02/08/2019

Futures Recap

| Futures Month | Class III 02/01 | Class III 02/08 | Change | Cheese 02/01 | Cheese 02/08 | Change | Dry Whey 02/01 | Dry Whey 02/08 | Change |

| Feb-19 | $14.03 | $13.98 | ($0.05) | $1.407 | $1.400 | ($0.007) | 45.950¢ | 45.875¢ | (0.08¢) |

| Mar-19 | $14.39 | $14.59 | $0.20 | $1.456 | $1.480 | $0.024 | 43.300¢ | 43.350¢ | 0.05¢ |

| Apr-19 | $14.62 | $14.80 | $0.18 | $1.490 | $1.514 | $0.024 | 41.475¢ | 41.000¢ | (0.48¢) |

| May-19 | $15.14 | $15.22 | $0.08 | $1.550 | $1.562 | $0.012 | 40.900¢ | 40.000¢ | (0.90¢) |

| Jun-19 | $15.56 | $15.56 | $0.00 | $1.598 | $1.603 | $0.005 | 39.175¢ | 39.350¢ | 0.18¢ |

| Jul-19 | $15.97 | $15.92 | ($0.05) | $1.641 | $1.645 | $0.004 | 39.250¢ | 39.000¢ | (0.25¢) |

| Aug-19 | $16.26 | $16.25 | ($0.01) | $1.675 | $1.679 | $0.004 | 39.000¢ | 39.025¢ | 0.02¢ |

| Sep-19 | $16.45 | $16.41 | ($0.04) | $1.695 | $1.693 | ($0.002) | 39.100¢ | 38.750¢ | (0.35¢) |

| Oct-19 | $16.45 | $16.39 | ($0.06) | $1.698 | $1.697 | ($0.001) | 38.250¢ | 38.025¢ | (0.23¢) |

| Nov-19 | $16.39 | $16.34 | ($0.05) | $1.695 | $1.692 | ($0.003) | 38.725¢ | 38.025¢ | (0.70¢) |

| Dec-19 | $16.23 | $16.23 | $0.00 | $1.680 | $1.683 | $0.003 | 38.800¢ | 38.300¢ | (0.50¢) |

| Jan-20 | $15.89 | $15.89 | $0.00 | $1.665 | $1.664 | ($0.001) | 39.325¢ | 39.325¢ | 0.00¢ |

| 12 Mo Avg | $15.62 | $15.63 | $0.02 | $1.604 | $1.609 | $0.005 | 40.271¢ | 40.002¢ | (0.27¢) |

| Futures Month | Butter 02/01 | Butter 02/08 | Change | Class IV 02/01 | Class IV 02/08 | Change | NDM 02/01 | NDM 02/08 | Change |

| Feb-19 | 226.68¢ | 226.25¢ | (0.43¢) | $15.87 | $15.93 | 0.06¢ | 98.850¢ | 98.900¢ | 0.05¢ |

| Mar-19 | 228.50¢ | 227.50¢ | (1.00¢) | $16.00 | $16.00 | 0.00¢ | 98.700¢ | 99.300¢ | 0.60¢ |

| Apr-19 | 230.40¢ | 228.30¢ | (2.10¢) | $16.22 | $16.10 | (0.12¢) | 100.100¢ | 100.175¢ | 0.08¢ |

| May-19 | 231.00¢ | 229.00¢ | (2.00¢) | $16.35 | $16.25 | (0.10¢) | 101.825¢ | 101.300¢ | (0.53¢) |

| Jun-19 | 231.75¢ | 229.08¢ | (2.68¢) | $16.45 | $16.41 | (0.04¢) | 102.850¢ | 103.525¢ | 0.68¢ |

| Jul-19 | 232.75¢ | 230.75¢ | (2.00¢) | $16.62 | $16.55 | (0.07¢) | 104.800¢ | 105.300¢ | 0.50¢ |

| Aug-19 | 234.00¢ | 232.00¢ | (2.00¢) | $16.71 | $16.77 | 0.06¢ | 105.700¢ | 105.825¢ | 0.13¢ |

| Sep-19 | 234.73¢ | 232.48¢ | (2.25¢) | $16.91 | $16.80 | (0.11¢) | 106.450¢ | 106.475¢ | 0.02¢ |

| Oct-19 | 233.83¢ | 231.50¢ | (2.32¢) | $16.86 | $16.94 | 0.08¢ | 107.000¢ | 107.250¢ | 0.25¢ |

| Nov-19 | 233.10¢ | 230.70¢ | (2.40¢) | $16.87 | $16.94 | 0.07¢ | 107.500¢ | 108.000¢ | 0.50¢ |

| Dec-19 | 231.40¢ | 228.50¢ | (2.90¢) | $16.74 | $16.79 | 0.05¢ | 108.000¢ | 109.000¢ | 1.00¢ |

| Jan-20 | 220.75¢ | 220.75¢ | 0.00¢ | $16.48 | $16.45 | (0.03¢) | 109.275¢ | 109.275¢ | 0.00¢ |

| 12 Mo Avg | 230.74¢ | 228.90¢ | (1.84¢) | $16.51 | $16.49 | (0.01¢) | 104.254¢ | 104.527¢ | 0.27¢ |

