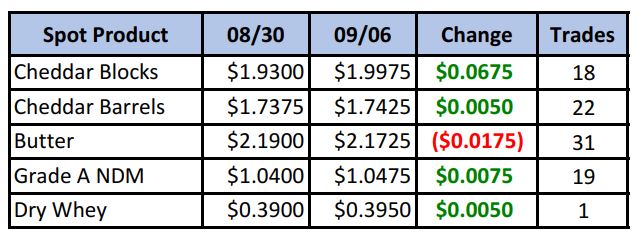

Spot cheese continued to show strength this week, with the block price hitting a level not seen since the last administration was in office; Nov 2014. Settling at $1.99¾/lb, it came within a tick of hitting psychological resistance of $2.00/lb.

Barrels managed to inch higher, lifting the block/barrel spread to a new high for the year at $1.87/lb. Next resistance looks to be the $1.90 level, but can we get a barrel rally to close the spread?

Spot Market Recap

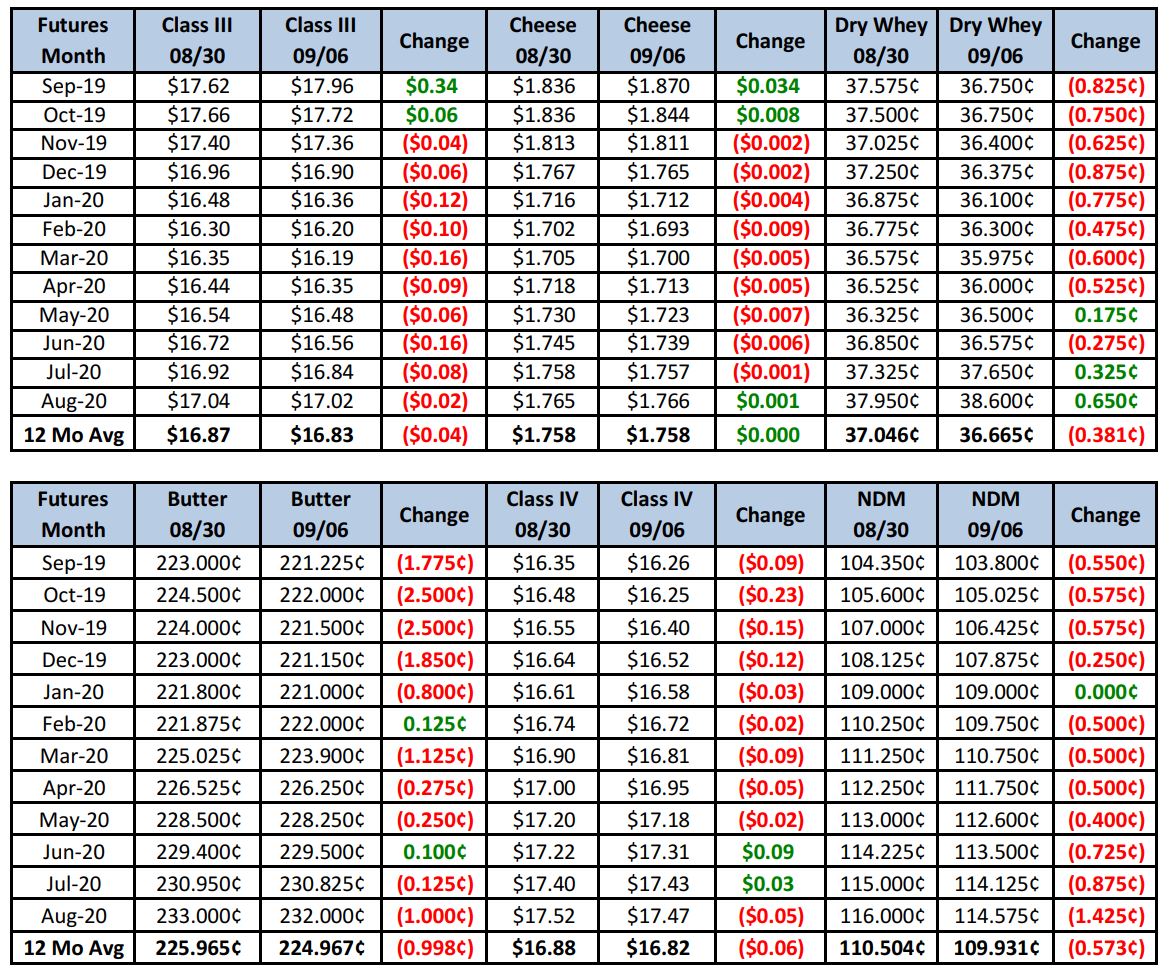

One would have thought that breaking in to new multi-year highs in spot cheese would have triggered a strong response from Class III futures, but that wasn’t the case. The September contract finished solidly higher, but only because it’s in its calculation period, with just one week left before October starts pricing. That said, current spot prices work out to about $18.10 Class III, not including NDPSR basis. Add that in and we’re pushing $18.50 if not higher. Should spot prices hold or go even higher, the Q4 contracts, and October in particular, would rocket higher. But instead, the response this week was mostly red.

