3/19/2023

Big jump this week spurred on by exports and the possibility of putting in a bottom on this market. Milk Production is out Monday. I do not expect Milk Production to be down as there is plenty of milk floating around with some loads going for as much as $11 under this last month. With reports of heavy culling and dairies going to action and not very many of those cows finding new homes, cow numbers should be starting to drop. As prices move higher the question is will exports hold.

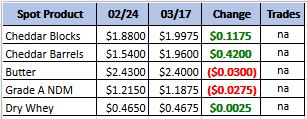

Weekly Spot Prices

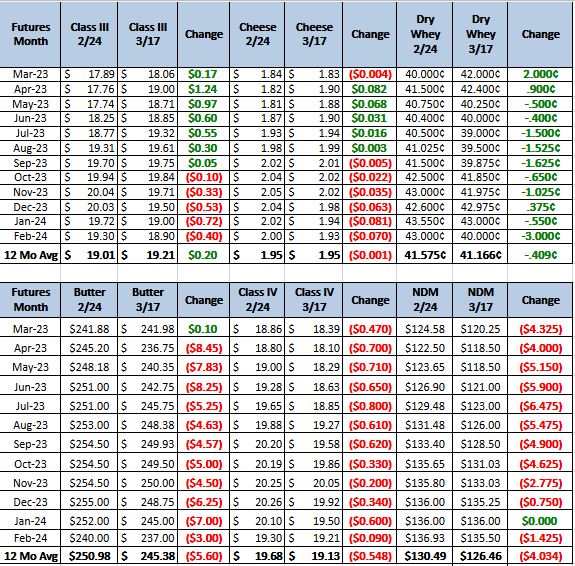

Weekly Future Prices

Cheese: Milk supplies are readily available across the country, and contacts in the Midwest continue to report spot loads of milk being traded for $10 or more under Class III. Cheese makers in the West say they are using available milk supplies to operate strong production schedules. Some plant managers in the Northeast say they have been manufacturing more cheese than expected due to strong regional milk output. In the Midwest, some cheesemakers who process cheddar and Italian style cheese are, reportedly, concerned their production capacity is not enough to build inventories for summer and fall. Cheese sales are hearty in the Midwest, and stakeholders in the Northeast note steady demand for cheese from retail and food service customers. In the West, cheese barrel sales are active, though block demand is lighter. Contacts in the West relay mixed demand from export purchasers. Spot cheese inventories are available in the West and growing in the Northeast. (USDA Cheese Highlights)

Butter: Cream volumes have begun to tighten in the East and Central regions amid strengthening demand from cream cheese and ice cream makers. Cream is available in the West, while demand remains steady to light in the region. Some butter makers in the East say they are operating seven-day production schedules, despite tightening regional cream availability. In the West, some butter makers say production is steady to strong, while others say downtime for plant maintenance is negatively affecting butter output. Demand for butter varies from region to region: in the Central region, contacts note strengthening demand ahead of spring holidays, particularly to retail customers. In the East, food service demand is steady, though current retail prices are contributing to lighter purchases from consumers. Western contacts report light retail sales and steady to lighter bulk butter demand. Bulk butter overages range from 0 to 10 cents above the market, across all regions. (USDA Butter Highlights)

Dry whey: The price range of dry whey at the bottom has moved higher. Supplies of dry whey are somewhat snug. Demand is not necessarily hearty, but end users report their bids in the high $.30s are not getting traction. End users also say they are still buying more on a necessity basis, as expectations are mixed on near-term availability, as some contacts suggest Western suppliers are not as tight as their Midwestern counterparts. Feed whey prices increased on both sides of the range. Depending on age and the nature of dried whey not meeting edible standards, price points are nearing those at the bottom end of the edible dry whey price range. Dry whey market tones are uncertain, as bears and bulls are somewhat at a stalemate. Bears, in this case, being the notable availability of milk currently moving into Class III, while bulls being a potential uptick in orders into Asian markets, some of those outside of China. (USDA Dry Whey updates)

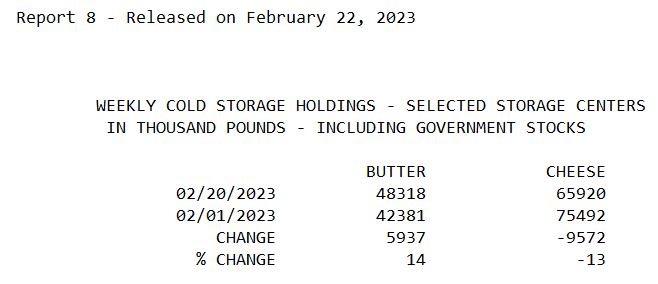

Weekly Cold Storage for February

Milk Production is out Monday but the bigger mover might be Cold Storage that is out Thursday. The weekly Cold storage for February had a big drop and the numbers have not come back up in March. There is plenty of milk for Manufacturing so I am not expecting a big drop on Milk Production, but if export demand has made a dent in cold storage when there is plenty of milk. As milk production comes down with smaller cow numbers we could see cheese availability tighten up. Recommendation this week, buy some calls.