03/08/2019

Futures Recap

| Futures Month | Class III 03/01 | Class III 03/08 | Change | Cheese 03/01 | Cheese 03/08 | Change | Dry Whey 03/01 | Dry Whey 03/08 | Change |

| Mar-19 | $15.20 | $14.97 | ($0.23) | $1.560 | $1.531 | ($0.029) | 40.425¢ | 40.700¢ | 0.275¢ |

| Apr-19 | $15.13 | $14.80 | ($0.33) | $1.552 | $1.516 | ($0.036) | 39.925¢ | 40.175¢ | 0.250¢ |

| May-19 | $15.20 | $15.03 | ($0.17) | $1.560 | $1.539 | ($0.021) | 39.800¢ | 40.150¢ | 0.350¢ |

| Jun-19 | $15.52 | $15.40 | ($0.12) | $1.596 | $1.582 | ($0.014) | 39.000¢ | 39.700¢ | 0.700¢ |

| Jul-19 | $15.98 | $15.89 | ($0.09) | $1.648 | $1.632 | ($0.016) | 39.300¢ | 39.525¢ | 0.225¢ |

| Aug-19 | $16.13 | $16.15 | $0.02 | $1.665 | $1.660 | ($0.005) | 39.500¢ | 39.575¢ | 0.075¢ |

| Sep-19 | $16.33 | $16.39 | $0.06 | $1.680 | $1.681 | $0.001 | 39.600¢ | 39.600¢ | 0.000¢ |

| Oct-19 | $16.30 | $16.37 | $0.07 | $1.681 | $1.685 | $0.004 | 39.325¢ | 39.550¢ | 0.225¢ |

| Nov-19 | $16.24 | $16.25 | $0.01 | $1.675 | $1.680 | $0.005 | 39.025¢ | 39.025¢ | 0.000¢ |

| Dec-19 | $16.14 | $16.20 | $0.06 | $1.670 | $1.675 | $0.005 | 39.025¢ | 38.775¢ | (0.250¢) |

| Jan-20 | $15.85 | $15.85 | $0.00 | $1.655 | $1.656 | $0.001 | 37.175¢ | 37.175¢ | 0.000¢ |

| Feb-20 | $15.75 | $15.75 | $0.00 | $1.658 | $1.660 | $0.002 | 36.750¢ | 36.750¢ | 0.000¢ |

| 12 Mo Avg | $15.81 | $15.75 | ($0.06) | $1.633 | $1.625 | ($0.009) | 39.071¢ | 39.225¢ | 0.154¢ |

| Futures Month | Butter 03/01 | Butter 03/08 | Change | Class IV 03/01 | Class IV 03/08 | Change | NDM 03/01 | NDM 03/08 | Change |

| Mar-19 | 228.000¢ | 227.525¢ | (0.475¢) | $15.86 | $15.79 | ($0.07) | 97.400¢ | 97.225¢ | (0.175¢) |

| Apr-19 | 230.925¢ | 228.200¢ | (2.725¢) | $16.05 | $15.92 | ($0.13) | 98.075¢ | 97.025¢ | (1.050¢) |

| May-19 | 232.125¢ | 230.575¢ | (1.550¢) | $16.24 | $16.08 | ($0.16) | 100.000¢ | 98.725¢ | (1.275¢) |

| Jun-19 | 231.750¢ | 231.500¢ | (0.250¢) | $16.44 | $16.33 | ($0.11) | 102.025¢ | 100.850¢ | (1.175¢) |

| Jul-19 | 232.725¢ | 232.000¢ | (0.725¢) | $16.63 | $16.49 | ($0.14) | 104.100¢ | 102.925¢ | (1.175¢) |

| Aug-19 | 233.025¢ | 233.000¢ | (0.025¢) | $16.71 | $16.71 | $0.00 | 105.850¢ | 104.525¢ | (1.325¢) |

| Sep-19 | 233.025¢ | 234.000¢ | 0.975¢ | $16.77 | $16.77 | $0.00 | 107.000¢ | 105.125¢ | (1.875¢) |

