08/30/2019

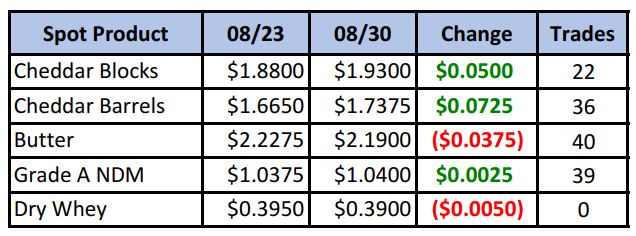

The spot block/barrel average hit a new multi-year high of $1.83/lb this week, with blocks also trading into a multi-year high of $1.93. But it was barrels with the stronger gain on the week, helping to narrow the block-barrel spread to just under 20¢.

Spot Market Recap

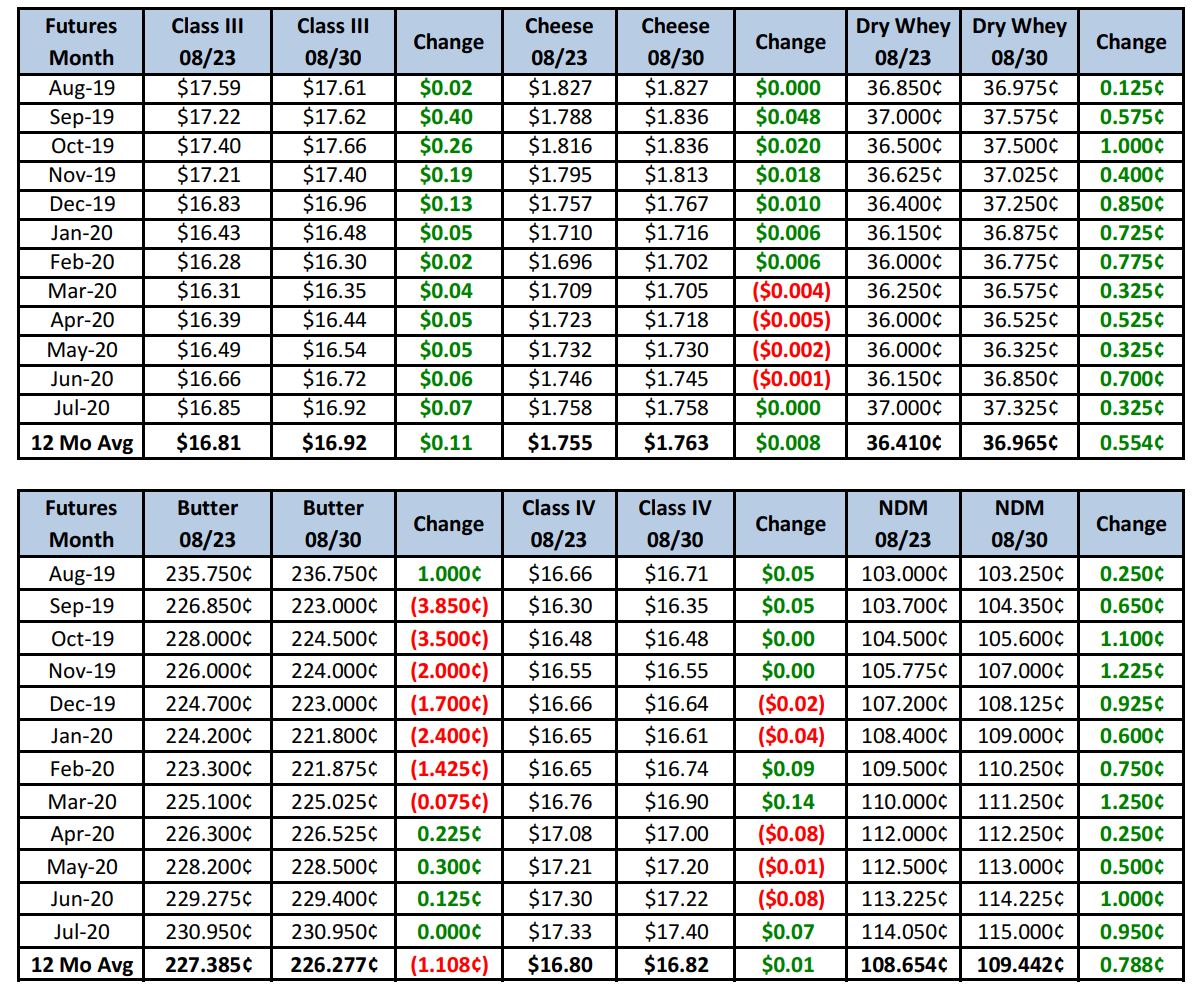

Futures Recap

Dairy Market News updates this week continue to paint a largely price-supportive picture. Strong Class I orders in the East are putting the squeeze on milk supplies. Some balancing plants are receiving less milk, while other supplies are routed to the Southeast, which remains in a milk-deficit situation. Milk output has picked up a bit in the Midwest, but bottling demand is keeping milk away from cheese plants. Components are still struggling to recover after the recent heatwave. Milk is generally in balance in the Southwest, though in New Mexico, calls for Class III milk have increased, despite reduced intakes from some cheese plants. Milk output has finally reached its peak in the Pacific Northwest, and is starting to back off. Bottling demand is up, but manufacturers still have plenty of milk for processing.

Cream availability has increased across the country, as standardization of milk increases with the opening of schools. Churning is active to process the extra cream, while manufacturers are also anxious to stock some butter away for fall demand.

Prices for dry whey have been edging higher, despite the ongoing affect of African swine fever. Lower cheese output has helped keep supplies in check, with some manufacturers indicating inventories are not burdensome.

Buyers from Latin America and Indonesia have requested more loads of NDM, perhaps signaling an increase in international demand. Domestic demand is stable, but inventory levels are starting to decline.

Cheese output is near capacity across much of the country, but demand is strong and increasing as well. Midwest plants report orders for both blocks and process cheese are strong. Western manufacturers indicate the improved demand has worked to help reduce inventories.

Weekly cold storage numbers show a 4% (3.4 million lbs) decline in cheese inventories from USDA-selected warehouses over the period 08/01 through 08/26. Butter stocks are down 5% (2.2 million lbs) over the same period.

