8/13/2023

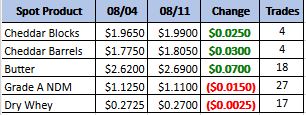

Buyers stepped in this week and move the market higher with spot block prices hitting 1.99 and spot barrel prices reaching 1.825. Up dates this week note slowing demand at these prices, especially for the export market. Milk volumes have also come down as heat and lower cow numbers start to take effect. Schools are also opening back up which means more milk flowing into class 1. The market looks to hold these new price levels into the fall.

Weekly Spot Prices

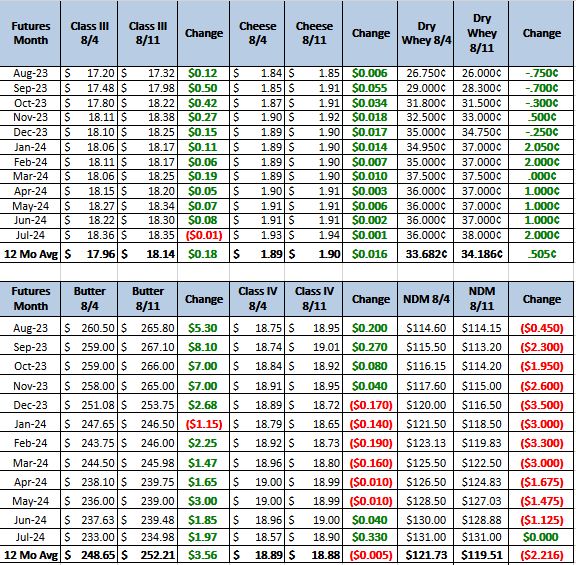

Weekly Future Prices

Cheese: Class III spot milk prices in the Midwest were reported from Class up to $2 over Class during week 32. This marks the first week of the year in which no prices below Class were reported. Seasonal milk tightness is being reported across the regions, but Western cheesemakers relay they are still taking in enough spot milk to keep somewhat steady production schedules. Cheese demand varies. Some cheesemakers say the recent bullish run on the CME cash markets has slowed buying. Demand is noted as steady rather than slow, nonetheless. Barrel cheese loads are more accessible than their block counterparts, which has manifested in a roughly $.1650 margin on the CME spot call. Still, in general, market tones are viewed bullish to steady for the near-term. (USDA Cheese Highlights)

Butter: Cream availability remains tight across the country. In the Northeast, contacts say that they are relying on contracted loads of cream and micro-fixing bulk butter that was frozen earlier in the season in order to meet demand. In the Central states, many butter processors relay that the cost of spot loads of cream is curtailing spot purchasing and that they, too, are relying on contracted loads of cream and micro-fixing. In the West, cream is tight albeit generally more available in the Pacific Northwest than in the southern parts of the region. Contacts state that salted butter is more of a manufacturing focus at the moment, which has caused some unsalted butter inventories to wane. Retail and food service demands are unchanged. Bulk butter overages range from 2.0 to 10.75 cents over market value. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved higher across all facets of the range and mostly price series. Demand is moderate. Stakeholders indicate less hesitation by purchasers to secure loads beyond their immediate needs. Demand is mixed, with some noted upticks in interest from Mexican and South American purchasers. Loads are available to accommodate current demand. Some manufacturers report ample amounts of liquid whey from cheese production are available to accommodate steady dry whey production, despite seasonally declining milk output. (USDA Dry Whey)

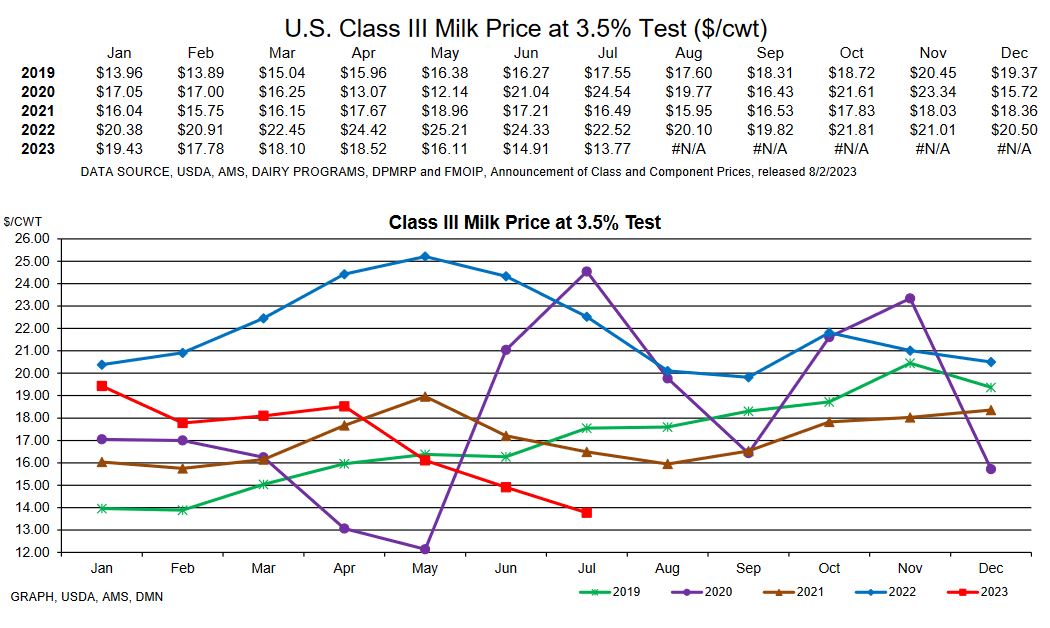

With production dipping lower I and spot loads of milk moving higher the lows should be in for this year. That is not to say there will not be some pull backs. Current spot prices are above world market which has begun to erode exports. Good domestic demand as well as continued strong exports to are neighbors to the south should lend support to these markets. Recommendation: buy calls on pull backs in the market, 1900 calls for 40 cents for the next 6 months.