10/18/2019

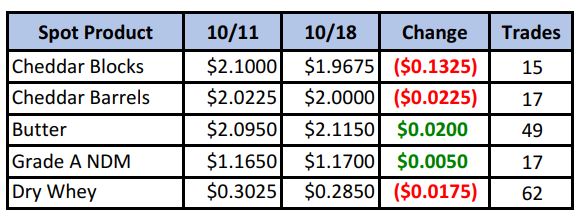

Spot Grade A NDM continued to march into new multi-year highs this week, reaching a level not seen since Nov 2014, but sellers took control of spot cheese, pushing blocks back below $2.00/lb. Dry whey continued to see the heaviest action, with 62 loads exchanging hands, while buyers in butter took on 49 loads.

Spot Market Recap

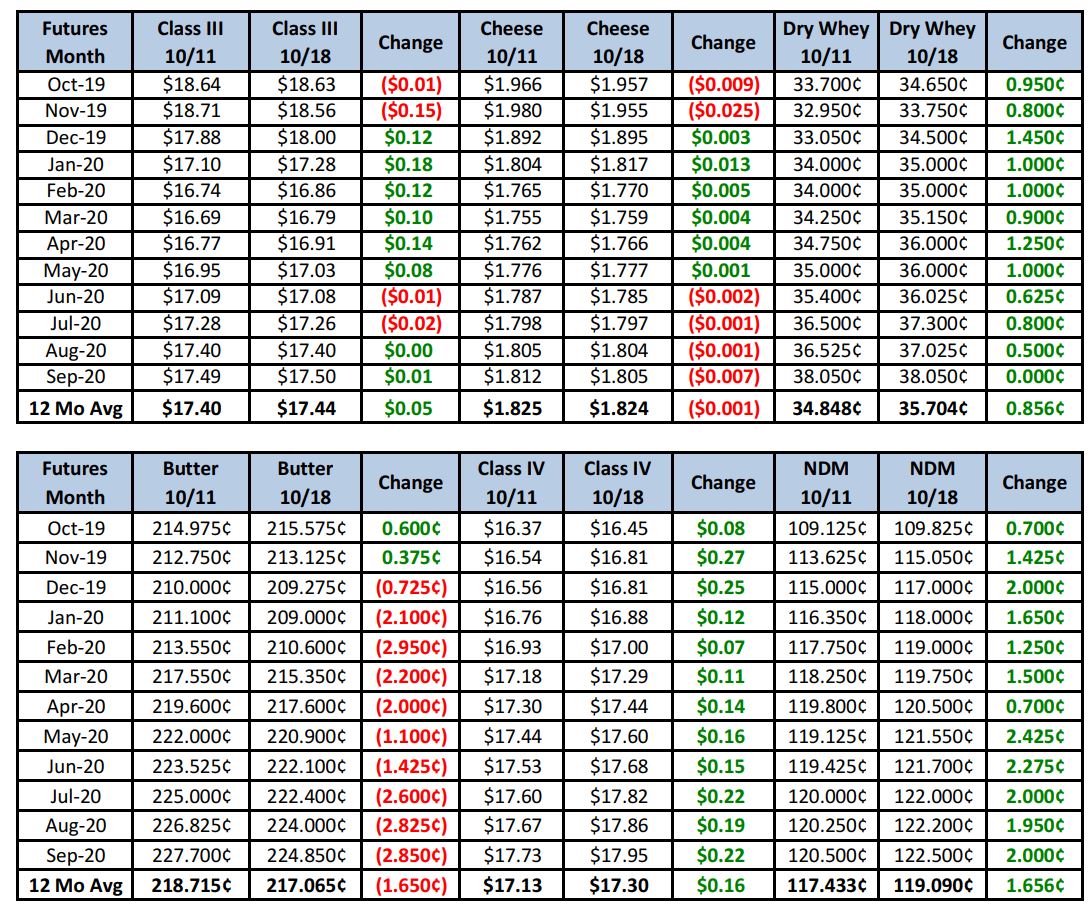

Futures Recap

Aside from the action in the spot market, it was a quiet week with no major reports released. The market felt more like it was in a consolidating pattern, getting ready for the data dump next week with the Milk Production Report scheduled for Monday, followed by the Cold Storage Report on Tuesday and the Livestock Slaughter Report on Thursday. Lots of questions may be answered in regards to the trend in herd size, days of cheese in storage and aggressiveness of the dairy cull.