| Oct-19 | 232.350¢ | 233.000¢ | 0.650¢ | $16.93 | $16.85 | ($0.08) | 107.775¢ | 106.000¢ | (1.775¢) |

| Nov-19 | 231.875¢ | 232.000¢ | 0.125¢ | $16.88 | $16.88 | $0.00 | 108.500¢ | 107.000¢ | (1.500¢) |

| Dec-19 | 229.625¢ | 229.750¢ | 0.125¢ | $16.75 | $16.75 | $0.00 | 107.750¢ | 107.500¢ | (0.250¢) |

| Jan-20 | 222.000¢ | 225.000¢ | 3.000¢ | $16.65 | $16.55 | ($0.10) | 109.750¢ | 109.100¢ | (0.650¢) |

| Feb-20 | 222.125¢ | 222.525¢ | 0.400¢ | $16.58 | $16.55 | ($0.03) | 109.625¢ | 109.500¢ | (0.125¢) |

| 12 Mo Avg | 229.963¢ | 229.923¢ | (0.040¢) | $16.54 | $16.47 | ($0.07) | 104.821¢ | 103.792¢ | (1.029¢) |

Spot Market Recap

| Spot Product | 3/1 | 3/8 | Change |

| Cheddar Blocks | $1.6100 | $1.5350 | ($0.0750) |

| Cheddar Barrels | $1.4100 | $1.3650 | ($0.0450) |

| Butter | $2.2875 | $2.2675 | ($0.0200) |

| Grade A NDM | $0.9850 | $0.9750 | ($0.0100) |

| Dry Whey | $0.3600 | $0.3400 | ($0.0200) |

Spot Market Trade Volume

Fluid Milk Output

Milk production continues to climb in the Northeast, leaving plentiful supplies for manufacturers and keeping balancing plants at near capacity levels. Class I sales have slowed due to some schools being on spring break. In the Mid-Atlantic, milk output is also increasing and less milk is being moved to other regions. Balancing plants are therefore receiving more milk this week. Milk production in the Southeast is up slightly, though manufacturers are receiving fewer loads than in previous weeks. Output in Florida is about at its peak. Class I sales are slower due to spring break and cream supplies are plentiful. Farmers in the Midwest are continuing to be pummeled by record snowfalls. Many haulers in upper Wisconsin, Minnesota and parts of Iowa were unable to reach farms for milk pickup. A number of loads had to be dumped as a result. There were also some reports of barns collapsing under the weight of the snow. In the southern part of the Central region, milk production is increasing seasonally, and on the whole, milk is plentiful, with some discounting taking place and intake facilities full. Spot loads of milk range from $0.50 to $2.00 under Class, yet cheese producers are reluctant to purchase any extra milk at this time. Cream demand has begun increasing as cream cheese producers are ramping up production in preparation for spring holidays. Butter producers are also busy stocking up supplies for spring and fall. Bottle milk sales continue to decline, losing ground to plant-based products, thus more milk is heading into cheese, yogurt and milk powder production. In the West, milk output in California is up slightly and supplies continue to be heavy. Processors are running full schedules in order to handle all the milk, while Class I sales are flat. Milk supplies remain heavy as well in Arizona, though milk volumes are down from last year, so processors are not quite as busy. New Mexico milk output is higher than current demand due to some planned downtime, but a drop in production this week helped ease the burden. Finally, milk production in the Pacific Northwest remains strong. There was some expectation for a dip in output due to recent winter storms, but that never happened. Manufacturers have plenty of milk for all processing needs.

Butter

Cream supplies are plentiful in the East, as are spot offers. Butter churns are running full schedules and some manufacturers are purchasing additional loads. Manufacturers’ stocks are stable to increasing and demand is even with last week. Spring holiday orders are starting to roll in. Central region butter plants continue to run heavy schedules as seasonal cream supplies flow in. Butter is being stored for spring and fall demand. A pickup in interested relative to recent weeks has been noted. In the West, butter sales are described as “lively”, as orders have started to pick up. Inventories continue to grow, but at seasonal levels, which is not concerning.

