1/8/2021

Stimulus fever sent us on a rocket ride this week with more than a two dollar jump in the front months on futures. We will see if it is justified in the coming weeks as the stimulus rolls out and government purchases get under way. Elsewhere in the dairy market: The dairy products report came out this week with supportive numbers but the weekly updates were more of the same high production, lower demand. However, the farmers to food box program is the main driver and it pushed the market higher.

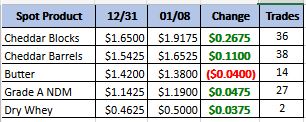

Spot Market Recap

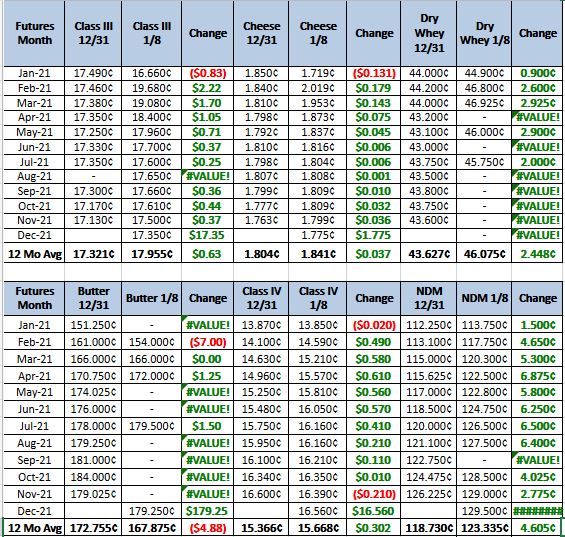

Futures Recap

Cheese: In the Northeast, productions schedules are running strong and milk volumes are abundant. Most class III plants are running at capacity with inventories increasing slightly. Retail sales are steady and restaurants sales are steady to decreased. In the Midwest, production schedules are struggling to run at capacity with staffing shortages. Milk volumes are at a surplus and spot prices are at or near holiday levels. In the Western region cheese going into pizza sales has been strong and retail orders are firm as grocers restock the shelves after the winter holidays, Food service is still sluggish but the farmers to families food box program is helping to clear inventories.

Dry whey prices have shifted higher across the board. There is ample milk supply for Class III, which has whey production picking up but the supply/demand balance is leaning stronger on the demand side which is bullish for whey prices.

Butter has been receiving ample cream supplies for active churning schedules. Butter stocks are heavy, especially for bulk butter. Retailers are still restocking shelves but orders are sporadic. Food service demand is weak, but the butter market got a lift from the food box program.

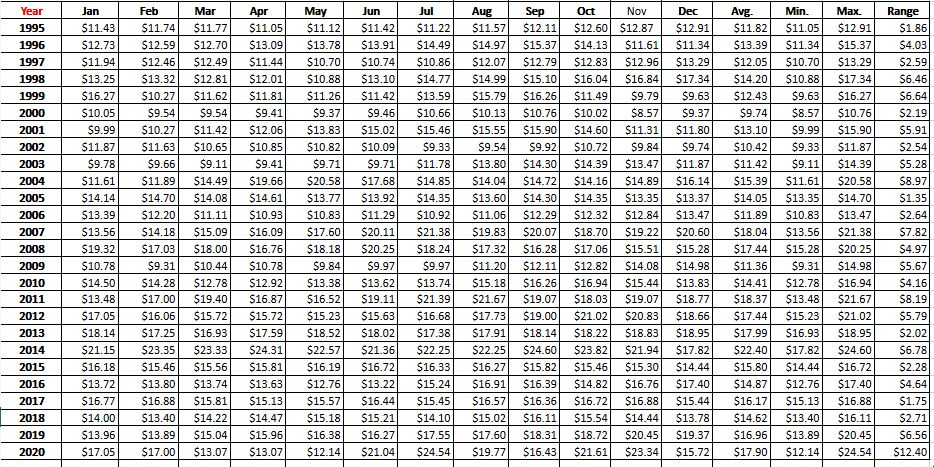

With the end of 2020 I figured it would be a good chance to look back on what we have seen in class 3 pricing of the last 15 years (see the chart below). A couple of things to note – prices have increased over the years and on the range column 2020 is by far the most volatile year we have had.

We had some big swings this week posting new highs on class 3 futures for most of 2021. It settled down a little by Friday but the numbers still look pretty good. The farmers to families food box program is now the main driver in the market, and it will continue to push the market around based on when and how much the government is buying. On the flip side, the traditional fundamentals do not look good for milk prices long term. As we have seen huge swings this last year I think that will continue this year. When the government contracts are announced the market will swing higher and as they are filled and we are waiting on the next one the market will drop. This will produce some opportunities to get hedged at good price. With the high volatility option prices have skyrocketed so I like the spreads and three ways right now. In the 3rd quarter I would look to buy 1700 put and sell the 1550 put for 40 cents. If you are comfortable with margining positions, I would also sell the 2000 call for 40 cent to get you to even. Always discuss your options with your broker to make sure any trades are right for you.