Futures Recap

We find that odd and really have just one response…..

Seriously though, we respect the market, so this week’s price action in the face of a strong spot rally has us asking the question, “What are we missing?”

In the bear corner we can certainly find some fodder. Cull rates continue to decline, with 3 out of the last 4 weeks weekly totals below year ago levels. This week’s Dairy Products Report had butter output in July up 6% vs. July ’18 and above most analyst expectations.

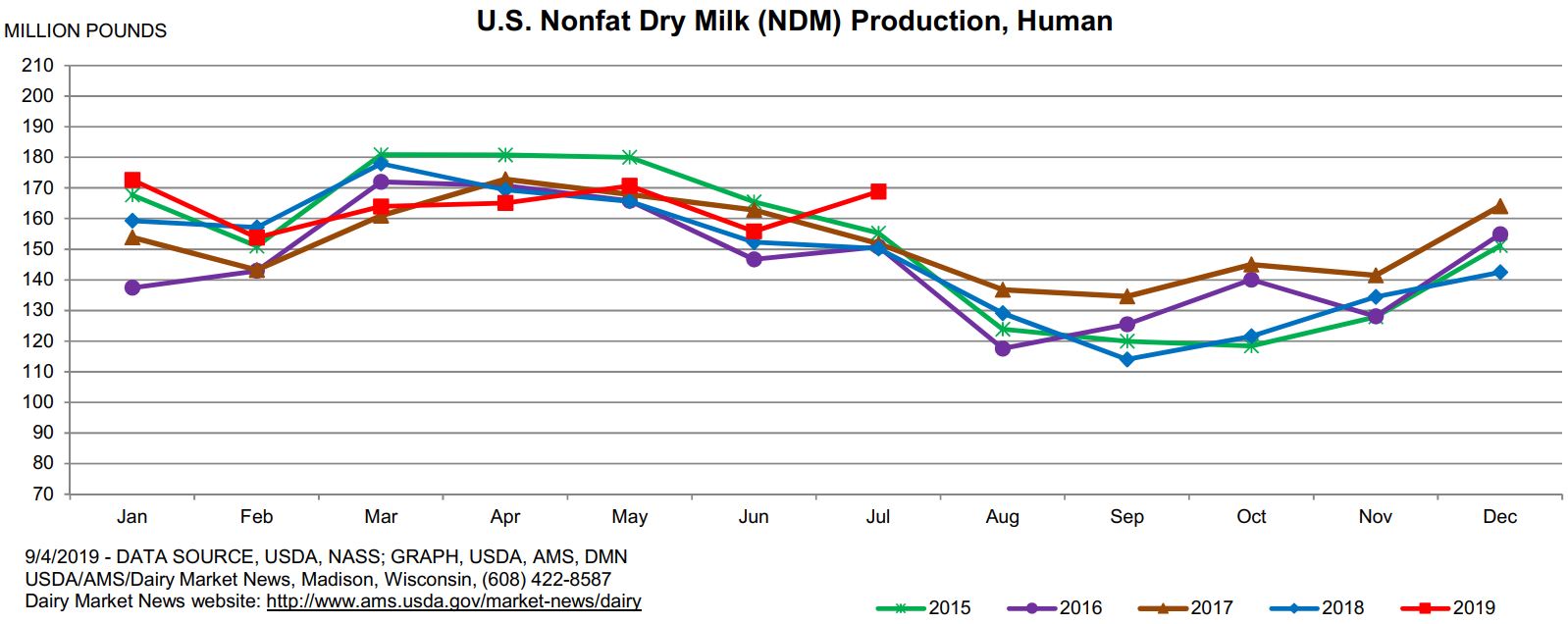

Likewise, NDM output registered a strong 12.4% YoY increase.