Spot Market Recap

| Spot Product | 2/1 | 2/8 | Change |

| Cheddar Blocks | $1.5000 | $1.5275 | $0.0275 |

| Cheddar Barrels | $1.3000 | $1.3725 | $0.0725 |

| Butter | $2.2900 | $2.2950 | $0.0050 |

| Grade A NDM | $1.0025 | $0.9950 | ($0.0075) |

| Dry Whey | $0.3625 | $0.3650 | $0.0025 |

Spot Market Trade Volume

Fluid Milk Output

Milk output is increasing in the Northeast, to the extent that many operations are able to run full production schedules. Output is unchanged in the Mid-Atlantic, leaving some manufacturers below capacity. Milk output is up slightly in the Southeast, but an increase in bottler demand is keeping many manufacturing plants idol. Florida is the exception, where output is climbing at a good pace. Strong Class I orders are resulting in higher cream supplies. In the Central region, the bitter cold has had no affect on milk production so far. Supplies are readily available, with spot loads as lows as $2 under Class. That said, some contacts suggest year-over-year production levels are down noticeably as more farms have exited the industry. Heading west, milk output in California is mostly unchanged from last week. Hay quality is being affected by weather, while stronger export demand from Saudi Arabia is expected. Comfortable weather in Arizona is giving a boost to cow output, keeping plants at or near full capacity. In New Mexico, milk production is lower this week, but a decline in Class III demand has resulted in some excess loads available. Finally, milk production in the Pacific Northwest is steady, with intakes in good balance with processing needs. Some coops in the region are encouraging their members to curtail milk production ahead of spring flush.

Butter

Cream is noticeably more accessible in the Northeast this week. The market is described as soft, with additional offers on the spot market. Churns are running on fairly heavy schedules and inventories are balanced to growing. That said, many plants want to build stocks at this time for later in the year. The story is similar in the Central region; heavy churning with cream coming in from the West. Demand is about at expectations, with interest in bulk butter growing. Western butter plants continue to run on busy schedules. Cream is still plentiful in the region, but spot loads are a little less available. Retail sales are good, while export interest is stable.

Dry Whey

Eastern whey prices slipped this week as the market seems to be weakening. Domestic sales are steady to decreasing, while international demand is down due to the African Swine outbreak and tariffs. With prices falling, buyers are more tentative. Strong cheese output is resulting in more dry whey becoming available. In the Central region, discounted milk loads are heading to the vat, thus more dry whey is being produced as well. Some end users are stocked through the end of the month. The market has turned bearish with slower domestic demand, export concerns and increasing availability. Western dry whey prices also slid this week. Inventories remain snug and domestic demand is good, but international demand is weakening. Competition from the EU and unresolved trade negotiations are pressuring prices. There is growing concern that inventories could expand.

Nonfat Dry Milk

NDM output in the East remains strong, in line with the milk supply. Dyers are mainly trying to fill orders since they don’t have uncommitted offers through the end of February. That said, buyers seem to be taking a break as they reevaluate the market. In the Central region, Mexican buying and the decline in EU inventories had pushed prices higher over the last couple weeks. But that momentum seems to have slowed down, and prices have eased somewhat. Out West, price changes have been minimal in a stable market. However, with Class IV prices higher than Class III, processors with drying capabilities are moving more milk into NDM production. Stocks are steadily growing.

Cheese

Northeast cheese makers are taking in all the milk they can handle and running full production schedules. Farm output is increasing, keeping the milk supply abundant. Some contacts suggest cheese supplies are steady to growing, while others report stock levels that aren’t that long. Some operations have even lowered their inventories. In the Midwest, cheese makers are reporting a seasonal slowdown in demand. Supplies of some slower moving cheese varieties have become burdensome, while others are balanced. Milk remains plentiful, but some production schedules are being lowered to keep inventories manageable. Western cheese inventories remain long. Domestic buyer interested has picked up, but exports have not. Many manufacturers are running full schedules, but those with drying facilities are trying to ease back on cheese production and route milk into Class IV channels.

International

EU cheese is likely to have greater access to the Japanese market compared to the U.S., due to the new Japan-EU treaty that went in to effect last week. EU cheese stocks remain lower than processors would like as most output is committed to contracts. Spot buyers are typically unable to get all the loads they desire.

