What’s Bullish:

- Fluid Milk Mid-Atlantic: milk production is fairly level. Balancing and manufacturing plant intakes are below capacity at this time. Some milk from the area is traveling to the Southeast for Class I needs.

- Fluid Milk Southeast: Milk output is not meeting some market participants’ expectations. Milk off the farms is fairly flat currently. The Eastern area continues to be in the situation of receiving milk loads from other regions. Cooler temperatures are hitting parts of Florida. Milk production is growing, but Class I sales are strong at this time.

- Fluid Milk Central: Extreme cold, on top of snow and ice in the upper Midwest, has some contacts expecting a dip in milk production this week. Up until now, even with fairly mild winter conditions early in the year, overall milk production has seen year to year declines due to closing farms and higher cull rates. Bottlers were busy, while trying to get ahead of the mid to late week temperature drops and winter storms. As such, spot milk into cheese production averaged above Class: from $.50 under to $1 over Class III.

- Butter Central: More cream is expected in upcoming weeks as winter weather has bottlers busier. Churning continues apace, but demand is healthy. Butter markets are steadily bullish. Contacts suggest butter markets were expected to dip a little earlier in the year, but now some suggest expectations have shifted toward continued steady-bullishness.

- Butter West: Inventories are building at a seasonal rate as processors have plenty of cheap cream available to them. However, some contacts say that Q1 sales are relatively stronger than usual. Overall, retail orders are good, while demand from the food service businesses is very good.

- Dry Whey Northeast: Most of the current sales are made on a contractual basis. Consequently, spot trades are limited, but some buyers are quick to purchase on the spot whenever they find a few loads. Dry whey inventories are generally tight to well- adjusted with demand. Manufacturing of dry whey is ongoing at a slightly slower

- NDM Northeast: Prices are trending higher on both ends of the range and at the top of the mostly price series. Inventories are generally minimal to in equilibrium. Therefore, processors are focusing their production schedules on first fulfilling contractual orders before serving spot buyers. Several industrial facility managers plan on producing more Low/medium heat nonfat dry milk for storage whenever possible, but right now they don’t have the time and milk necessary to do that.

- NDM Central: Reported spot prices continue to trade at over $1 in the region. Recently produced loads are still hard to come by, and some suppliers report being sold out through Q1. Regionally, market tones are holding firm.

- NDM West: Large stocks are available throughout the region; however, most of these stocks are highly committed thru Q1 and Q2 contracts, according to some NDM manufacturers. Demands from the bakery sector are active as the spring baking season approaches. Exports to Mexico are strong.

- CWT member cooperatives accepted 15 offers of export assistance to sell 2.932 million lbs of Cheddar, Monterey Jack and Gouda cheese, and 83,776 lbs of butter to customers in Asia, Central America, the Middle East, and Oceania. The product will be delivered during the period from January through July 2019.

- International: November milk output in Australia was down 7.8% the prior year. YTD (July-Nov), their current milking season is lagging last year’s by 4.8%.

What’s Bearish:

- Cheese stocks at USDA-selected storage centers increased 4% (3.5 million lbs) over the period 01/01 through 01/21. Butter stocks increased 19% (4.3 million lbs) over the same period.

- Fluid Milk Northeast: Milk output is flat to slightly increasing. Class I sales are pulling strongly and Class III sales are strong, but some operations are running at capacity.

- Fluid Milk Southwest: Milk production throughout the state of California is even. Class I sales in Southern California are down because the strike in the Los Angeles school district caused the closure of the schools for several days. In Arizona, milk production is strong, but remains below last year’s volumes. However, they continue to run at full capacity. New Mexico farm milk yield is stronger compared to a week ago. The seasonally moderate weather is bringing some extra comfort to dairy cows. Consequently, their milk productivity continues to improve. Class I and II sales are both trending up whereas Class III demand has declined a bit.

- Fluid Milk Pacific Northwest: Milk production is strong. Bottling demand is steady and there is plenty of milk for most processing needs. Many manufacturers are running at or near capacity. In the mountain states of Idaho, Utah and Colorado, milk intakes are in relatively good balance with processing needs. Milk production is heavy and processors are running near full capacity. Cream is relatively heavy in the West. Most churning facilities are full.

