7/29/2023

Some support showed up in the futures market this week. After last weeks jump there was some skepticism that prices would hold this week. Cash took a dip in prices but ended the week on a positive note with loads trading hands at higher prices. Volume has decrease the last two weeks on the spot market that last couple of weeks allowing the buyers to push and hold prices higher. Hot weather and the potential for lower milk production is a contributing factor. Whey is the only weak spot with it trading in the mid 20s.

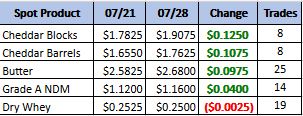

Weekly Spot Prices

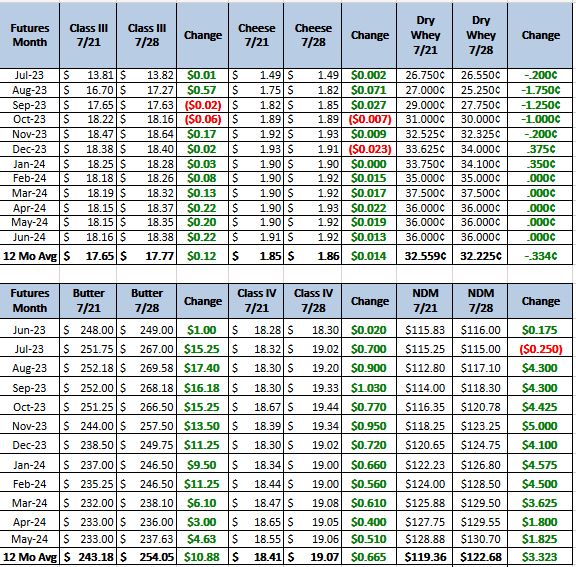

Weekly Future Prices

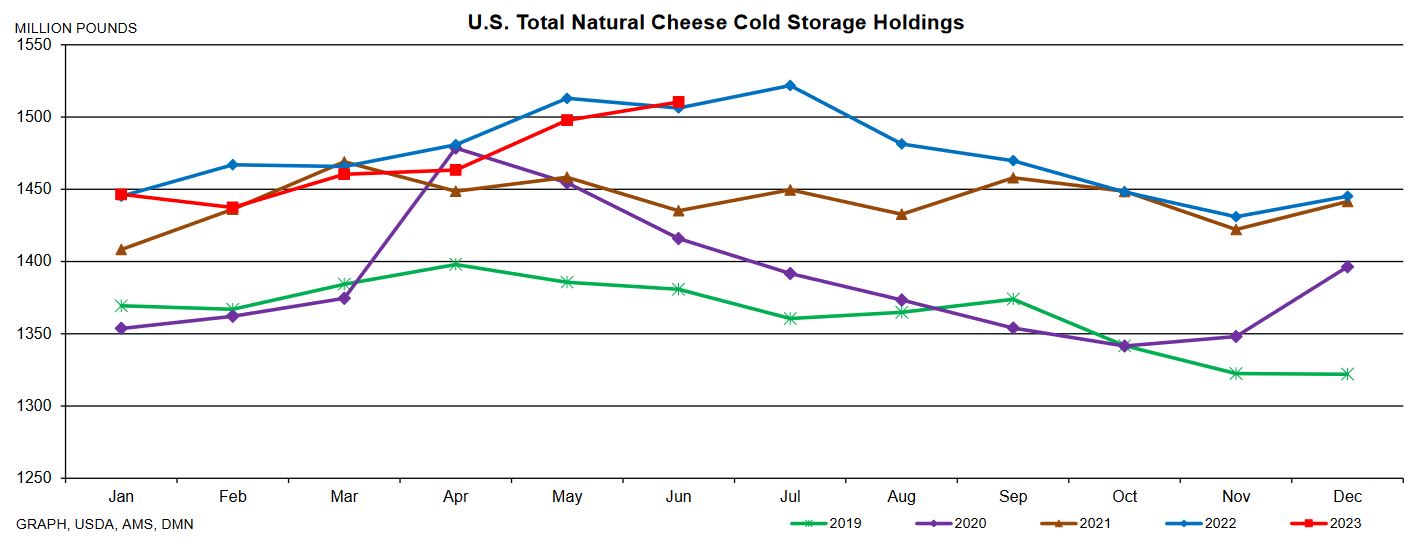

Cheese: Cheesemakers in the Northeast say production has plateaued, as milk output is declining in the region. In the Midwest, cheesemakers are operating strong production schedules, though some have reported downtime at plants this week. This downtime has contributed to some milk availability, while overall milk production is declining in the region. Spot milk prices in the Midwest range from $5 to $3 under Class III. In the West cheesemakers note declining milk availability but say supplies are available for strong to steady cheese production. In the East and Midwest, contacts report strong cheese demand. Export sales of cheese are mixed in the West, as contacts report steady interest from purchasers in Mexico but note some hesitation in Asian markets. Cold storage space has become more available in the Northeast in recent weeks, and contacts in the Midwest say loads are moving quickly. Spot loads of cheese are available in the West. (USDA Cheese Highlights)

Butter: In the East and Central regions cream availability is tightening. Contacts in the West report cream is more available than in other regions, but say temperatures are increasing in the northern parts of the West and are contributing to a reduction in excess cream volumes. Butter production is mixed in the West, as some manufacturers note light production schedules, while others say they are steadily churning. East region butter makers are running active production schedules, while some butter makers in the Central region report scheduled down time at plants this week. Butter inventories are tightening in the Central region amid strong demand from retail and food service customers. In the East, increased market activity is starting to chip away at butter stocks, but contacts note inventories remain ample. Demand for butter is steady from retail and food service customers in the East. Some contacts in the West say they are building inventories ahead of the baking season. Export demand for butter is light in the West, while retail sales are steady, and food service demand is strong. Bulk butter overages range from 0 to 12.5 cents over market value. (USDA Butter Highlights)

Dry Whey: Price range contracted and moved higher on both ends this week. Demand for dry whey is steady to moderate. Stakeholders relay purchasers are focusing orders on loads meeting their current needs and hesitant to secure loads for additional dry whey storage. Manufacturers relay demand from Mexican purchasers is picking up, but Asian purchasers are only lightly active. Loads are available for spot purchases. Although milk output is seasonally declining, ample volumes of Class III milk are available for cheese makers to run strong to steady production schedules, leaving ample amounts of liquid whey to accommodate steady dry whey production. Prices for: Western U.S., All First Sales, F.O.B., Extra Grade & Grade A, Conventional, and Edible Dry Whey. (USDA Dry Whey)

Milk production has started to drop but cheese production has still been running strong. Last weeks and this weeks strength have been based on what market participants have been looking for in the future. With heat and lower cow numbers the expectation is that milk for cheese plants will tighten, therefore tighten cheese availability. This is a good possibility as long as demand does not falter. Recommendation, this week. cover half your needs with put spreads or drp for the next 6 months. Buy $18 put sell the $17 put for 35 cents Oct. 23 – Mar. 24.