10/25/2019

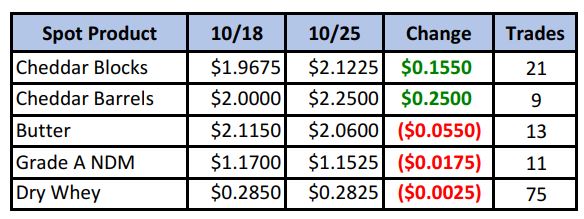

Spot barrels ripped 25¢ higher on just nine loads trading, leaving it at its highest price since August, 2014. Blocks gained 15½¢ to help put the block/barrel average at a new multi-year high of $2.19/lb. That’s that highest it’s been since October, 2014 (see graphs below).

Spot Market Recap

Spot Barrels

Block/Barrel Average

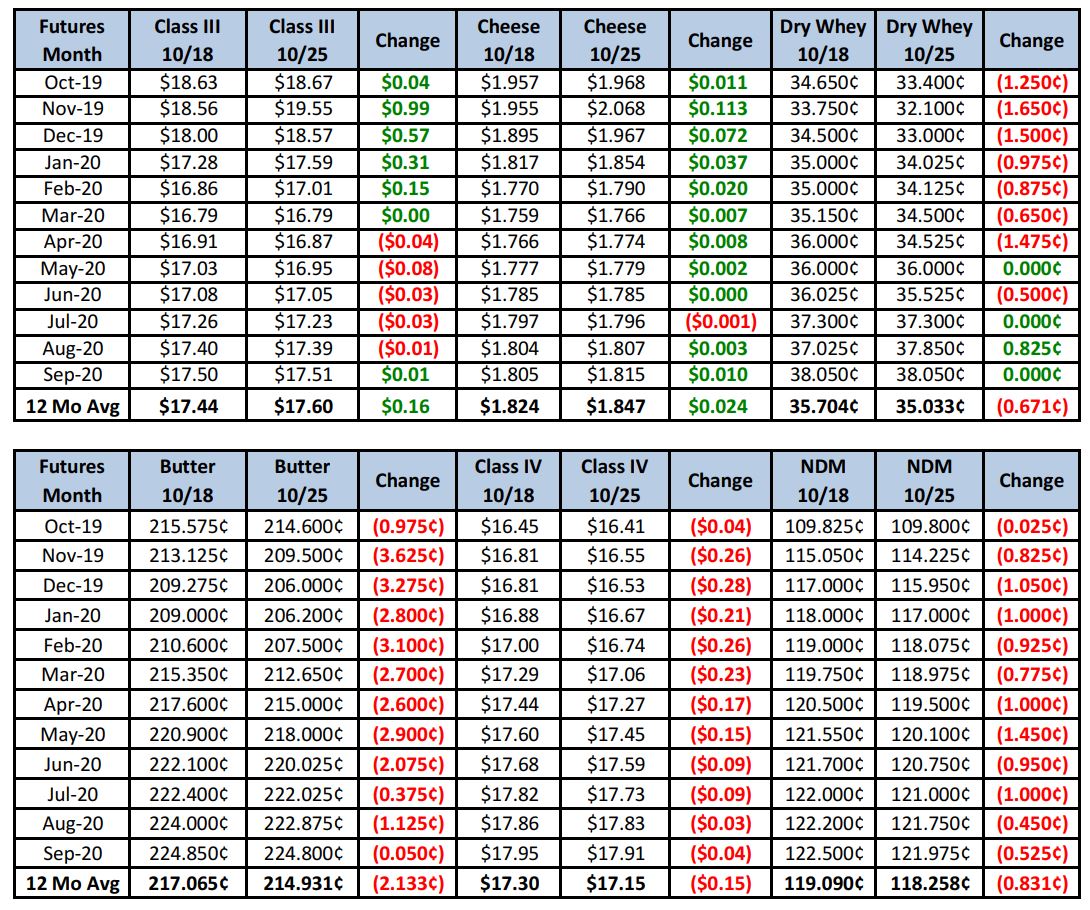

Futures Recap

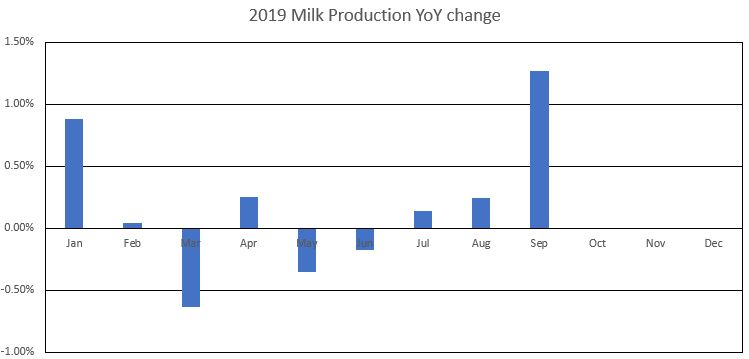

A lot of anticipated data was released this week. Starting with the Milk Production Report, September output in the U.S. increased 1.3% over last year, which was a larger gain than expected and the biggest YoY gain this year. The West led the way with TX up 9.3% and CO up 5.6%.