Dairy Market News reports this week that fluid milk output in the Northeast is variable, but balancing plants in the Mid-Atlantic remain under capacity. Manufacturing milk is tight in the Southeast, the cooler weather is finally beginning to arrive. Milk production in the Midwest is up slightly and component levels are on the rise. However, milk draws from the Southeast continue to pull milk away from manufacturing. This is also keeping spot milk prices trading above Class. Temps in California are declining, helping improve yield, but the milk supply is described as in balance with needs. Manufacturers in the Pacific Northwest continue to have plenty of milk due to strong producer output. Idaho, in particular, has an abundance of milk, and is pushing it to surrounding states at discounts of up to $4.75 below Class IV.

Butter sales are very active as holiday season approaches, which means cold storage stocks are on the decline. Cream is readily available across most of the country, but there is some expectation that it may tighten in the near term. Dry whey prices continue to slide, but buying is picking up as it’s now seen at a “value” level. Some contacts in the Midwest are expecting a turn-around, as cheese production has slowed with the lower milk supply. Mexican demand for NDM continues to support the market. NDM plants across the country are not drying at capacity due to milk availability. NDM inventories are highly committed through Q4/Q1 contracts thus inventory is limited.

Cheese production in the Northeast is steady to strong with a gradual increase in inventories. However, buyer interest is good, especially for Mozzarella, with contracts for the remainder of 2019 in the books. Midwest cheese plants are running steady schedules, but they continue to use NDM to fortify the vat and improve yields, as milk flowing to the Southeast has kept spot milk at a premium. Cheese inventories are described as balanced to tighter. In the West, short-term demand has been enough to keep inventories under control. A new trade deal with Japan, effective Jan 1st, will see the elimination of Japan’s tariffs on cheese, which is the largest dairy category exported to the country. Cheese holdings in cold storage at USDA-selected storage centers declined 2% over the period 10/01 through 10/14.

Dairy cow slaughter for the week ending 10/05 totaled 64,200 head, up just 0.5% compared to the same period a year ago.

This week’s GDT event saw the dairy price index increase a modest 0.5%; however, it was the third consecutive increase in what is hopefully a trend. Gains were led by Rennet Casein up 3.6% and skim milk powder up 2.4%. Cheddar cheese, on the other hand, declined 2.2% to a U.S. equivalent $1.65/lb.

Looking longer term, Rabobank released a research article called “Global Cheese Trade Dynamics”, in which they state that strong demand for cheese is expected in emerging markets, particularly Asia. A growing preference for Western-style diets is setting the stage for per-capita growth in cheese consumption, while the trend towards more dining out should bode well for pizza and process cheeses.

NDM is still tight and prices continue to rise, while milk is tight in the Midwest, limiting cheese output in that region. How long will it last? The worst of summer heat is behind us, which should allow southern regions to begin making incremental gains in both output and components. But we don’t see a surge coming from the Midwest. We continue to hear about limited replacement animals and a feed shortage that should work to limit expansion. On the demand side, it’s good now as we ramp up for the holidays. Be be aware of the potential for a slow down, once we’re about three weeks from Thanksgiving. After that, ordered product won’t arrive in time. That still gives the market several weeks of hopefully good demand, and brings us well into the November calculation, which started this week. Even with the lower spot cheese prices, Class III works out to about $19.00/cwt, not including basis. If cheese can hang on a bit longer, Nov Class III futures should benefit the most as it continues to trade at a discount. But who knows, with blocks now under barrels, is a barrel plunge in the works? A lot of data will be released next week as well, which should aid in price discovery. It could be a wild week, so hang on.

Producers should consider PUT options up front and courage calls in Q1 2020. We would still be light, outright sellers of 2020 contracts.

Have a great weekend!