3/25/2023

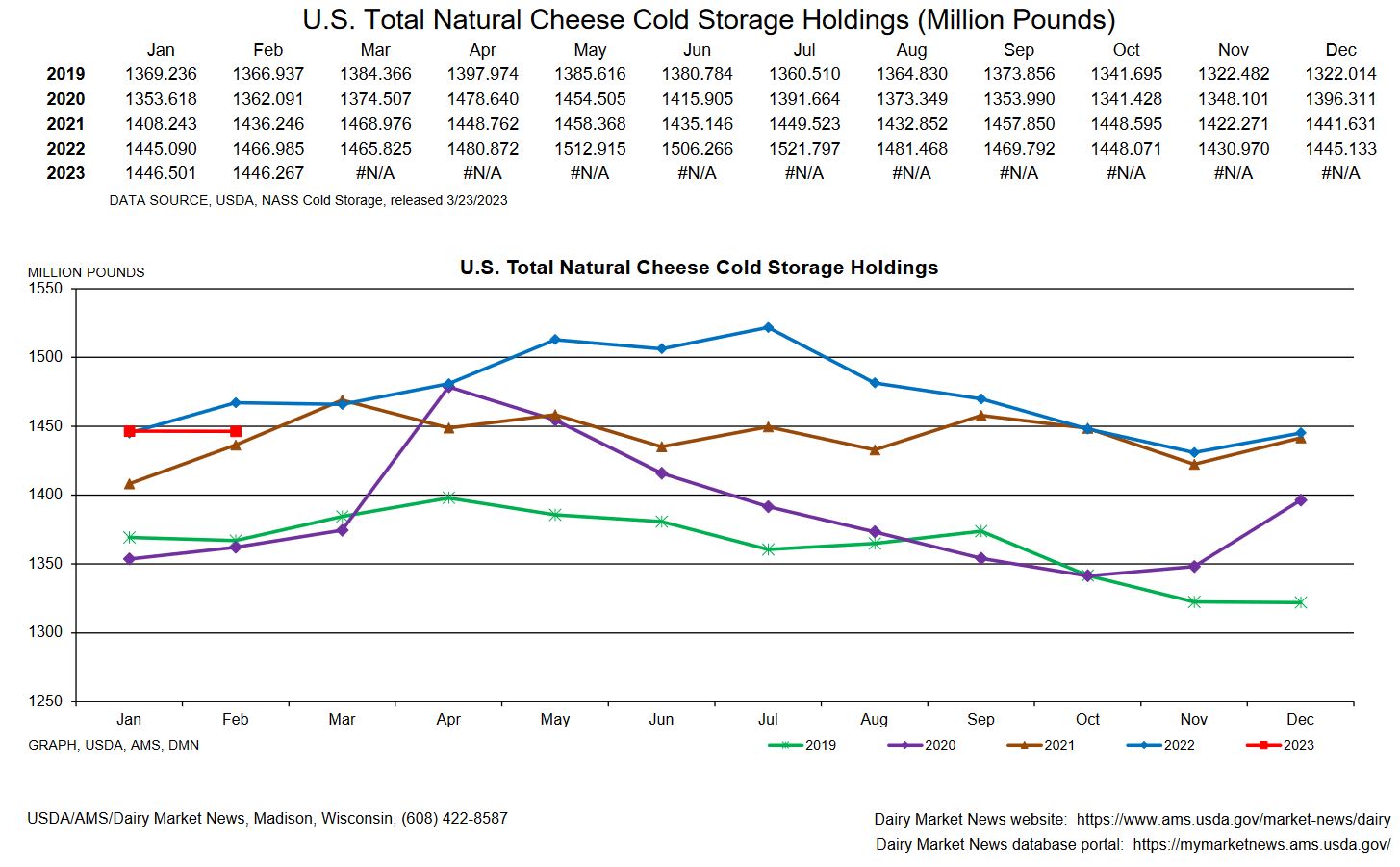

Good jump this week putting class 3 Spot prices up over $20. Exports have been good but with the higher prices there are some concerns of a drop in demand. Cold storage was out this week with a draw down of 1 percent. This is bullish for this time a year where we typically add to cold storage, but with last two week jump in prices that could be already priced in.

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk is available for processing throughout the country. Contacts in the Northeast say regional dryer challenges have freed some milk volumes intended for nonfat dry milk production. In the Midwest, loads of milk continue to move as low as $11 under Class III, but some cheesemakers say they are not receiving offers quite as low this week. Cheesemakers in the Northeast and West are operating strong production schedules. In the Midwest, some cheesemakers say their output is lagging demand, despite strong regional milk availability. Strong cheese production in the Northeast is contributing to growing cheese inventories, while retail and food service demands are steady in the region. Spot loads of cheese are available to meet market demands in the West. Contacts report steady demand from domestic spot purchasers in the West. Exports of cheese from the West are mixed. Some stakeholders note strong demand from purchasers in Asian markets, while lighter demand is present for loads to ship to other regions. (USDA Cheese Highlights)

Butter: In the East, cream cheese and ice cream makers are drawing on cream supplies, and availability for butter making is tightening. Contacts in the region anticipate greater cream availability as spring flush begins. Central region stakeholders say cream offers are quieter this week, and some butter makers are sourcing loads from the West to meet their current churning needs. Organic cream volumes are more available in the Central region than conventional cream. Cream volumes are plentiful in the West, and stakeholders say demand is steady to light. Butter makers are running active production schedules across all regions. Some processors in the East are, reportedly, running seven days a week and freezing some bulk butter. In the West, some butter makers are operating at reduced capacity as equipment is undergoing repair. Contacts in the region note steady demand for butter. Eastern butter contacts note steady to higher demand, while contacts in the Central region say sales are on par to busy. Bulk butter overages range from 0 to 10 cents above the market, across all regions. (USDA Butter Highlights)

Dry whey: Prices on the bottom ends of the range and mostly price series slid down, while the top ends of the range and mostly price series moved up. Higher to balanced inventories remain reported by stakeholders. Loads continue to be available for additional contract sales. Spot markets had moderate activity this week and market tones are slightly more bearish than bullish. The latest market price for dry whey on the CME is $0.4475, which represents a decrease of less than 1 cent since last week. Export demand from Mexico and Asian countries is steady to light. Inventories continue to outpace demand. Stocks on hand and current prices for high protein whey concentrates keep some stakeholders shifting production schedules into dry whey. Cheesemakers running strong production schedules are generating plenty of liquid whey available for drying. Dry whey production is steady. (USDA Dry Whey updates)

Good demand has jumped the class 3 prices into levels that are putting many producers into the black again. With that I would expect the cull rate to slow in many areas and milk production to remain high. Recomondation this week is to buy puts. April through June buy the 1850 put for 40 cents. July through November buy the 1900 put sell the 1800 put for 30 cents.