Cow numbers declined 2,000 head from August to September nationwide, but within the 24 top-producing states, the dairy herd increased 7,000 head.

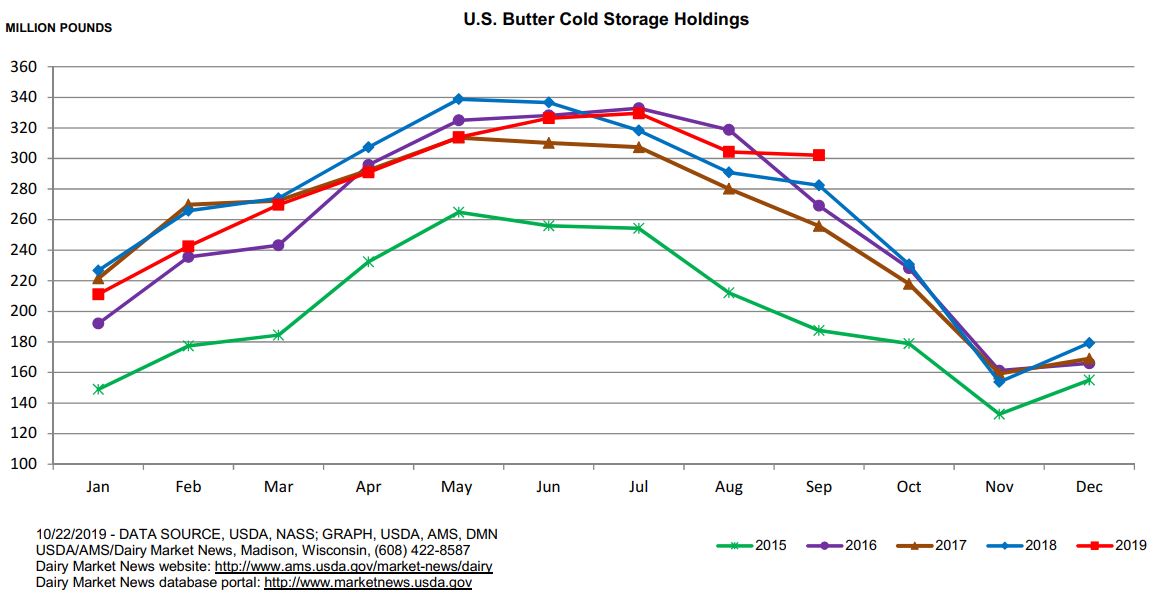

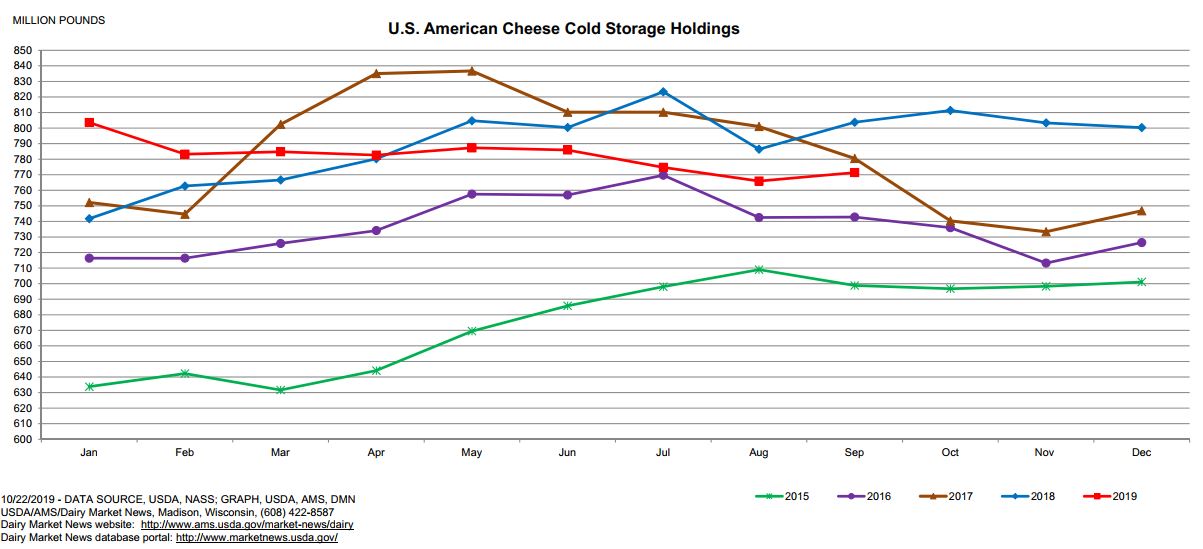

Cold Storage numbers came out on Tuesday. Butter stocks at the end of September were 7% higher than a year ago, which was seen as bearish for that market, but American cheese stocks were down 4% from the prior year and Total cheese stocks fell 1%. This is interpreted as mildly price-supportive for cheese.

