11/20/2020

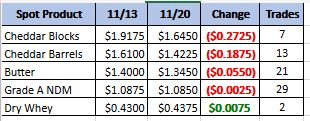

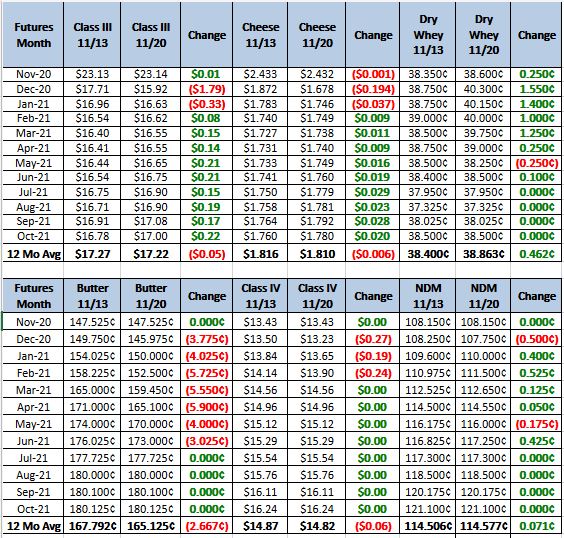

Is there a light at the end of the tunnel. With Spot cheese giving up 27 cents in the blocks and 19 cents in the barrels it is hard to say anything positive. The futures are trying to show a little life with December class III future up 40 and January up 37. They still got crushed this week with $2.70 in losses on December and $.65 in losses on January. (at the time of writing this report). The bigger long term picture is the milk production report which came out this week.

Spot Market Recap

Futures Recap

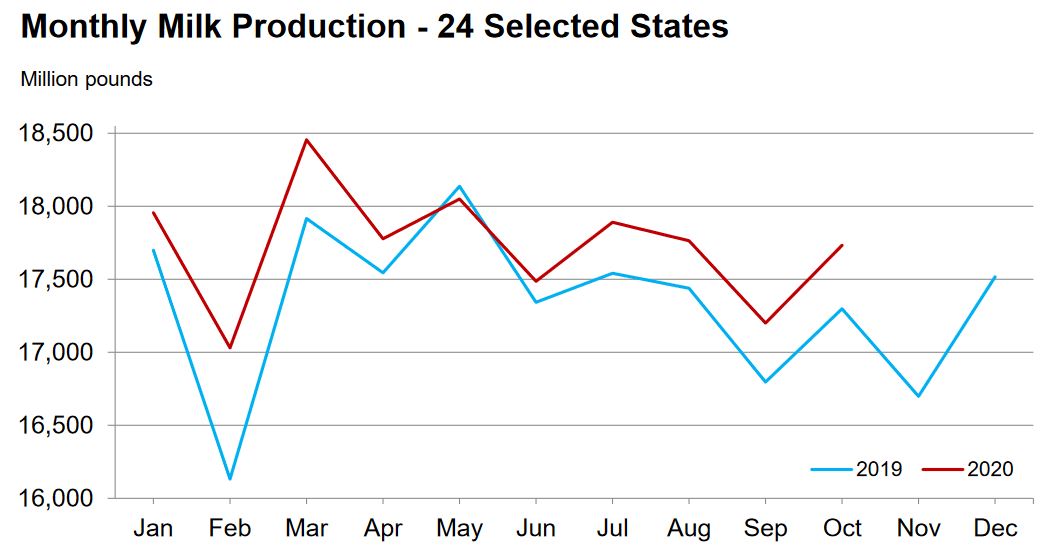

Milk production was up 2.3 nation wide and up 2.5 in the 23 major dairy producing states. That makes the second month in a row that milk production rose more then 2%. With another good class III milk price in November and cull cow prices on the lower end I don’t see production dropping any time soon. The number of milk cows on farms increased 43,000 head more than last year and 14,000 more than last month. If we stay on this trajectory there are estimates that we will be up more then 4% on production by the middle of summer. This could pose a challenge with overall demand decreasing because of food service continuing to struggle.

The other major mover of the cheese price: government buying programs which are slowing their purchases. The Western cheese weekly update stated that government purchases were less then previous rounds.

With milk production going up, government buying programs tapering off, and COVID-19 still raging, the result is an oversupply of cheese. This combination of factors has dropped our cash cheese price dramatically in the last couple of weeks. The question, at this point, is whether we have dropped enough. Last week Western cheese update reported that at these prices some buyers have begun to step back in to the market, which we saw in the spot trade this Friday with bidders showing up.

Global Dairy trade was higher this week and with the drop in the US prices there might be some opportunity there. Unfortunately COVID-19 is again on the rise globally which makes the worlds market just as vulnerable as ours. Foreign Cheese weekly update stated there is higher demand from the grocery sector with a contrast of lower demand from the food service sector leaving their market in balance as manufacturers try to shift production toward the grocery sector.

Without higher demand we are going to need a drop in production. Earlier this year when we started to go toward $1.00 cheese, manufactures placed quotas on farmers’ milk production and forced a drop in production. It back fired when the government came in with their buying programs and the plants that did not implement cut backs were better able to take advantage of the price jump. I think manufacturers will be more hesitant this time around, and until farmers really start to feel the pain of the overproduction we are going to see lower prices. There is always a chance that the government will feel the need to step in again but with the current political climate I do not think that will happen this year. I would get 100% hedge in the first quarter of this year with 50% to 75% further out. There are a lot of options to do this whether selling, buying puts, or doing some insurance like DRP. Talk to your broker to figure out what is best for you and if you do not have one give us a call.

We will not have a report next week as it is a short week because of the holiday. From all of us at KDM Trading have a happy Thanksgiving.