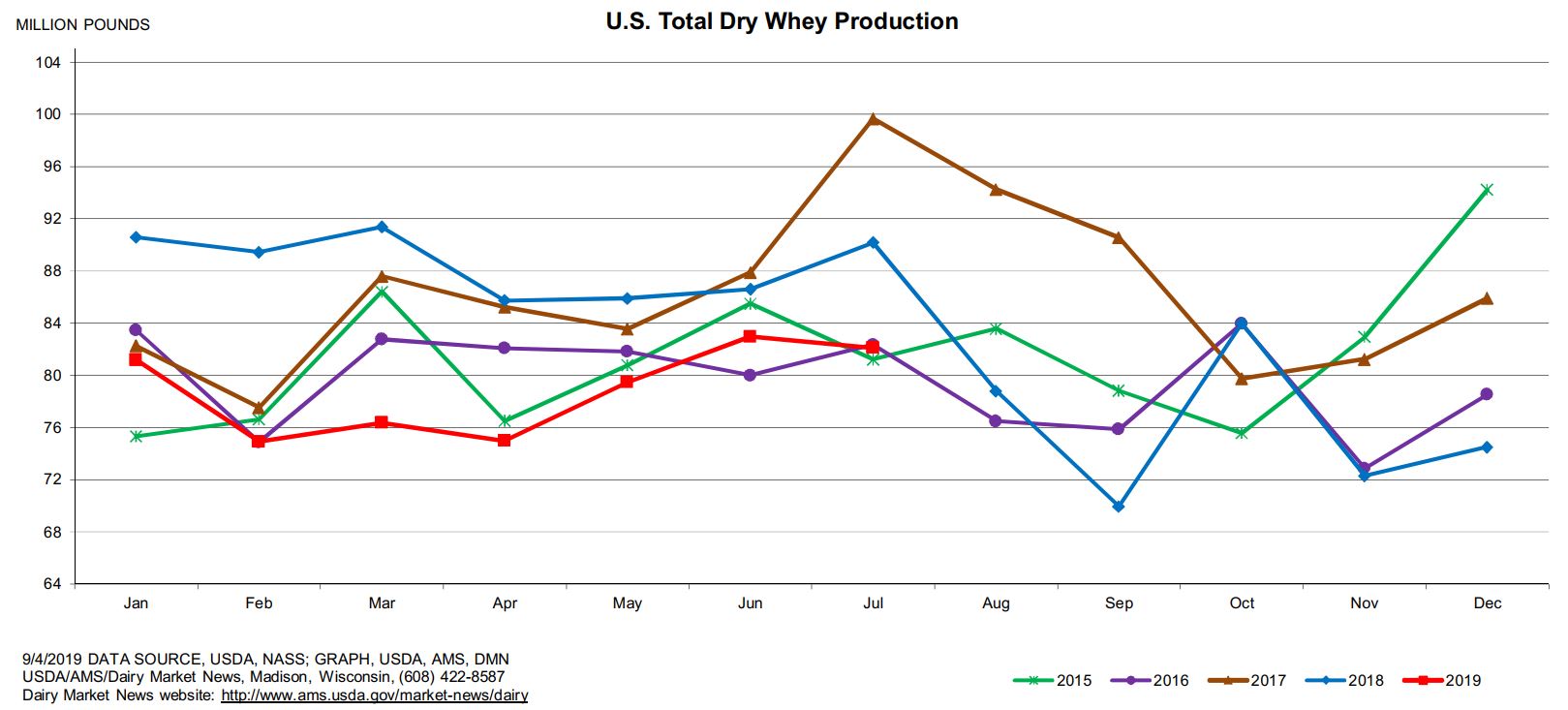

This helps explain recent spot weakness in these products, but dry whey output declined 8.9% and stocks at the end of July were down 15.6%.