Dry Whey

Buyers in the Eastern region are still in a “wait and see” mode, lending a weaker tone to the market. Dry whey from other regions remains price competitive to local output and global sales are slow, especially to China. With cheese plants running at or close to full schedules, the whey stream is plentiful and adding to inventories. Central region contacts report a number of dry whey end users are hesitant to take on any extra loads due to current warehouse space limitations. There’s also a belief that prices will lower further. Cheese plants are scaling back output, thus whey production is lower as well, but as multiple markets deal with swine flu, the dry whey markets are in an uphill battle. Western dry whey continues to move well through existing contracts, but many international buyers are not compelled by current U.S. prices. Uncertainty over trade negotiations is also slowing decision-making as buyers wait to see what develops.

Nonfat Dry Milk

Cheese

With growing milk production on farms in the Northeast, many cheese plants are working on active schedules. Inventories are stable to rising as plants are receiving substantial milk supplies. Midwest cheesemakers report orders have been slow since early February, and expectations going forward are not that high. Spot loads of milk ranged from $0.50 to $2.00 under Class III, prompting some plant managers to pick up a few extra loads. Cheese inventories remain long nationally, though within the region, some suggest they are in better balance. Western cheese is moving well on existing contracts, with some pockets of strong demand noted. However, spot cheese sales are slow to develop and recent price increases have cooled the moods of buyers. Plants are running at or near full capacity and stocks are plentiful, but a few contacts report cheese supplies are in better balance.

International

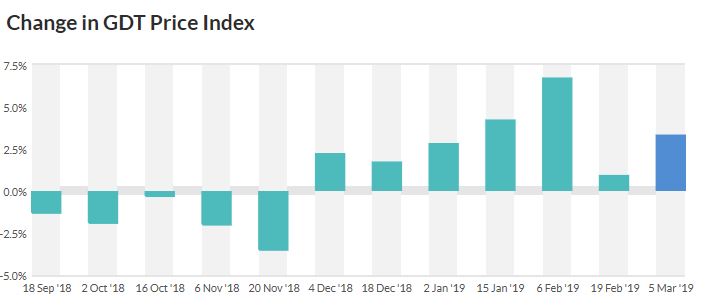

This week’s GDT auction saw the dairy price index increase 3.3%. It was the seventh consecutive increase, which also saw cheddar cheese gain 6% to a U.S. equivalent $1.76/lb.

Source: Global Dairy Trade

Evidence of extreme heat and drought was revealed in Dairy Australia’s latest milk production report. January output was down 11% vs. the prior year, while the current season (July-Jan) is now down 5.8%.

