8/27/2023

There was no report last week do to technical difficulties. This week saw class 3 push back into the mid 18s for the next six months. This has be a place where the market has seen resistance and then tips back into the high 17s. With production tightening up and schools pulling class 1. Domestic demand is keeping cheese tight.

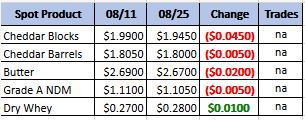

Weekly Spot Prices

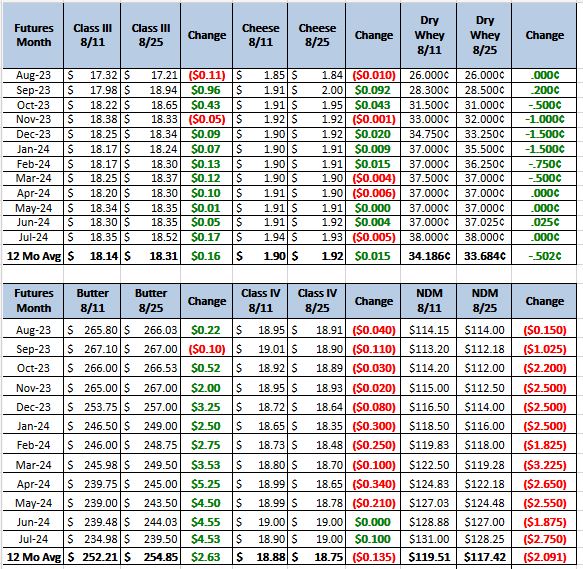

Weekly Future Prices

Cheese: In the Northeast, Class I milk processors are ordering increased, volumes reducing availability into cheese processing. Plant managers in the region suggest this, and persistent labor issues, are contributing to lighter cheese production. Spot milk prices range from at Class III to $.50 over Class in the Midwest, though some stakeholders say spot load offers have dried up in recent weeks. Some cheesemakers in the Midwest relay downtime for a day or two at plants to complete updates. In the West, cheese production is steady, and cheese inventories are available in the region. Cheese inventories are steady in the Northeast, while Midwest contacts report balanced inventories. Cheese sellers in the Midwest say demand in mid/late August is comparable to previous years. In the Northeast, contacts report stronger demand for cheddar than other American-type cheeses. Food service demand for mozzarella cheese is strong in the region. In the West, domestic demand is strong to steady. Meanwhile, stakeholders say export demand is quieter overall. (USDA Cheese Highlights)

Butter: In the West, cream volumes are tightening, and some processors say availability is on the short side. Meanwhile in the Central region, cream has become more available amid school milk cream spin off and softening Class II orders. Some butter makers in the region are sourcing cream from the West region and from locally sourced suppliers. In the East some contacts anticipate cream availability will increase in the near term. Meanwhile, regional butter makers are micro-fixing frozen bulk butter, and relying on contracted loads of cream for churning. Contacts in the Central region say butter churning is increasing. Butter makers in the West report mixed schedules as some say they are running steady or reduced production schedules, while others have stopped churning. Demand for butter is strong in the Central region, while contacts in the East say retail and food service sales are steady. In the West, demand for butter from retail and food service purchasers is strong to steady. Bulk butter overages range from 2.0 to 10.0 cents over market value. (USDA Butter Highlights)

Dry Whey: The bottom of the dry whey price range moved higher, while other prices were steady. Trading activity was reportedly quieter this week. Supplies remain available in some cases, but contacts say suppliers are not as pressured to offer loads at recent lows, such as $.19/lb and $.20/lb. Current offers are nearing or even at the $.30 mark. Limited milk availability for cheese processing, along with recently firming high protein blend markets, have created a slightly bullish safety net for a market that has been struggling to gain traction for a better part of the calendar year. Animal feed whey prices moved higher on both ends of the range. Animal feed trading was steady to slow, as demand remains hit/miss with plentiful supplies of alternative carbohydrate rich ingredients, but tones are not as bearish as in previous weeks, in general. (USDA Dry Whey)

Cheese market is steady to bullish for the present time with domestic demand taking up the slack from reduced exports. Dry whey could be key in the coming months for class 3 to break into the 19s or even 20s. This weeks updates are much improved from the last couple and if the supply of dry whey can tighten. The buyers could push this market higher. Recommendation: Buy calls or contracts on the dips in this market. Still looking for some 19s or 20s to start selling. No report next week with Labor Day weekend. If you have questions on the markets feel free to give us a call.