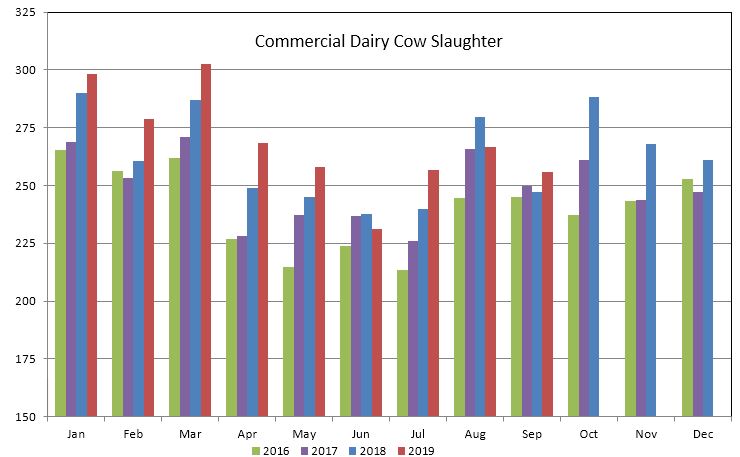

On Thursday, monthly slaughter numbers were released via the Livestock Slaughter Report. In September, 255,700 dairy cows were removed from the milking herd. This is the highest September total since 2013 and was 3.4% (8,300 head) higher than a year ago.

Dairy Market News reports milk output in the NE and SE is starting to pick up, but there is little extra available for manufacturing. In the Central region, output is about steady, the cream availability is tightened this week. Feed concerns remain as wet fields are hampering harvest. Milk production in the West remains in balance, with continued excess supply in the Pacific Northwest.

Butter sales are slow in the West, but strong cream pulls for sour cream, ice cream and cream cheese is limiting churning. Sales are steady in the Midwest and good in the Northeast, where micro-fixing is underway to satisfy demand.

Dry whey remains in the doldrums. Buyers are receiving offers for large quantities, yet inventories remain high. Prices look to remain depressed for some time. On the other hand, demand for NDM is very good, with few excess loads on hand. Some manufacturers are sold out through the end of the year. Buyers are trying to secure contracts into Q1.

With cheese above $2/lb, some buyers are hesitating, while others are not. Barrel makers in the Midwest report continued order strength, beyond expectations. Holiday demand is starting to pick up as well, with orders for gift packages keeping specialty cheese makers busy.

On the international side of things, Western European cheese manufacturers are making as much cheese as they can with available milk. With solid sales both internally and externally, most cheese is committed. Milk output Jan-Aug increased just 0.3%, so manufacturers’ ability to increase output to build stocks is limited by the milk supply. SMP prices have firmed as some customers are still seeking product for the last part of 2019. However, most stocks are already committed, while Q1 contracting is well under way.

September milk output in Australia was down 4.5% compared to a year ago, putting the current season (July-Sep) down 6% vs. last year. Milk output is near the season al peak, leading to a disappointing season so far. Hay supplies are limited, with demand exceeding supply. In addition, new season hay is showing disappointing yields in some areas and is behind schedule. New Zealand weather is much better, and that is helping keep dairy plants full.

Our take: The current tightness in barrel cheese looks like it may continue for another week or two, but don’t expect this to be the norm. We’re hearing about some plants switching over the cheddar production just because it is so profitable to make right now. This week’s Milk Production Report may be a sign that farms are starting to increase output at a more rapid pace. They certainly have the financial incentive to do so. Cow numbers are still basically flat, but growing in the dairy states. We’ll need to keep an eye on that to see if it is a trend, or a one-off. We would have preferred a more orderly and long-running bull market, but this is the hand we’ve been dealt. With strong milk prices up front, the 2nd half of 2020 becomes more vulnerable. Producers may want to consider taking an “annual average” contract on a percentage of their output for 2020 somewhere above $17.25. The current average is $17.16. Up front we would leave Nov alone at this point. Current spot prices work out to about $20.80 Class III, so even with its huge gain this week and settlement at $19.55, it’s still a steep discount to spot. Buy PUTs Nov/Dec and get ready to sell hard in a week or two through Q1.