2/25/2022

Dairy put in new highs this week as the market tries to figure out what to make of the current world events. With a lower milk production and inflation fears already pushing commodities higher, Russian’s invasion with Ukraine just added fuel to the fire. This has pushed most of 2022 over $22 class 3 prices on the futures and class 4 prices heading to $25 range. Even with dairy price moving to some of the highest levels we have seen sense 2014, cost of production is also moving higher quickly with corn and soybean futures also putting in new highs.

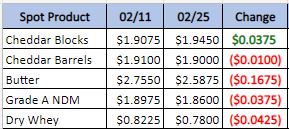

Weekly Spot Prices

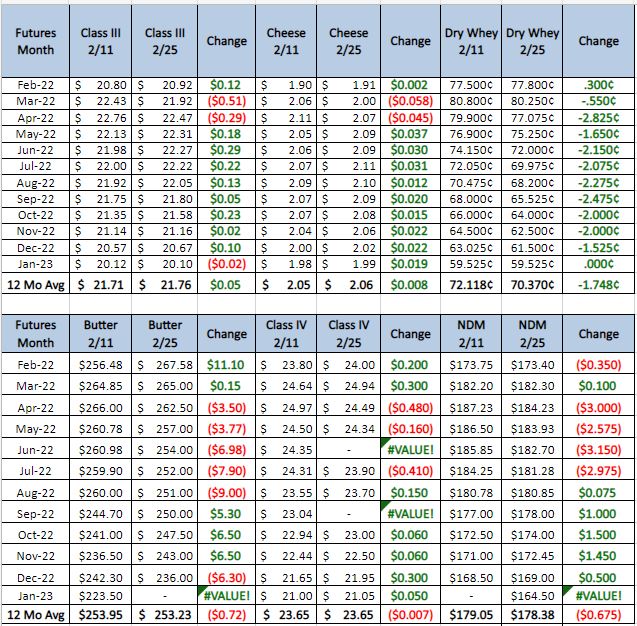

Weekly Future Prices

Cheese:

Cheese demand has found some more steadiness/strength in recent weeks. Western contacts say export demand, particularly from Asian markets, has improved as buyers there are ordering for summer/fall deliveries. Cheese production is steady, but stilted by laborer and driver shortages, which continue to obstruct cheese plant managers nationwide. Milk is generally available for the cheese vats, as discounts reached $1.50 under Class this week, although there were still some Class III prices reported, as well. Cheese market tones are steadily bullish. Cheese block prices hit the $2 mark on Thursday’s CME spot call, while barrel prices are hovering just below. USDA Cheese Highlights)

Butter: Cream is available to Eastern and Central butter makers. There are some reports of short cream supplies this week in the West as inclement weather and driver shortages have delayed some deliveries. Butter output varies somewhat from plant to plant, but production is generally active. The January NASS Cold Storage report indicates a 33 percent drop in year to year inventory levels, and some contacts have relayed tightness in regional inventories while others say supplies are adequate for near term needs. Food service demand is increasing while retail sales are softening. Export demand is reportedly strong. Across the country this week, bulk butter overages range from 7 to 15 cents above market. (USDA Butter Highlights)

Dry whey prices were mixed this week. There were some loads traded below last week’s low end of the range on block volumes, while most spot trading remains in the upper $.70s/low $.80s. Trading activity picked up noticeably week to week. Undoubtedly, production activity is irregular. Laborer shortages are continually being reported at the cheese plant level, therefore whey drying, processing and packaging has become increasingly difficult in recent months. That said, dry whey inventories, at least in the last couple weeks, have become at least temporarily more available. Some producers say there is a hesitation from end users at the $.80+ price point. Others say if buyers are not willing, they can move whey loads toward contractual obligations. Animal feed whey trading is slow, as prices are unchanged. Some feed whey traders say trading has slowed to a crawl, as customers are moving to alternatives for feed mixes due to $.60+/lb prices. Dry whey market tones are less certain than they were in the run-up of the past few months. (USDA Dry Whey updates)

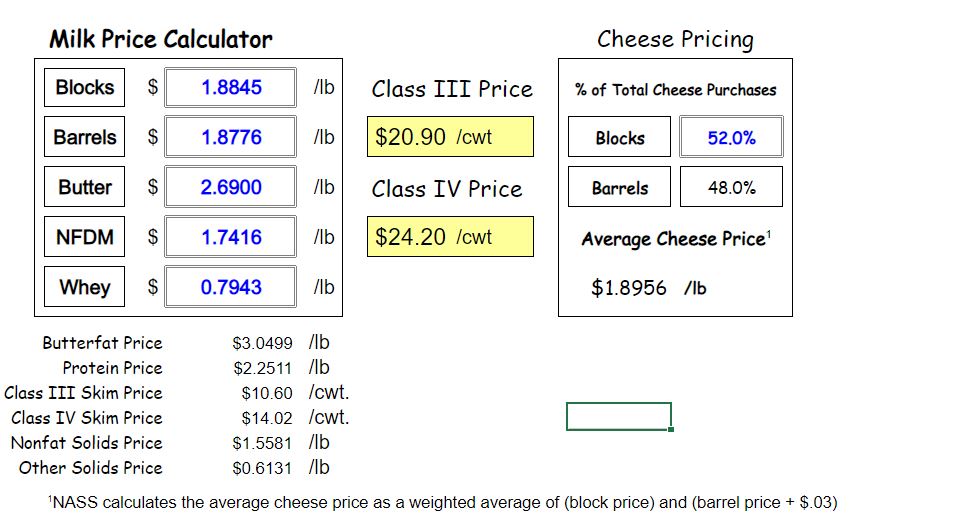

NDPSR Dairy Class Calculator

With a bullish start to this week we are now seeing a sell off on commodities. July Wheat is down 75, May Soybeans are down 68, and May Corn is down 33. These largely represent the gains they made this week. Class 3 is down 30 to 80 in the front months which is a little more then what the gains were on Thursday. The high volatility is making the option prices skyrocket. You can use this to spread out your options spreads but there is not much for volume in the option market so you need to be patient. On a more human note. I want to express my deep sympathies for the Ukrainian people and what they are going through right now.