3/3/2024

Cold storage is winning the day this week at the market turned more negative. Whey also took a hit this week as sellers returned to the cash market. The lack of demand from China has effected all commodities and whey is among them. Lower production helped push whey into the higher numbers but with lower demand the price could slump back down. Overall a bearish week for Class 3.

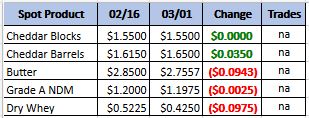

Weekly Spot Prices

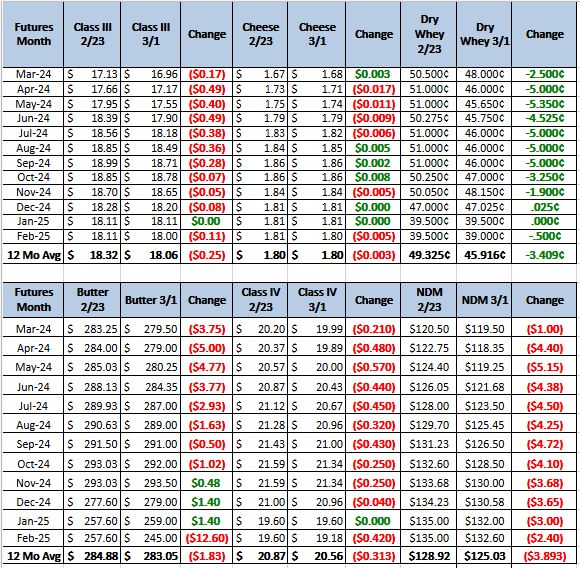

Weekly Future Prices

Cheese: Farm level milk production is trending slightly higher in the Northeast. Cheese plant contacts share steady barrel production schedules despite quiet demand. Inventories remain comfortable. Contacts in the Central region report quiet spot milk offers, but they expect spot availability to increase in the near term as Class I demand wanes due to school breaks and seasonal milk production increases. Current spot milk prices are $0.25- to $2.50- over Class. Cheese demand remains lackluster, but some barrel makers share strong year over year demand. In the West, contacts share steady to stronger production schedules. Class III spot loads of milk are tight in some parts of the region. Several manufacturers note spot cheese availability is tight through the remainder of Q1(USDA Cheese Highlights)

Butter: Retail demand is generally steady across the country. Food service demand varies. It is noted as quiet in the East and strong to steady in the West. Some stakeholders note orders for spring holiday demands are starting. Cream continues to be readily available throughout the nation. Butter makers are running strong production schedules. Butter manufacturers are busy building stock for later quarter demands and planned summer downtime. Some manufacturers say unsalted butter and bulk butter loads are tight for spot buyers. Bulk

butter overages range from 3 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved lower at every point this week. There are a number of factors at play, according to contacts, regarding the bearish turn whey markets have taken in the past week. Asian needs are being met by competitive European dry whey pricing, keeping more stocks in the U.S. in general. On the flip side, high protein composition markets, such as whey protein concentrate 80%, etc., are still considered firm. Contacts’ views remain mixed on how long this bearish turn will last, as it is simply too early to call. Animal feed whey prices are unchanged. (USDA Dry Whey)

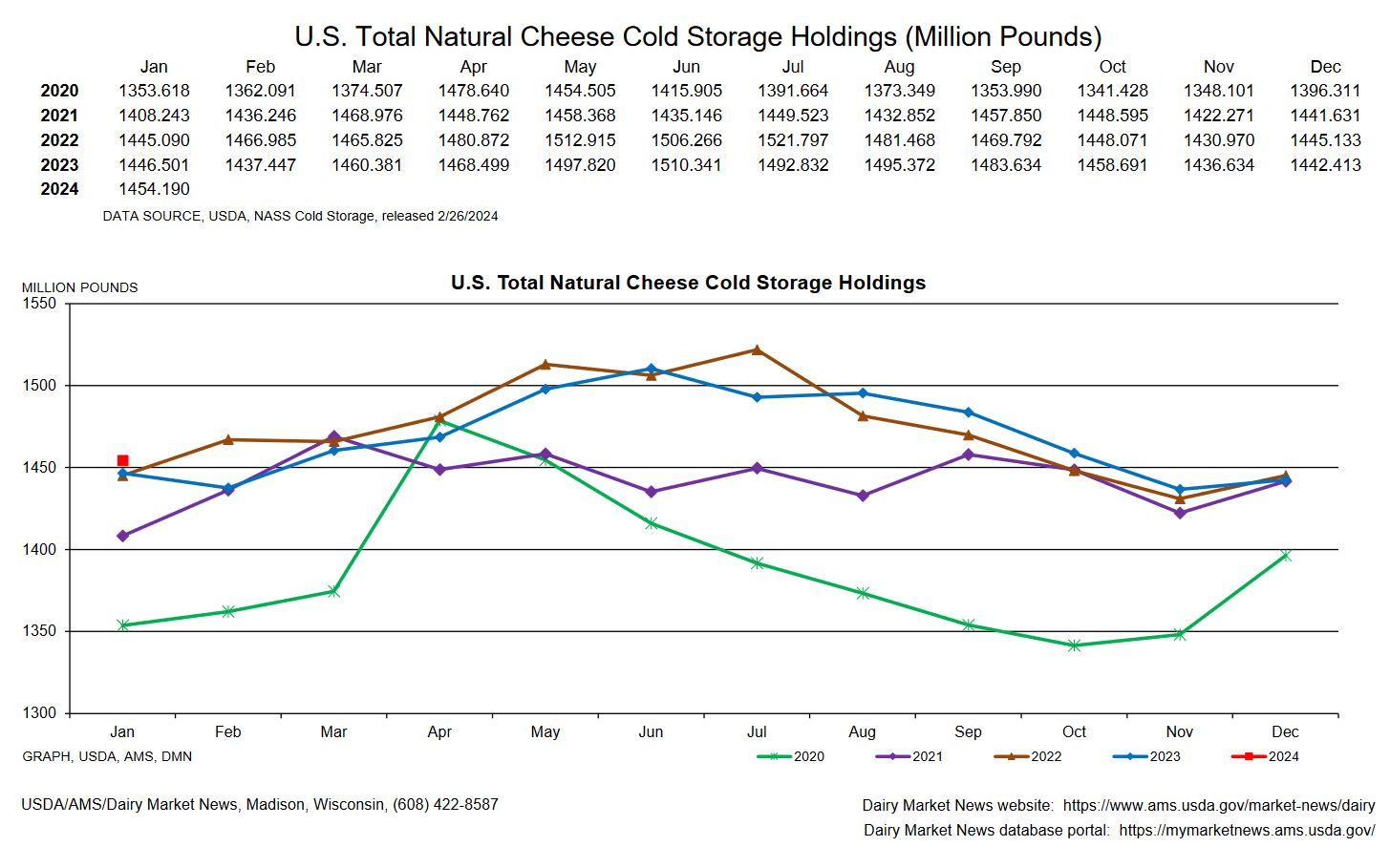

The red dot above represents the more bearish tone this week. Cold storage is above last year even though production was down. That means demand is not as good as last year. Asian demand is a big part of that as China’s econometric is still struggling. Cow numbers will continue to drop with prices remaining below cost of production. The question is then when is demand going to exceed supply. Recommendation, in the front months sell futures or buy puts, second half of the year buy call.