9/9/2023

Another week of tightening supply, with heat still persisting into September milk availability has pushed prices above class. Domestic demand is good and exports are strong to Mexico but Asia has been quite. This has kept supply and demand in relative balance, and class 3 is holding in the high 18s and low 19s. Even though the market has held here for a few weeks it does not feel settled. If there is an uptick in demand before production can come back higher numbers are a likely result. If production comes back and export demand does not improve there is enough plant capacity to overwhelm the market.

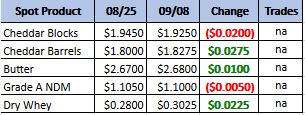

Weekly Spot Prices

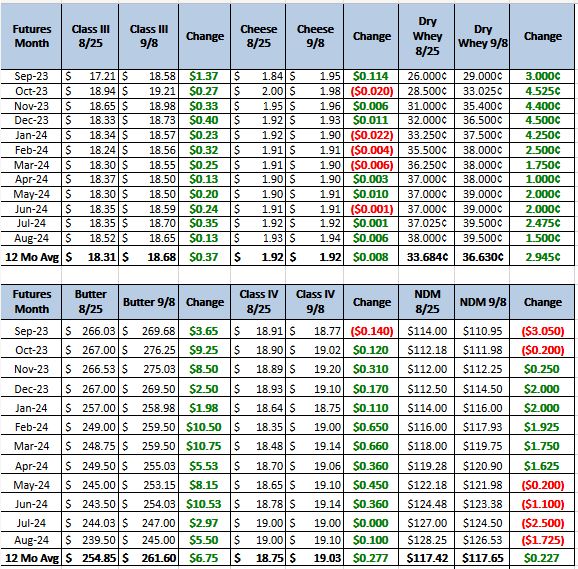

Weekly Future Prices

Cheese: In the Northeast, Class I operations are pulling on milk supplies, reducing availability for cheesemakers. Contacts in the Midwest note declining milk availability and report spot trading at $1 over Class III and higher. Meanwhile in the West, cheesemakers say milk supplies are balanced with strong to steady production schedules. Northeastern cheese production has been hampered by persistent labor issues and pauses in manufacturing over the holiday weekend. Midwestern cheese output has declined from the winter/spring months when ample milk volumes enabled cheesemakers to operate busy schedules. Some regional plant managers relay more downtime now, while others are paying higher prices for spot milk to maintain strong cheese output. Cheesemakers in the Midwest, particularly mozzarella and pizza cheesemakers, are growing more concerned with their ability to meet market demands. Restaurant demand for cheese is steady in the Northeast, while retail sales are strong. In the West, contacts report strong to steady retail and food service cheese demand. (USDA Cheese Highlights)

