37 | $1.484 | $1.518 | $0.034 | 41.375¢ | 42.250¢ | 0.88¢ |

| Apr-19 | $14.43 | $14.80 | $0.37 | $1.485 | $1.512 | $0.027 | 38.825¢ | 41.300¢ | 2.47¢ |

| May-19 | $14.80 | $15.08 | $0.28 | $1.528 | $1.542 | $0.014 | 38.375¢ | 40.300¢ | 1.93¢ |

| Jun-19 | $15.30 | $15.52 | $0.22 | $1.582 | $1.590 | $0.008 | 37.775¢ | 40.000¢ | 2.23¢ |

| Jul-19 | $15.78 | $16.01 | $0.23 | $1.628 | $1.638 | $0.010 | 38.000¢ | 40.275¢ | 2.28¢ |

| Aug-19 | $16.05 | $16.21 | $0.16 | $1.660 | $1.666 | $0.006 | 38.400¢ | 40.000¢ | 1.60¢ |

| Sep-19 | $16.32 | $16.42 | $0.10 | $1.682 | $1.682 | $0.000 | 38.750¢ | 39.500¢ | 0.75¢ |

| Oct-19 | $16.26 | $16.37 | $0.11 | $1.683 | $1.685 | $0.002 | 38.400¢ | 38.750¢ | 0.35¢ |

| Nov-19 | $16.23 | $16.33 | $0.10 | $1.683 | $1.680 | ($0.003) | 38.000¢ | 38.750¢ | 0.75¢ |

| Dec-19 | $16.06 | $16.15 | $0.09 | $1.672 | $1.670 | ($0.002) | 38.000¢ | 38.750¢ | 0.75¢ |

| Jan-20 | $15.81 | $15.80 | ($0.01) | $1.655 | $1.655 | $0.000 | 37.000¢ | 37.000¢ | 0.00¢ |

| 12 Mo Avg | $15.46 | $15.63 | $0.17 | $1.595 | $1.603 | $0.008 | 39.075¢ | 40.231¢ | 1.16¢ |

| Futures Month | Butter 02/15 | Butter 02/22 | Change | Class IV 02/15 | Class IV 02/22 | Change | NDM 02/15 | NDM 02/22 | Change |

| Feb-19 | 226.00¢ | 226.13¢ | 0.13¢ | $15.85 | $15.85 | 0.00¢ | 98.250¢ | 98.250¢ | 0.00¢ |

| Mar-19 | 225.98¢ | 227.05¢ | 1.08¢ | $15.80 | $15.92 | 0.12¢ | 98.225¢ | 98.500¢ | 0.28¢ |

| Apr-19 | 227.50¢ | 229.10¢ | 1.60¢ | $15.99 | $16.10 | 0.11¢ | 99.025¢ | 100.000¢ | 0.97¢ |

| May-19 | 227.50¢ | 229.75¢ | 2.25¢ | $16.13 | $16.30 | 0.17¢ | 101.050¢ | 102.250¢ | 1.20¢ |

| Jun-19 | 229.68¢ | 230.85¢ | 1.17¢ | $16.43 | $16.52 | 0.09¢ | 102.525¢ | 103.800¢ | 1.27¢ |

| Jul-19 | 230.45¢ | 231.60¢ | 1.15¢ | $16.62 | $16.68 | 0.06¢ | 104.000¢ | 105.775¢ | 1.78¢ |

| Aug-19 | 231.53¢ | 232.43¢ | 0.90¢ | $16.83 | $16.90 | 0.07¢ | 105.800¢ | 107.125¢ | 1.33¢ |

| Sep-19 | 232.55¢ | 233.25¢ | 0.70¢ | $16.90 | $17.00 | 0.10¢ | 106.525¢ | 108.500¢ | 1.97¢ |

| Oct-19 | 232.03¢ | 233.55¢ | 1.53¢ | $16.90 | $17.10 | 0.20¢ | 107.900¢ | 109.500¢ | 1.60¢ |

