02/01/2019

Fluid Milk Output

The Northeast was affected by the severe cold, but milk output is steady to slightly higher, allowing more milk to enter balancing plants. Output is flat in the Mid-Atlantic and Southeast, with little to no milk heading to manufacturers. The exception is Florida, with rising output. However, that is being largely offset by very strong Class I sales. More milk was available for manufacturing in the Midwest during the cold freeze, partly due to some plant closures. A 60 degree warm-up over the weekend has some farms concerned about herd health and how the cows will adjust. Bottling demand has been slow. Heading west, milk production in California is flat, but sales are strong. In Arizona and New Mexico, output is unchanged week to week, but currently there is more than enough milk to meet demand. Finally, the Pacific Northwest continues to deal with an abundant supply of milk, as output is slowly increasing. Manufacturers are running near capacity.

Butter

Cream availability is strong in the Northeast, keeping manufacturers busy making both salted and unsalted varieties. Inventories are growing slightly, but are kept in check by strong contracted sales. The market is steady in the Central region. Sales are a bit slower than expected, but plants are happy to build inventory for spring/summer. Western butter inventories remain abundant, partly due to holiday sales not being as strong as in previous years. Butter output continues to be strong, but Q1 sales are picking up and almost at a level equaling production.

Dry Whey

Whey powder inventories in the Northeast are beginning to grow some, due to increased cheese output. Demand is steady, but market participants expect prices to soften further. In the Central region, preferred-brand dry whey is commanding a premium at around $0.50, while non-preferred loads are pushing in to the lower $0.40’s. Some buyers have limited warehouse space so are turning down offers. Western contacts are mystified by the recent market weakness, as inventories remain tight in the region, and product is moving well through current contracts. There is some question as to whether this is just temporary, or the beginning of a trend lower.

Nonfat Dry Milk

Demand is slight weaker in the East, as some traders have sufficient supplies. Drying schedules are heavy, but inventories are steady to slightly lower, due to current supplies being largely committed. The Central region is making more shipments to Mexico around the $1 level. That is keeping inventories balanced, and a bullish tone to the market. Sales are unchanged and inventories are mixed in the West. An abundant milk supply is keeping dryers busy, with market participants unsure of the near term direction.

Cheese

Heavy milk loads continue to flood the vats in the Northeast, keeping many plants are running at capacity. Inventories are stable to growing, but pizza cheese orders are strong. Demand is up slightly in the Midwest, due to the upcoming Super Bowl and upcoming basketball tournaments, but more spot milk was available this week, some at $2.75 under Class III. Western cheese output continues to be at or near capacity. Contacts are growing accustomed to the heavy inventory. Some manufacturers are placing more cheese in aging programs to add value to the product. Domestic demand is steady, but new export business has been hard to develop, due to the expectation of low prices from high inventories.

International

November milk output in the EU was 0.7% lower than in 2017, according to Eurostat. That brings Jan-Nov output to just a 1% increase over 2017, lower than expectations early on. SMP prices have firmed, as all but 3,651 MT of intervention stocks have been sold. Lower cheese output is supporting whey prices, along with stronger buying interest. Supplies are tighter than buyers would like.

The conditions in Oceania couldn’t be further apart. Australia is dealing with drought, followed by record heat, with temps this week hitting 115 degrees in some inland areas. Wildfires, dust storms, intermitant power outages, poor quality feed and a water shortage are resulting in cow deaths, dramatically affecting dairies. Meanwhile, New Zealand weather has been in the mid 80’s, with some light rain over much of the country. December milk output was up 3.8% by volume over 2017, while milk solids increased 6.1% over the same period.

Commentary

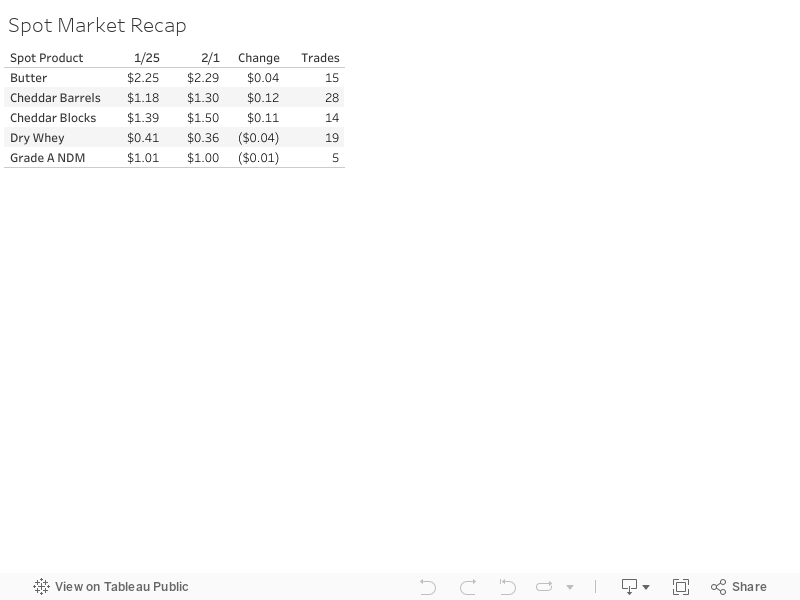

Spot blocks and barrels both picked up more than a dime on the week, with blocks hitting a price not seen since October. Volume was decent, though the spread remains wide at 20 cents. The powder complex, however, appears to have lost some steam as both dry whey and NDM finished lower. Much of the national news this week was dominated by the Polar Vortex encompassing much of the nation, and in particular, the Midwest. It was brutal (some of us live there), but most farms we talked to saw minimal drops in milk output. Undoubtedly the cows did eat more to keep warm, so there may be some lingering affects. Class III futures were higher across the board as the combination of being technically oversold, bargain priced cheese and the potential for a drop in milk output motivated buyers. News later in the week that progress in trade negotiations with China was being made, including a promise to purchase more U.S. goods (like grains), caused both a jump in the stock market and in soybean prices. Solid corporate earnings as well as strong economic indicators also played a role.

We’re finally getting some dairy data from the government (thank you USDA!). Weekly slaughter numbers are back up, with the latest weekly total (ending 12/22) at 69,600 head, up a strong 13.4% vs. a year ago, and the highest total since the 3rd week in 2013. Cows are going to slaughter, and with the recent increase in beef prices, we expect that trend to continue.

Overall, the combination of a shrinking herd in the U.S., limited to no milk growth in much of the rest of the world and a fairly strong domestic economy gives us a supportive bias over the medium to long term. Class III prices basically fell off a cliff starting Jan 11th, and maybe went too fast, too far. The gains this week could just be part of a bounce in a larger bear market, or the start of a longer term rebound. We’re starting to get more positive on the Q2 contracts. Dairy producers should consider buying cheap call options in those months, using them as targets to sell in to. For example, April Class III futures settled at $14.62. The April $15.00 call settled at 18¢. Look also at the May $15.75 call at 20¢ and the June $16.25 call at 23¢. Once bought, enter orders to sell any milk you need to market within 25-35¢ of the strike price. While you give up some upside with this strategy, a larger move higher would give you upside risk protection. July-Dec we would hold off selling, and would look at buying put options on further strength in the market.

Navigating the current markets is difficult, us included. Give us a call and we’ll help you put together a strategy that works for you. Have a great weekend!