Source: Dairy Australia

Commentary

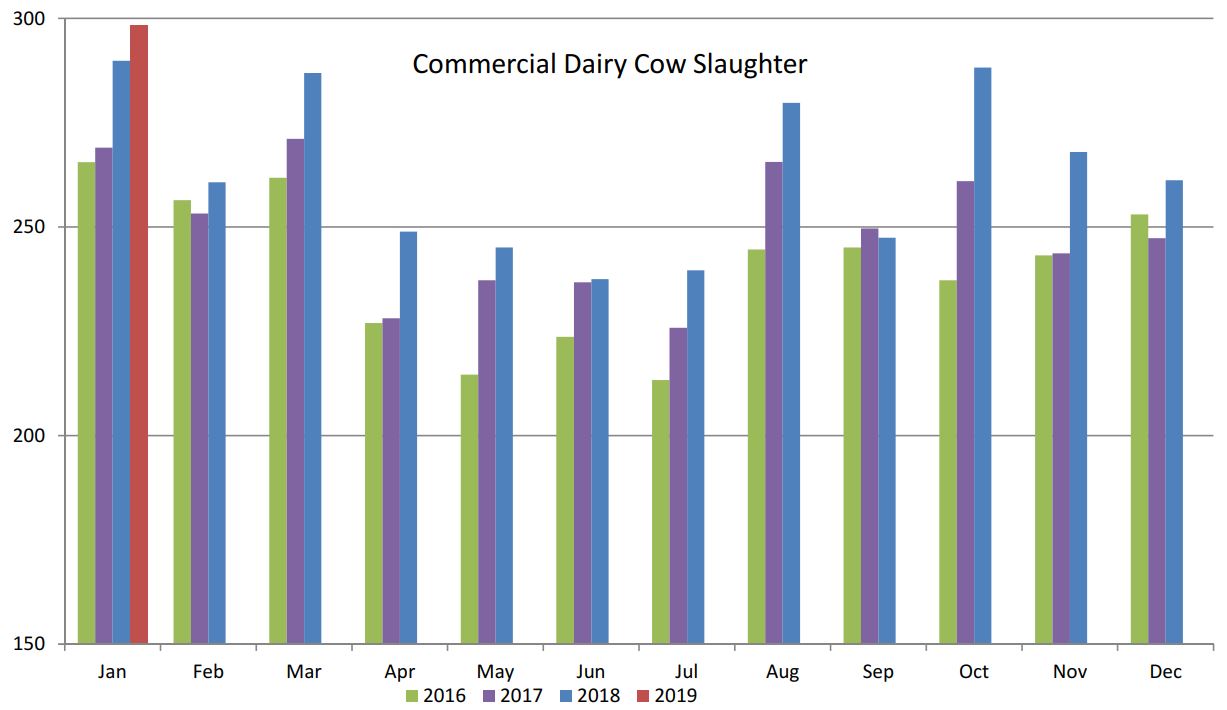

There was a lot of excitement and optimism early on this week as spot cheese prices continued to see a lack of offers, while the GDT auction on Tuesday saw a nice increase, especially for cheddar cheese. More evidence of aggressive culling was revealed in the Livestock Slaughter Report on Monday, as 298,400 dairy cows were removed from the herd in January, the highest monthly total of any month since before 2006.