- Butter Northeast: Churns are active as cream supplies are accessible in the region. Some manufacturers are focused on salted butter production. Some are purchasing spot loads for production needs. Butter supplies are balanced to growing a bit.

- Dry Whey Central: Class III producers continue to report steady to declining production schedules, but inventories are available for customers willing to take on interchangeable dry whey if the warehouse space is available. That said, a number of end users report being chock-full and have foregone offers at prices below current market averages. The dry whey market tone has taken a bearish hit this week on the CME.

- Dry Whey West: Some industry contacts suggest the dry whey market may be cooling, pointing to the large decline on the CME spot market. It may be too early to tell if this is a trend that takes hold or a temporary setback. Inventories are comfortable to a little snug, but buyers say there are stocks available.

- Cheese Northeast: Cheese makers continue to clear strong milk volumes into their vats. Many operations are running at full capacity. Cheddar, mozzarella and provolone cheese production is strong in the region currently. Cheese supplies are steadily increasing at this time. There are reports of increased cheese production and lower domestic demand on the spot market. Some market participants are not purchasing spot loads as their immediate needs are currently filled.

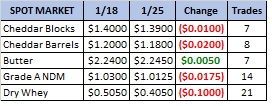

- Cheese Midwest: Generally, demand is slow for most types of cheese producers. Reported spot milk intakes were light this week. Most spot prices range from $.50 under to $1.00 over Class. Cheese barrel inventories are heavy nationwide.

- Cheese West: Cheese makers report mixed cheese demand. While markets for mozzarella are strong, as expected near the apex of the football and pizza seasons, other signals suggest total cheese demand is missing its mark. Industry contacts indicate retail demand has been adequate, but exports have yet to take off. Cumulated together, the pull from cheese buyers has not been able to overtake active cheese production. As a result, industry contacts say there has been little substantive effect on drawing down the large cheese inventories. Until improved cheese demand or reduced production can bring cheese stocks into better balance, low prices will be a symptom of those heavy supplies.

Recommendation:

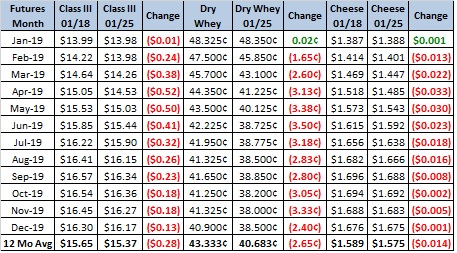

As the barrel cheese supply grows due to changing consumption habits and excess capacity, spot prices hit a low of $1.16 this week, a price not seen since July, 2009. Bidders finally showed up on Friday to bring the settlement up to $1.18, but the outlook still does not look very friendly in the near term. Powder finished lower as well, with spot dry whey giving up 10¢ for the week; that works out to a 60¢ drop for Class III. As expected,. Class III futures were hit particularly hard in the nearbys, especially Q2, which has given up nearly $1/cwt in two weeks (see top chart). The selloff was so fierce we remain in an “oversold” situation and are due for a bounce. Producers could target the $15.40 level if they desire to get some protection. The fundamental picture looks a bit friendlier for butter/powder, however, as much NDM output is sold out through Q1 and Q2, and butter demand has been very good. While dry whey gave up a dime this week, bidders started bringing both NDM and butter prices back up by week’s end. Milk output continues to struggle in the EU, while November milk output in Australia was down sharply due to drought, and that’s before record-setting heat set in in Dec/Jan. While Australia bakes, the Midwest and much of the country is heading into a deeper freeze next week as a polar vortex descends. Places as low as Iowa may see -35 temps. Expectations are for milk output to be affected as cows eat more fuel and use it to stay warm vs. make milk. Stay tuned! Grains continue to make a bit of noise as soybeans are seeing some strength (see bottom chart). The July contract broke through a downtrend going back to last June and has gained 31¢ since Jan 16th. Meal prices have been slow to respond, but they should eventually if beans keep rising. Higher live cattle prices are also moving cull cow prices higher. We hearing about prices paid that haven’t been see in months. This should encourage more aggressive culling. The partial government shutdown has resulted in a loss of weekly cull numbers, as well as the last Milk Production Report, so we’re all flying a little blind without those numbers. However, a temporary opening has been passed, and we’re hopeful a longer-term resolution can happen in the meantime. Longer term, then, we continue to have a more positive outlook.