10/22/2022

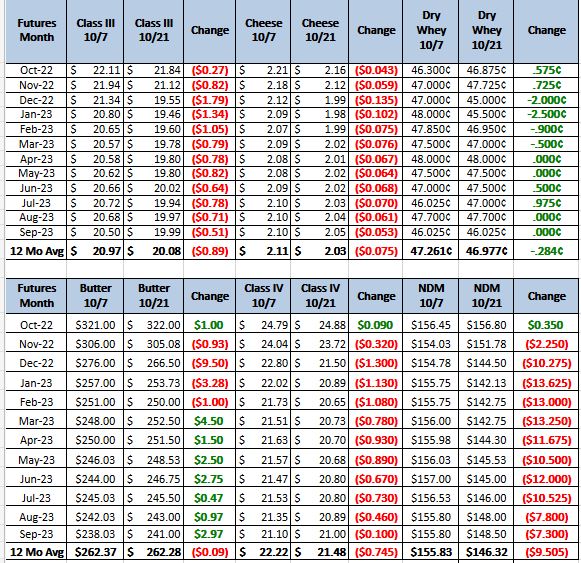

After several strong weeks of higher prices, we saw a sell off this week pushing Dec 22 through the first quarter of next year into the 19’s. Milk production for September was up 1.6 percent the futures reacted negatively to it, but most traders were expecting a number right around that. Lastly, milk production is up world wide which has brought price down and the US no longer has competitive price gap.

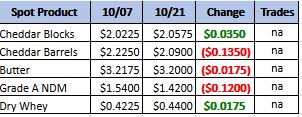

Weekly Spot Prices

Weekly Future Prices

Cheese: In the Northeast and West milk is available, allowing cheesemakers to run steady production schedules. In the Midwest, milk availability is tightening as bottlers and other holiday- based demand is pulling on milk supplies. Cheesemakers in the region say they are operating as actively as they can. Cheese is available on the spot market in the Northeast, and blocks remain available for purchasing in the West. Contacts report tighter cheese barrel inventories in the West. In the Midwest, cheese barrel inventories are snug, and cheesemakers say they are keeping up or falling behind on orders. Contacts in the Midwest say demand for cheese is strong for all varieties. In the Northeast and West, stakeholders say food service and export demands are steady. Meanwhile, retail demand is declining in these regions as inflationary pressures are affecting some customers’ purchasing habits. Cheese barrels remain priced above blocks on the CME, and some contacts in the Midwest view this as a market inhibitor. (USDA Cheese Highlights)

Butter: Cream availability is growing across the country. In the West, some butter makers are purchasing more cream to maximize production. Butter makers in the Midwest are purchasing additional loads of cream with multiples in the low/mid 1.20s. In the Midwest, plant managers are churning and/or micro-fixing to keep up with demand. Northeast butter making is more sporadic: some butter producers are actively churning, while others are selling loads of cream while their churns are down. Retail demand for butter is hearty in the Northeast. Contacts in the Central region say demand is vigorous and meeting expectations. In the West, some retailers have, reportedly, underestimated their needs and are actively looking for additional loads of butter. Food service and bulk butter demands are steady in the region. Spot butter inventories are tight in the West. Meanwhile in the Northeast, butter inventories are available though some contacts are concerned that increased holiday demand will contribute to shortages in the coming months. (USDA Butter Highlights)

Dry whey: The price range for dry whey was unchanged this week. The top of the mostly price series also held steady, while the bottom moved 1 cent higher. Domestic demand for dry whey is steady but remains below some contacts’ previous forecasts. Export demand is present, as purchasers from Mexico and Asia are sourcing loads from the region. Regional cheesemakers are running busy schedules to make use of available milk volumes. The liquid whey from this production is being utilized by drying operations who are steadily making dry whey. Some plant managers say their dry whey production is limited as they are focusing their time and supplies on the production of higher whey protein concentrates and permeate. (USDA Dry Whey updates)

The class 3 market has turned a little more negative in the last couple of weeks with international demand showing some cracks. Monday is cold storage, the weekly for September had been moving lower so I expect that to be the case on the monthly report. Recommendation this week is to buy some calls on the first half before the cold storage report, if there is a good bounce from the report it could be a good time to get sold before we get into the holidays.