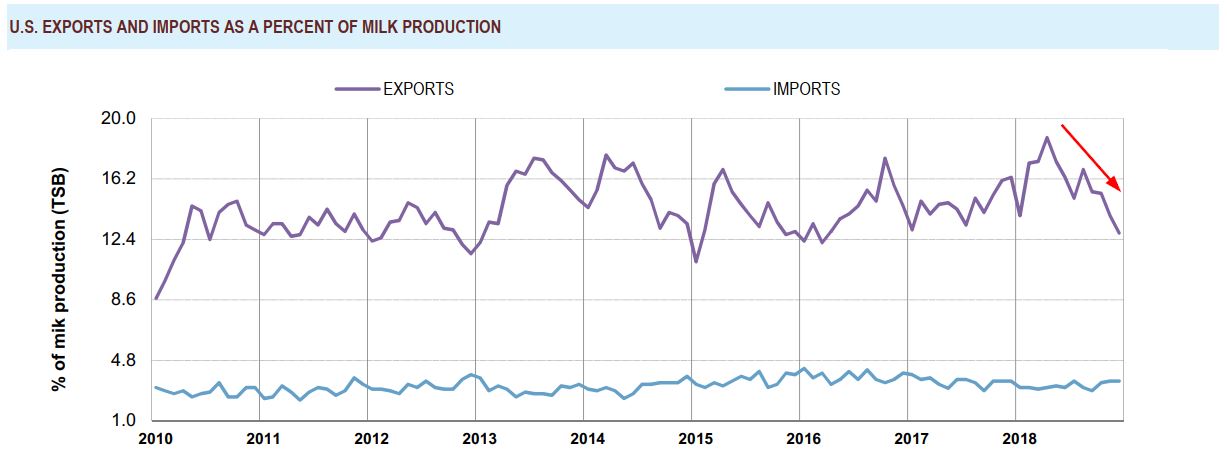

Weekly slaughter numbers were also strong, with 71,600 head culled, up an impressive 13.5% vs. the same period a year ago. Finally, optimism over the weekend that the U.S. and China were (once again) very close to a trade agreement bouyed markets. Class III futures seemed on the verge of taking off to the upside as long term resistance looked ready to be broken. The April contract traded as high as $15.24 as late as Thursday, but after blocks and barrels gave up several cents, prices up front fell hard, with April settling at $14.80. Spot settlements were lower for every component this week, with a big pickup in barrel trades. Some attribute the sudden change in spot market sentiment to the latest export data released by the U.S. Dairy Export Council. While total dairy exports reached record-high levels in 2018 (up 9% over 2017), they finished weak. The fourth quarter saw exports decline 11% vs. Q4 2017, much of that attributed to December’s numbers which plummeted 21% compared to the prior year. Total whey exports were down 35%, butterfat down 30% and WMP fell 29%. As a percentage of total milk solids produced in the U.S. in December, exports accounted for just 12.8% of U.S. milk production.

