8/5/2023

Buyers and sellers have both stepped back from the spot market as lighter trade left the markets moving sideways. From reports of tighter 30 day old cheese and prices above the world market this is expected. Continued reports of high cull rates with beef prices sky high I expect to see the dairy herd to continue to shrink. This combined with hot weather as we move through august, milk production will start to tighten up class 3. Therefore, the market should remain supported into the fall.

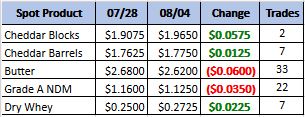

Weekly Spot Prices

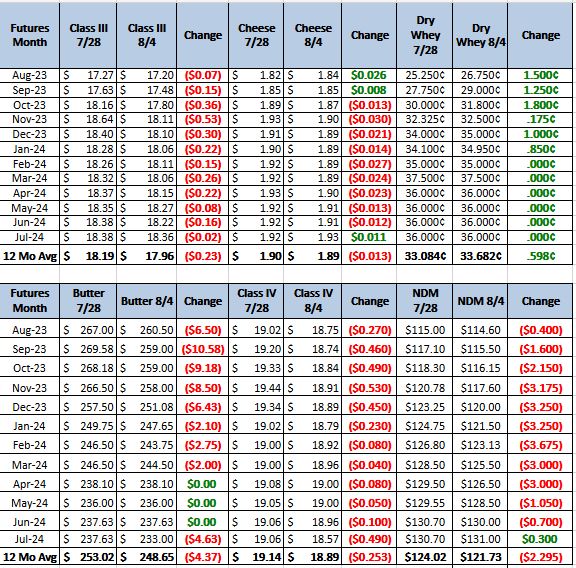

Weekly Future Prices

Cheese: production has declined in the Northeast, amid reports of declining milk output. Milk availability is declining seasonally in the Midwest. Contacts in the region report Class III milk loads are no longer trading at discounts of $10 to $11 under Class, but say volumes are moving for around $2 under Class III. In the West, demand for Class III milk is strong, while milk availability is tightening, but cheesemakers relay volumes are sufficient for strong to steady cheese production. Domestic demand for cheese is noted as strong in the West, though contacts report cheese blocks sales are healthier than barrels. Export interest from the region is mixed. Demand for cheese is steady from retail and food service customers in the Northeast, and cheddar cheese interest is greater than other American-type cheeses. Contacts in the Midwest say cheese is moving steadily to contract and spot purchasers. Cheese inventories in the Northeast and West are available to meet current market demands. (USDA Cheese Highlights)

Butter: Cream availability is tightening throughout much of the U.S., and butter makers in the Central region report finding volumes at or below a multiple of 1.30 is becoming more difficult. Eastern butter makers say they are relying on loads of contracted cream for churning, and some note they are micro fixing bulk butter inventory which was frozen earlier in the season. In the West, butter production is strong, though some manufacturers report running lighter production schedules. Demand for butter from domestic purchasers in the region is strong to steady. Contacts report light export interest in butter, but some say interest from purchasers in Canada is improving. In the East, demand for butter is steady from retail and food service customers. Contacts in the Northeast and Central regions say butter inventories are tightening. Butter makers in the West say current cream multiples are encouraging them to build butter inventories for later in the year. Bulk butter overages range from 2.0 to 12.5 cents over market value. (USDA Butter Highlights)

Dry Whey: prices moved down on the top end of the range and moved up on the bottom end. Dry whey demand is steady to moderate. Industry sources indicate less hesitation by purchasers to focus only on loads meeting their current needs and securing loads for additional storage. Manufacturers note demand from Mexican and South American purchasers is showing upticks, but demand from Asian purchasers is light to quiet. Loads are available for spot purchasing. Although milk output is decreasing, enough Class III milk volumes are available for cheese makers to keep strong production schedules, leaving ample amounts of liquid whey for steady production schedules to be accommodated. (USDA Dry Whey)

With milk production dropping especially in the butter powder areas class 4 should stay strong. June had one of the strongest draw downs in butter in recent years; this despite the US having one of the highest prices on butter in the world. Milk should continue to flow toward class 4 which will contribute to tightening class 3 as long as demand remains strong. Recommendation this week by calls Oct 23 through Mar 24. $20 calls for an average of 40 to 50 cents. Then put sell orders in at the same levels.