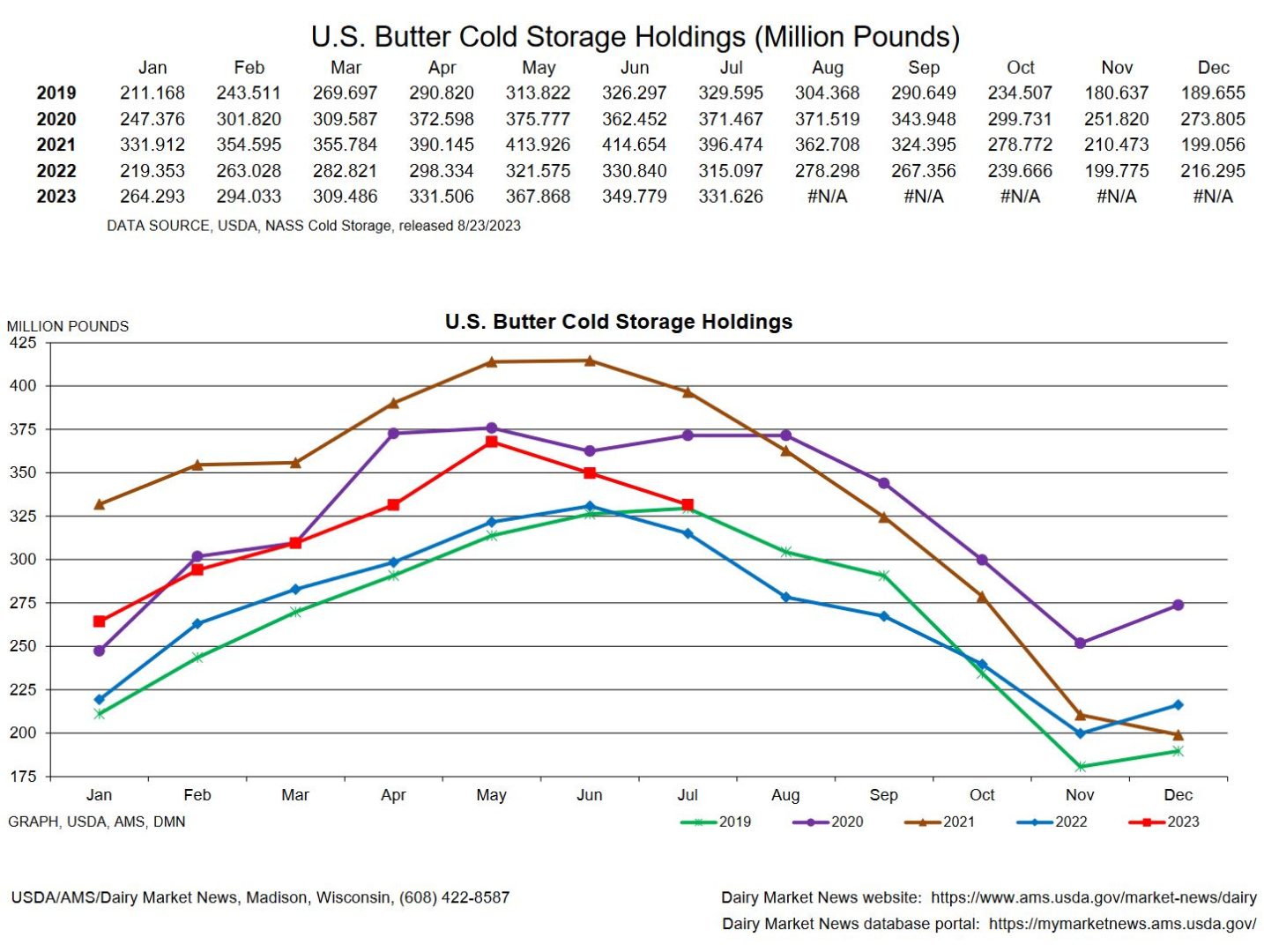

Butter: Throughout the country, cream availability picked up following the holiday weekend. However, in the Central and West regions, contacts say volumes quickly tightened as the week progressed. Some butter makers in the East report being able to operate strong production schedules this week, due to the extra loads of cream available. Others report labor issues and other obstacles have kept them from utilizing additional cream volumes. In the Central region, churning was more active this week, though some anticipate butter making to slow in the coming weeks. Western butter production is mixed, as some butter makers relay steady churning, while others say limited cream availability is preventing them from operating full schedules. Demand for butter from retail and food service customers is steady to strong in the East and West, and strengthening in the Central region. (USDA Butter Highlights)

Dry Whey: The dry whey price range contracted, and the mostly price series moved lower. Demand is steady. Stakeholders note more activity from buyers seeking out non-brand preferred loads, as well as brand preferred loads. Brand preferred trading activity is helping to minimize downward price movement on the top end of prices. Available supplies are accommodating current spot market demand. Export demand is moderate, as interest from international buyers lags interest from domestic buyers. Liquid whey volumes from cheesemakers are available to keep dry whey production schedules steady. Some processors capable of manufacturing both whey protein concentrate and dry whey, are focusing on whey protein concentrate production.(USDA Dry Whey)

Class 4 looks to be strong going into the fall. With lower production in butter powder areas and tighter cold storage butter has pushed up into the 2.70 range. This should give some support to class 3 therefore, I would keep puts and put spreads close to the money to ketch any drops in the market. Recommendation, spend 35 to 45 cents on 1850 – 1700 put spreads Dec 2023 to Jul 2024.