| Nov-19 | 231.40¢ | 231.60¢ | 0.20¢ | $16.90 | $17.05 | 0.15¢ | 108.125¢ | 109.750¢ | 1.63¢ |

| Dec-19 | 229.75¢ | 229.75¢ | 0.00¢ | $16.78 | $16.90 | 0.12¢ | 108.475¢ | 109.625¢ | 1.15¢ |

| Jan-20 | 222.00¢ | 222.00¢ | 0.00¢ | $16.50 | $16.65 | 0.15¢ | 108.950¢ | 109.750¢ | 0.80¢ |

| 12 Mo Avg | 228.86¢ | 229.75¢ | 0.89¢ | $16.47 | $16.58 | 0.11¢ | 104.071¢ | 105.235¢ | 1.16¢ |

Spot Market Recap

| Spot Product | 2/15 | 2/22 | Change |

| Cheddar Blocks | $1.5800 | $1.5950 | $0.0150 |

| Cheddar Barrels | $1.4350 | $1.4050 | ($0.0300) |

| Butter | $2.2500 | $2.2600 | $0.0100 |

| Grade A NDM | $0.9875 | $0.9975 | $0.0100 |

| Dry Whey | $0.3525 | $0.3475 | ($0.0050) |

Spot Market Trade Volume

Fluid Milk Output

Northeast milk production is picking up in some areas, despite snowy and icy conditions. Milk is readily available, allowing manufacturers to run on full schedules. Milk output in the Mid-Atlantic is rising slightly, but balancing plants still have available capacity. Southeast milk output is moving up as well. Overall, Class I sales are lower than last week, so more milk is moving into manufacturing. In Florida, output is leveling off. Cream supplies are abundant in the region due to heavy milk volumes. Central milk and cream volumes are nudging higher, while Class I demand is lackluster. Thus, spot loads of milk are available, usually at a discount. The situation may be changing, however. Cheesemakers in the Midwest report a number of smaller dairies are set to close once their feed rations are gone. Milk output remains strong in California, keeping balancing schedules full. Fluid demand is stable there and in Arizona, where milk output is near seasonal expectations. To handle the milk, processors are running at full capacity. In New Mexico production is steady, but more milk is being turned into cheese as Class II interest has declined a bit. Excess loads of milk are being shipped around to plants that can take on extra loads. The Pacific Northwest got hit by larger winter storms last week, but things are getting back to normal. There is plenty of milk available, so many facilities are running at or near full capacity. Due to low cull cow prices, some farmers are choosing to hang onto cows.

Butter

Cream is readily available across the U.S., thus churning remains active in all regions. Inventories are building, with much being put away for use this summer. Demand is described as fair to good.

Dry Whey

Supplies loosened up a bit in the Eastern region this week. Despite prices trending lower, some buyers are hoping for further declines before making purchases. International demand has slowed a bit as well, causing some concern. Central dry whey prices drifted lower this week, despite spot availability being tight. Some suggest slower exports are to blame. Western dry prices held steady this week on mixed demand reports. Shoppers are price-sensitive in a situation where stocks are generally available.

Nonfat Dry Milk

Cheese

With milk production picking up in the Northeast, cheese makers are busy clearing all the milk they need to run full production schedules. Inventories are stable to growing, though a few operations report lower supplies. Some Midwestern plants report solid demand for pizza varieties, while curd and barrel producers are hoping for a summer demand bump before spring, when milk output will be at its peak. Cheese plants in rural areas are expressing more concern over smaller dairies calling it quits, and how that might affect their long-term milk supply. Demand is mixed in the West as well. Domestic demand is strong, as are sales to some parts ofthe Middle East. But any new business has been hard to get, and the strong milk supply is keeping vats running at or near full capacity.