Source: U.S. Dairy Export Council

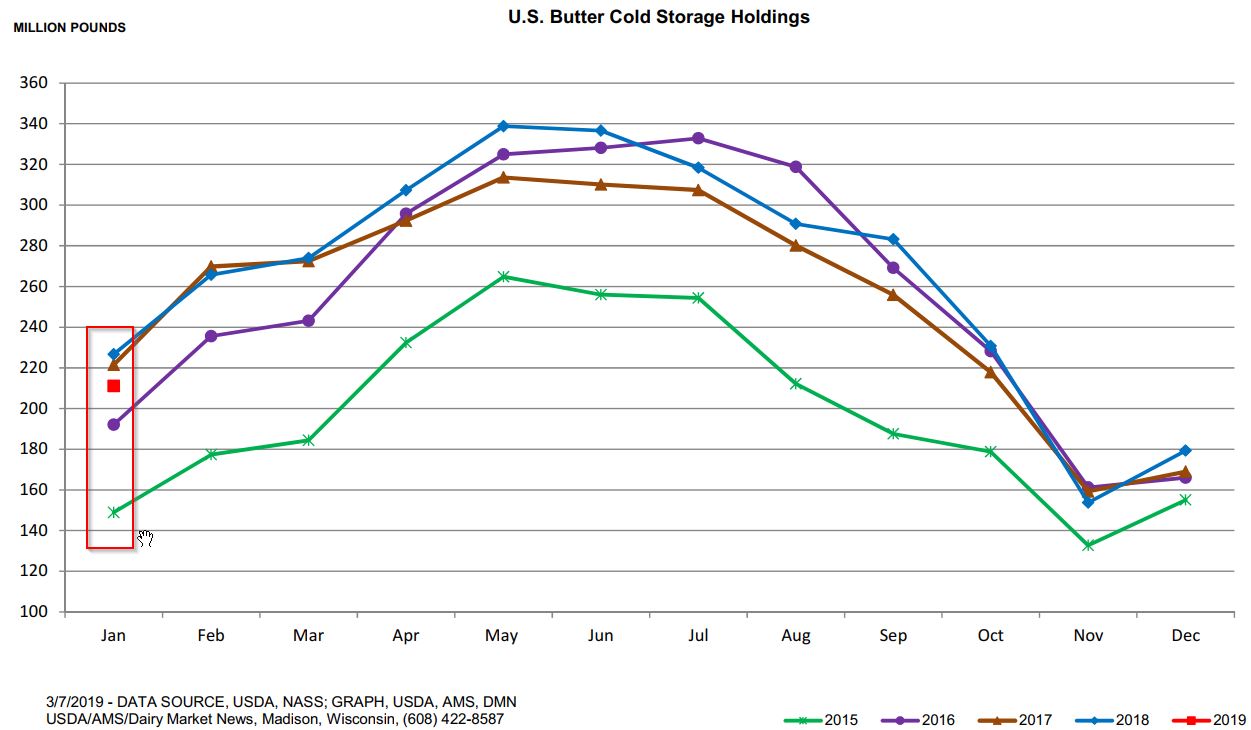

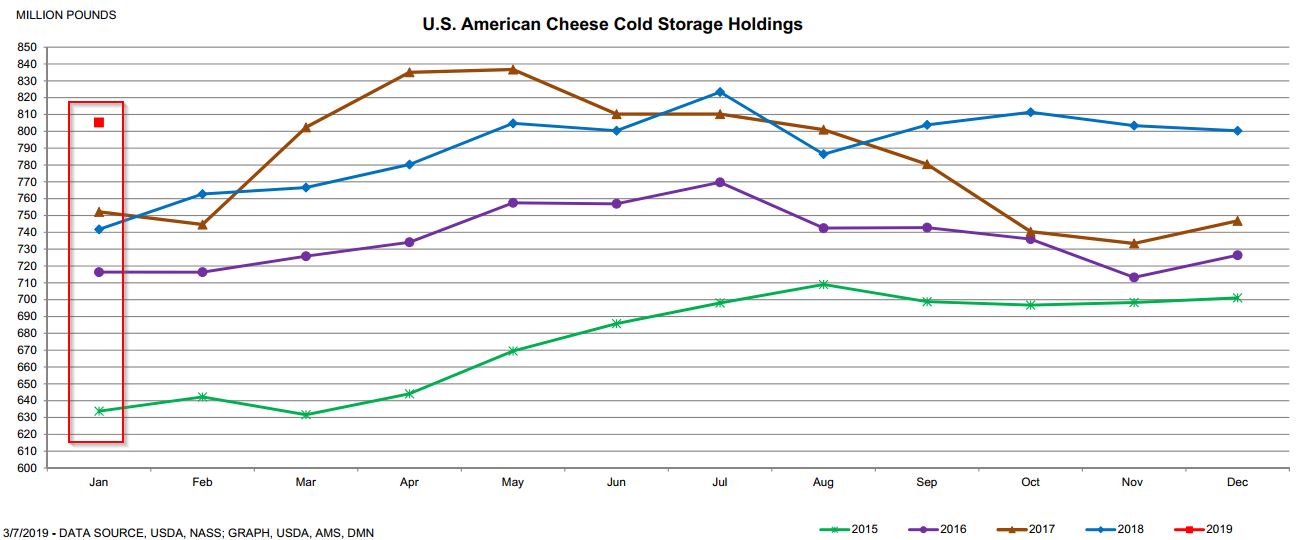

Another contributing factor was this week’s Cold Storage Report, which surprised on both the decline in butter stocks and larger than expected increase in American Cheese stocks.

Source: USDA

Despite the ongoing reduction in the milking herd, high inventories, full production schedules at most plants, headwinds for exports and a changing consumer taste for plant and nut-based drinking milks is painting a bearish face on the market. The weekly component updates above, summarized from Dairy Market News, appear to validate this view, and as we discussed last week, with plenty of milk headed our way this spring, it looks like we’ll be making at least one more cycle low before prices truly begin to recover. That said, we think the lows for 2019 are in, with both Jan and Feb settling under $14.00. The Q2 Class III pack closed at an average of$15.08 and may be headed lower. Current spot prices combined with April dry whey futures works out to about $14.31 Class III. Add the NDPSR survey basis and it’s closer to $14.70-14.80. But plenty of barrel offers remained unsold this week. Our guess is for those sellers to show up again next week. Producers who need more coverage should consider selling April at $14.90 or better, and May at$15.15 or better. If prices continue to weaken, those with milk locked in for the second half of the year should purchase upside protection in the form of call options. Assuming demand doesn’t completely fall apart, the economy continues to grow and trade issues can be sorted out, we believe the risk is to the upside near these levels. Remember to “Spring Ahead” this weekend, and adjust your clocks one hour ahead!