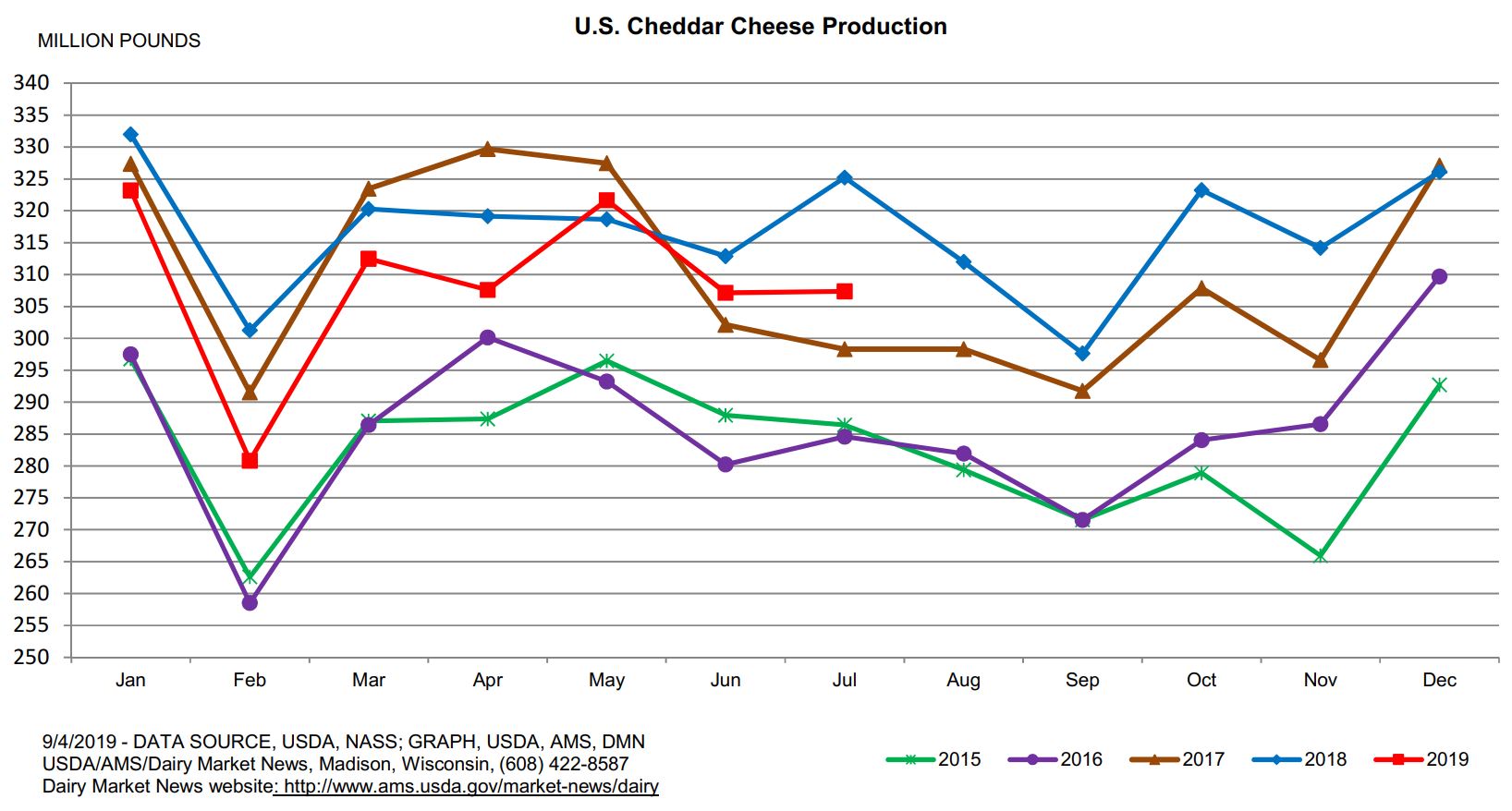

And finally, cheddar cheese output in July was down 5.5% vs. last year.

Cheese updates from Dairy Market News this week seem to confirm a strong domestic cheese market, with higher prices not deterring sales. Orders from pizzerias in the NE have picked up, while in the Midwest, food service orders have increased. Even the West reports stable export sales and increased domestic demand. While there is still plenty of cheese available, inventories have declined a bit, even as plants are running close to capacity.

Dairy exports in July were down 6% by volume, but up 10% by value, according to U.S. Dairy Export Council. Exports to China remained low, but surged 30% to Mexico. Dairy exports accounted for 14% of total U.S. milk production during the month.

Just a couple data bits on the international front. Dairy Australia reported July milk production down 8.4% vs. a year ago, giving them a slow start to their new milking season. In the EU, milk production data for May and June show output is nearly flat, with Jan-Jun production now just 0.2% higher than in 2018.

So where do we go from here? Fundamentals are painting a strong picture, but price action is painting an entirely different picture. We still lean, and are hopeful, for a continued move higher. It almost seems inevitable that we will see blocks hit $2 in the spot market next week, though they may not stay there for long. On the other hand, with domestic demand as strong as it is, maybe we’ll finally see some bidding for barrels. That would probably be enough to kick the market into high gear. But we could just as easily close the spread with a decline in blocks, which seems to be what price action is telling us. Either way, something is going to give, so expect a volatile reaction one way or the other. Producers should be looking at PUT options in Q4, especially on a strong move higher.