International

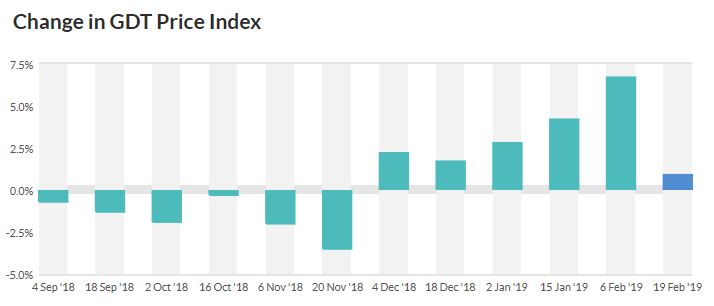

This week’s GDT auction saw the Dairy Price Index rise 0.9%. That’s the smallest increase in the last seven events, but it’s still positive!

Source: Global Dairy Trade

Commentary

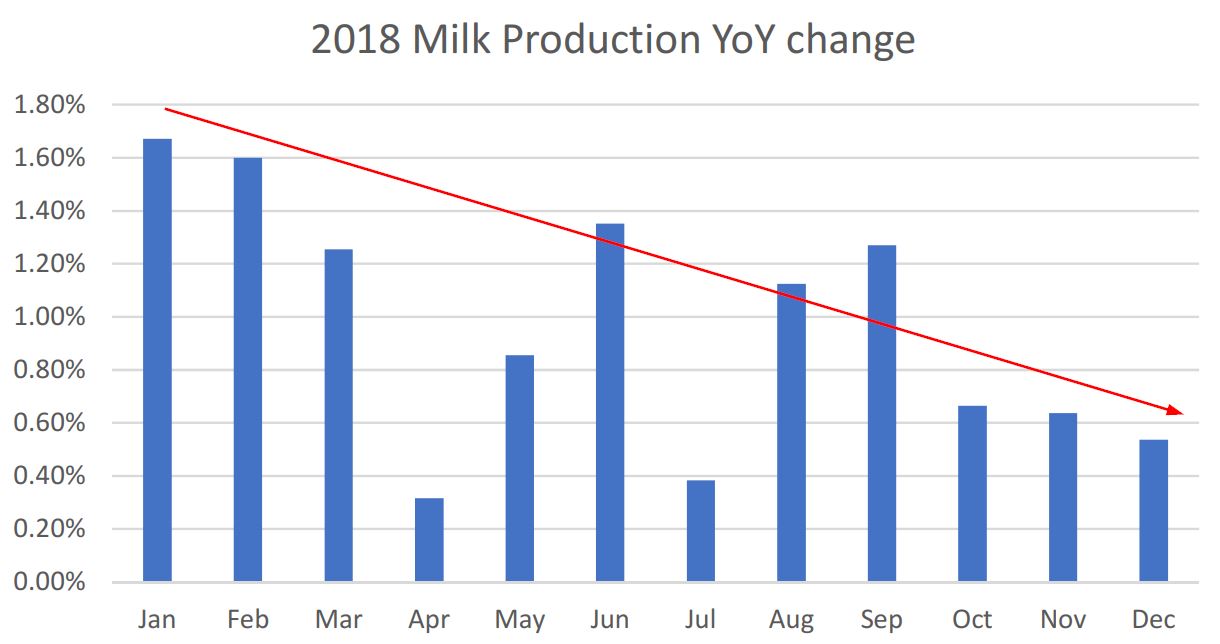

Class III futures rebounded sharply up front as spot cheese prices basically held steady (blocks up slightly, barrels down a bit). Bidders picked up 23 loads of barrels, while only 3 loads of blocks shook loose. That would seem to indicate that the fresh block supply is in a little more of a balanced situation, with sellers happier to hang on to what they have, or at least reluctant to sell. Then it all came down to math. With the March contract wrapping up it’s first pricing week, settling at $14.90, current spot prices (using Mar dry whey futures) work out to about the same $14.90 level. But that means March Class III is still trading at a discount, due to the 30-50¢ premium we’ve been seeing once the positive basis from the weekly NDPSR is factored in. It seems contrary to logic that we would rally much further from here, just as we face peak output season across the U.S., but perhaps things are changing. The weekly Cold Storage Holdings report indicates that cheese stocks at USDA-selected warehouses declined 3% (2.5 million lbs) over the period 02/01 through 02/18. Typically cheese is going in to aging programs at this time, thus this drawdown is contra-seasonal. On Wednesday, USDA published the Milk Production Report for December, showing production up just 0.5% for all 50 states. The monthly, year-over-year increases continue to trend lower.

