12/17/2022

Selling pressure forced the spot market to drop at the end of the week, but futures held relatively steady. This next week Milk Production is out on Monday and Cold Storage is out on Thursday. Expect some volatility in the futures market. On the supply and demand side. There is a flood of milk running into processing, and it is only plant capacity that is holding inventories in check. Good domestic demand is being offset with weaker exports. To maintain these prices or move higher domestic demand needs to continue to strengthen.

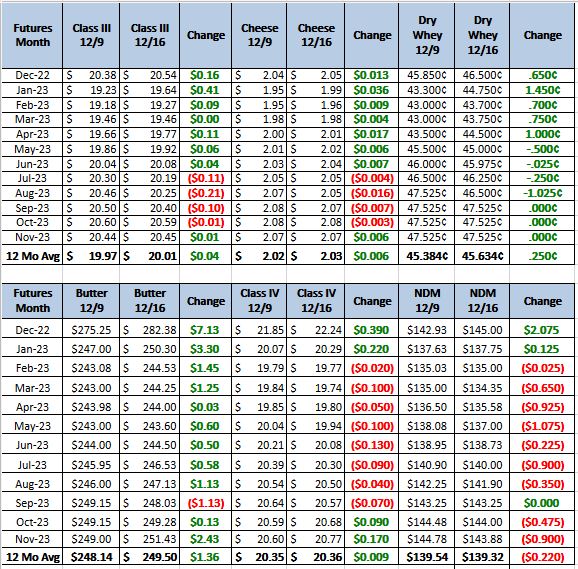

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk is available in all regions, and cheesemakers in the Northeast and West say this is enabling them to run busy production schedules. In the Midwest, cheesemakers are operating moderate to busy production schedules, though some plant managers report downtime for maintenance and/or the upcoming holidays. In the Midwest, demand for cheese curds is soft and some contacts expect similar demand until the early weeks of 2023. Contacts in the Northeast say retail demand is softening, while food service sales are steady. In the West, steady interest is present from retail and food service customers. Export demand is mixed in the West, as some stakeholders say purchasers in Asian markets are steadily ordering loads. Meanwhile, others in the West, as well as contacts in the Northeast, say lower prices for internationally produced cheese are contributing to softer export sales. Spot loads of cheese are available to purchase in the Northeast and Midwest. Some Central region cheddar and Italian-style cheesemakers report inventories are somewhat tight and anticipate this to be the case through the end of the year. (USDA Cheese Highlights)

Butter: In the Northeast and West, cream is available to meet year-end production needs. Some butter makers in the West say lower cream multiples have contributed to them utilizing higher volumes internally, in lieu of selling on the spot market. In the Central region, cream availability is mixed as some production facilities are, reportedly, full, while managers at other locations see steady availability compared to prior weeks. Butter makers are running active schedules in all regions. In the Central and West regions, retail demand is softening as purchasers have had their holiday ordering needs met. Food service demand is also slowing in the Central region, though contacts in the Northeast and West report steady demand. In the Northeast, retail demand remains strong, though some contacts suggest new orders are starting to slow. Bulk butter purchasers in the Northeast and West are limiting their orders as they are trying to avoid purchasing at higher price levels. Spot butter inventories are growing in the West. Butter inventories are relatively tight in the Northeast but are growing. Bulk butter overages range from 5 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: Prices are under some bearish pressure late in the year. Prices ticked lower on the most series, and shifting noticeably lower on the bottom of the range. Still, there are some brand-preferred trades holding steady in the lower and middle $.40s. Edible grade whey being sold into feed channels, however, are exclusively in the low and middle $.30s. Production has been steadier in recent months. This week, reported spot milk prices into cheese plants reached a low of $6 under Class, and contacts expect holiday affected spot milk surpluses (and discounts) to continue into early Q1. Demand has been sluggish. End users are acutely aware of current market tones and the lull from international buying interests. Feed whey prices slid lower on both ends of the range. Feed contacts say dairy powders for feed are widely available in recent weeks. (USDA Dry Whey updates)

As you can see from the chart above cow numbers have remained the same from May on. I do not expect that November’s numbers will very from that. This means that cow numbers will continue to increase over last year, and I would expect production to follow the same path. Production report is out Monday and if it is up over 2 percent the industry is going to see that as negative and futures could take a big dip at that point. With that in mind, the recommendation this week is to leg into put spreads. For Jan. Feb. and Mar. of 2023, Monday morning buy a put, then on a drop in the market sell a put lower. Hopefully you can get this done for little to no cost. Talk to your broker about the risks of this trade or any others you are considering. This is going to be the last report of the year, from all of us at KDM Trading have a Happy Holiday’s.