10/7/2022

Demand has started to return to the domestic market right as the foreign markets have started to cool. Strong up swing this week as buyers return to the domestic cheese market. This is typically a strong demand time of the year with schools back in session and football in full swing. The October contract put in a new high this week dating back to the middle of July, and the November contract pushed back into the $22 range. On the other side global trade took a slide this week down 3.5 over all and down 3.8 on cheddar. This puts their price at an equivalent of 2.26 pretty even with our spot barrel price. Therefore, we no longer have a price advantage on the world market.

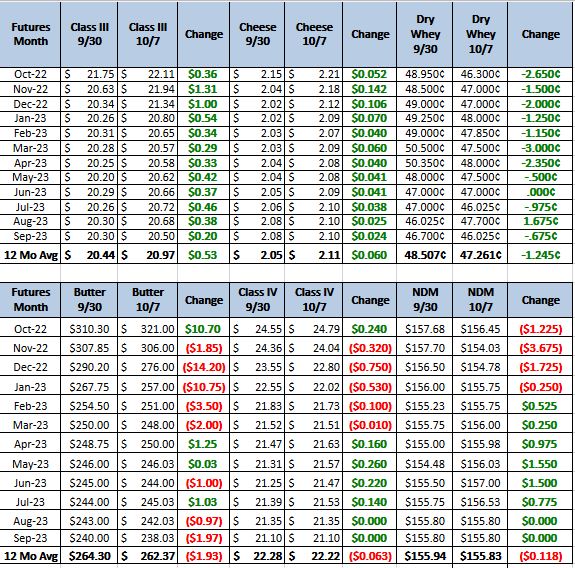

Weekly Spot Prices

Weekly Future Prices

Cheese: Cheesemakers are running steady production schedules in the Northeast and West. Some processors in the Northeast have been affected by recent storm activity. In the Midwest, downtime at some cheese plants and increasing milk production are contributing to lower spot milk prices. Demand for cheese varies across markets and regions. In the Northeast, food service demand is steady while retail demand is down compared to a year ago. In the West, demand for cheese is steady in both retail and food service markets. Midwest cheese sales are meeting or exceeding stakeholder expectations. Contacts in the Northeast and West report strong demand for cheese from international purchasers. In the Midwest, cheese availability varies but stakeholders say loads of process cheese are quickly being purchased when they become available due to order cancellations. Cheese is available for spot purchasing in the Northeast and West, but contacts in the latter say barrel inventories are tighter than blocks. (USDA Cheese Highlights)

Butter: In the Central and West regions cream is becoming more available. Cream volumes heading to states affected by hurricane Ian were moved to different parts of the country. Butter churning is increasing in the Central region. Meanwhile in the Northeast, production is mixed as churning has halted in some production facilities, but others are operating steadily. In the West, butter production is lighter due to maintenance at some production facilities. Butter demand is building in the Northeast and remains strong in the Central region. Food service demand is softening in the West, while bulk and retail sales are trending higher. Some contacts in the West say retail purchasers previously underestimated their needs and are searching for additional loads of butter. In the Northeast and West, butter inventories are tight. (USDA Butter Highlights)

Dry whey: Both ends of the price range and the bottom of the mostly price series moved lower this week. Meanwhile, the top of the mostly price series was unchanged. Demand for dry whey is steady to lower in domestic markets but steady demand is present from international purchasers. Dry whey production is steady as liquid whey remains available. Labor shortages and delayed delivery of production supplies continue to prevent some drying operations from operating at or near capacity. Spot purchasers say dry whey loads are available. Inventories are, reportedly, building as production is outpacing current market demands. (USDA Dry Whey updates)

October Class 3 Futures Daily Chart

October futures are holding a premium to NDPSR. We are now pricing October so this next weeks numbers will be the first for October. At $22+ for the futures price and the last NDPSR at $20.94 both blocks and barrels need to average 10 cents higher then the last report. That is a big jump to get up there. I continue to feel this market will continue to be range bound. Recommendation, look to sell at prices above $22 and take profits below $20 on the front months. If the numbers in 2023 work for you sell up to 50%.