Commentary

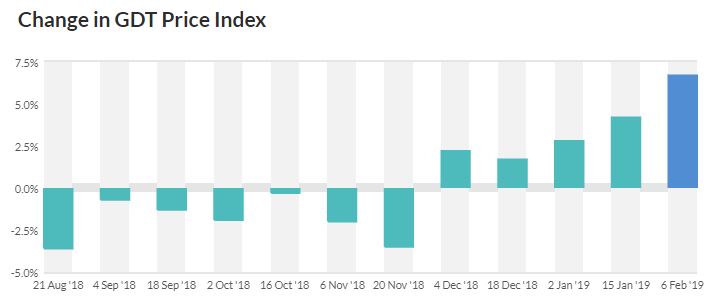

Monday and Tuesday saw Class III futures grind lower, but all that changed on Wednesday when the GDT auction finished sharply higher. The dairy price index gained 6.7%, marking the 5th successive increase, going back to early December. Tighter global powder supplies and potential drought in New Zealand were some of the motivators for buyers.

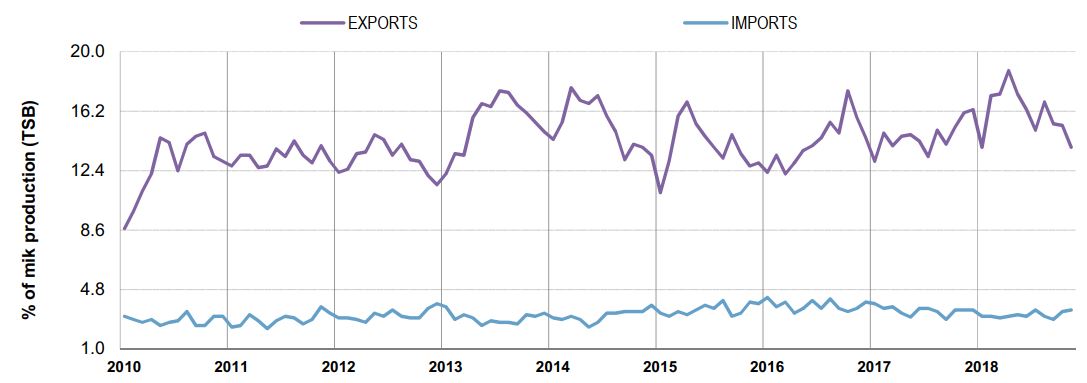

The U.S. Dairy Export Council released November trade data, which was disappointing. November dairy exports declined 12% by volume compared to November 2017. It was the first monthly decline vs. the prior year since October 2017. Trade policies certainly played a role, with exports to China down 32%. U.S. dairy exports accounted for the equivalent of 13.9% of total U.S. milk production for the month, the lowest level since early 2018.

Source: USDEC

USDA released November data for the Dairy Products Report this week, which contained a few surprises. Manufacturers stocks of dry whey were down 35% at the end of November, compared to a year ago, while dry whey output was down 8.6%. Skim milk powder production fell 27% vs. the prior year while nonfat dry milk output declined 7.7%. Butter output in November was down 2.7% vs. Nov ’17, while total cheese output increased a modest 1.0%.

In summary, we continue to deal with a mixed bag of fundamentals. The upward move in the GDT auction may have spurred cheese buyers in the spot market, with barrel cheese gaining the most and closing the spread with blocks slightly. However, cheese output is very strong across the country and demand seems to be faltering a bit. We think further gains will be met with more and more resistance. The export market did not look good in November and the U.S. is under threat to lose market share to the EU if we cannot get trade agreements in place. Dairy product output in November explains the recent strength we’ve seen in both dry whey and NDM futures, but recent weakness in those futures contracts indicates that may no longer be the case right now. And despite continuing farm closures, there appears to be plenty of milk available for manufacturing across the country at the moment, while the spring flush is around the corner. The bottom line is, there will be plenty of milk in Q1 and quite possibly into Q2. Producers should consider selling more Q2 milk on further spot market strength. A 50% retracement of the most recent high to low is a common, and fairly reliable means to enter target orders. The next level, at 61.8%, is based off of the Fibonacci series of retracement levels. Consider the chart below of Q2 Class III milk, showing the current bounce in progress.

The 50% retracement from the most recent high to low is shown at about $15.37, with the next level of resistance at $15.49. A producer could enter working orders to sell Q2 just below those levels and wait for them to hit. While there is no guarantee it will happen, they are surprisingly strong levels. In fact, while not drawn, had a producer used this strategy from the high near $16.35 (upper left of chart) to the low near $15.70, they could have entered orders to sell Q2 at it’s 50% retracement of $16.03, which clearly would have filled in the September timeframe. We’re not suggesting this is always the way to go. Clearly this would not have been helpful in a strongly bullish market, where these levels could get blown through. However, in an unclear market of mixed signals, it at least gives you a tangible target. Give us a call if you’d like us to work out some targets in individual months, or July-Dec, for example.

Have a great weekend!