2/13/2022

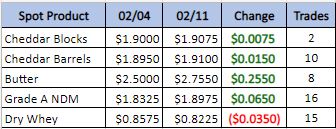

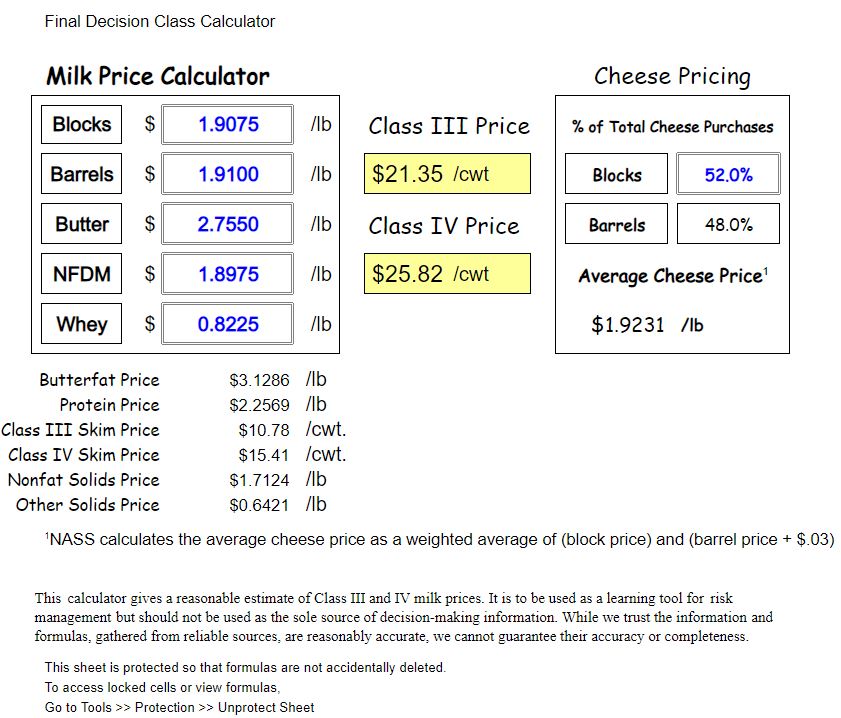

New highs on dairy this week. With with cash pricing in at class 3 $21.35 and class 4 at $25.82. There are some reports that cost of production has also skyrocketed and is coming in at $18 to $19 on a lot of farms. That being said $2 to $5 dollars over cost of productions leaves a pretty good profit margin. I expect the cull rate on dairy cows to decline and milk production to increase as we go into the spring. The big question is does demand hold up to the increased in price.

Weekly Spot Prices

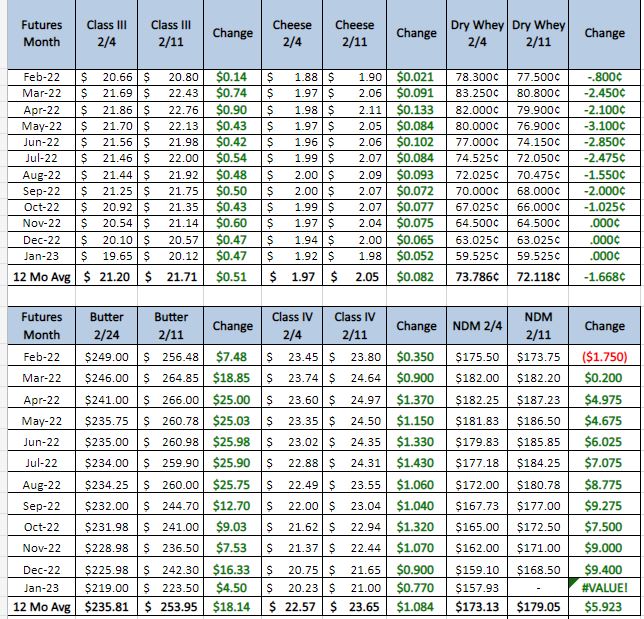

Weekly Future Prices

Cheese demand is mixed nationwide. Midwestern producers say market stability has brought some buyers back to the fold, while the culmination of the professional football season has given retail orders a push. Still, as restaurants contend with continued COVID hurdles and recent winter storms in the Northeast/Midwest, food service demand has been less than super. Laborer shortages continue to weigh on plant managers, and cheese production, across the nation. Milk availability is beginning to tighten, at least this week, in the Midwest. Spot milk prices ranged from $1 over to $2 under Class this week. Plants which are too shorthanded to run full schedules, or those which are closed for updating/cleaning, are creating milk discounts for neighboring plants, while contacts in areas where cheese production is running regularly are not getting discounted spot milk offers. Cheese market tones have settled a bit after the fluctuation of January/early February. (USDA Cheese Highlights)

Butter: Cream is steadily available in the Central and West regions. In the East, cream supplies vary across production facilities. Loads of cream continue to move into the Central region from the West, though driver shortages are causing some delays to these loads. Butter production is steady to higher across all regions. Butter makers in the Central region say that labor shortages are preventing them from running busier schedules. Retail demand is steady in the East and West. Central contacts note that butter demand has softened in recent weeks. Market prices for butter have been trading around $2.50, for the last two weeks. Bulk butter overages, across the country, range from 7 to 15 cents above market. (USDA Butter Highlights)

Dry whey prices continue northbound despite this week being one of the slower spot trading weeks so far this year. Edible dry whey stocks are tight, and there are signs that milk availability is balanced to tighter. Although there were some discounted milk prices into Class III plants, where neighboring plants are down due to various reasons, there were some overages reported on spot milk this week, as well. Whey end users are buying on a necessity basis, as on the customer side there was some easing of price pressure. Right now, though, producers say a majority of recently produced whey powder is spoken for via contractual obligations. Animal feed whey prices got a bullish price bump, also. Animal feed whey trading picked up after a fairly quiet start to the year. Dry whey market tones remain bullish on steady, albeit hesitant, demand and snug supplies. (USDA Dry Whey updates)

Dairy Class Calculator

The cash price is high and the futures are even higher. The Super Bowel is over and we have a week left of Olympic coverage. Sporting events tend to coincide with good dairy demand. There is a saying that, “we are always the most bullish at the top.” Is this the top? I do not know but domestic demand for dairy products tends to slip as we go into the spring, and the future prices go higher as we get into the spring. World prices are very strong and exports could move higher but containers, trucks, and ships remain in short supply. For recommendations look to DRP, or risk reversals. Buy the $21 put sell the $24 call Apr – Nov 2022 average cost of 20 cents. Have a good week and go team USA.