Moving to the international picture, Dairy Australia reported milk output in June was down 7.4% vs. the prior year, giving them a slow start to their new milking season. Milk is reportedly tight, which is impacted WMP production. Hay remains in short supply. New Zealand, however, reported milk output in June up 4.6% compared to a year ago.

In the UK, concerns are growing over the impact to dairy of a no-deal Brexit. New tariffs and decades long integration with the EU could cause major disruption to both dairy operations and processors.

After our confusion last week over a sagging market, it was good to see a strong rally in Class III this week. Dry whey futures also saw strength as supplies appear to be more in balance. And despite higher prices in the U.S. for most dairy end products, international interest seems to be picking up. Football season has begun, and with it, improved mozzarella demand, which has as short shelf-life. Dairy cow slaughter for the week ending 08/17 totaled 61,600 head, up 1.7% vs. a year ago. The herd is still most likely shrinking, although at not as fast a clip as earlier in the year. Financials probably do not yet encourage herd expansion yet, and we’re hearing that credit/lending to Ag is getting more difficult.

Overall, then, our bias is still towards supporting higher prices. Current spot prices work out to about $17.80 Class III. Adding NDPSR basis brings that easily over $18/cwt. Should barrel buyers come back next week like they did this week, we could see the front months continue their strong performance. Producers should consider buying PUT options Oct-Dec for downside protection. Unexpected moves lower, like we had last week, could (and will) happen at any time. Put option premiums declined this week, making that insurance cheaper. Don’t wait until it’s too late. Looking at 2020, we could consider buying “courage” calls, Jan-Mar. Look at the 17.50 strike at an average of 13 cents. Buying those, then entering orders to sell at anywhere above $17 would result in a hedge with a solid floor price, yet give up less than $1/cwt in upside should the market continue to rally into 2020.

Note: We will be closed on Monday in observance of Labor Day.

Have a great weekend!