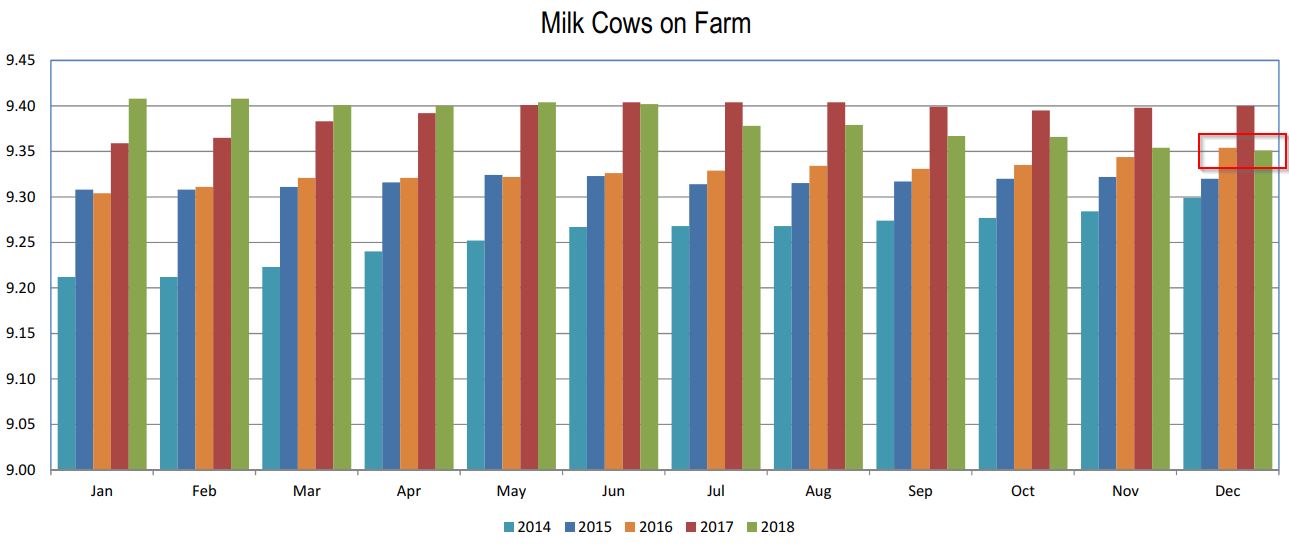

With more on-farm financial struggle since December, it almost seems like a foregone conclusion that the trend eventually dips into negative territory, if it hasn’t already. Meanwhile, cow numbers declined 3,000 head from November. At 9.351 million head, the herd size is at it’s lowest level since November 2016.

Further culling since then will likely pull the number lower. Many interested eyes will be on the next report, due to be released March 12th.

Trying to predict where markets go from here, at least in the short term, is problematic. We are heading into the peak production season, still with record amounts of cheese in storage with a questionable demand situation. The butter/powder complex, which had led Class IV prices strongly higher, has now weakened. Spot dry whey gave up more ground this week on heavy volume, while $1 NDM seems to be a resistance level. Will international interest pick up? Will domestic demand remain strong? However, if we were end users of dairy products, there is no doubt we would be active in getting our upside risk covered at current levels. There just doesn’t seem to be a lot more downside risk left. Dairy producers with milk already sold should look at getting upside risk protection (call options) in place. Those with milk to market should look back at our report from 02/08 and the Q2 chart with sell targets. Q2 settled at a $15.13 average and has bounced back after putting in new contract lows earlier this week. Selling some Q2 production around the $15.40-15.50 level might not be a bad idea in case this rally fizzles out. The July-Dec average settled at $16.25. We would consider light sales around the $16.40 level, but no more than 15% of your production. Have a great weekend!