7/23/2023

Some life in the class 3 market. This week saw the biggest jump in the class 3 market in months. This was mostly do to spot cheese this week which went up 28 and 24 cents in blocks and barrels. The spot market also saw lower volumes this week than the last couple of months. 18 loads for blocks and 12 loads for barrels, this compared with the 40 to 60 loads per week we have seen for the last couple of months. This points to some of the sellers finding alternative markets to sell their cheese than dumping it on the CME. All in all a positive week for class 3.

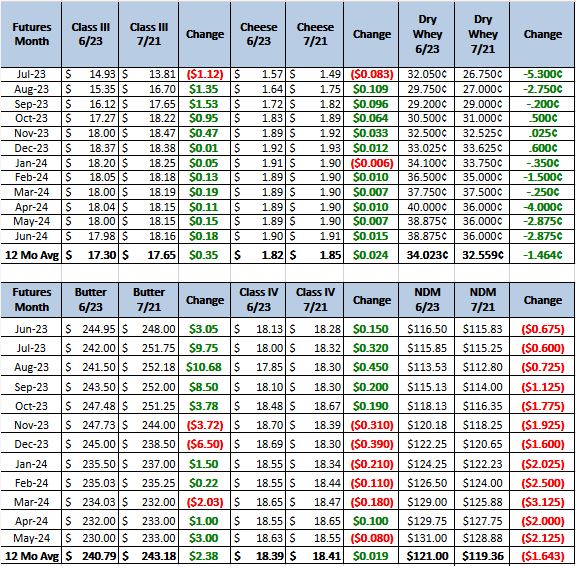

Weekly Spot Prices

Weekly Future Prices

Cheese: Cheesemakers in the Northeast say milk volumes are tightening as hot, humid weather, and heavy rain are having a negative impact on milk production and cow comfort. In the Midwest and West, contacts note declining milk production, though cheesemakers say volumes are available for cheesemakers to run steady production schedules. Some cheesemakers in the Midwest say plant downtime is contributing to spot availability, as milk is trading between $7 and $3 under Class. Cheese inventories are strong in the Northeast, and contacts in the West say spot loads are available to meet current market demands. Cheese availability varies in the Midwest, though some cheesemakers say they are rapidly selling any extra loads produced. Contacts report somewhat strong demand for cheese in the region. In the Northeast, contacts report steady demand from retail and food service purchasers. Higher restaurant menu prices are, reportedly, deterring some potential customers. (USDA Cheese Highlights)

Butter: Cream availability for butter churning is declining across the country. Contacts in the East and Central regions note ice cream makers are pulling on supplies, while warm weather is having an impact on cream supplies in the Central and West regions. Some butter makers in the Central region say they are churning lighter schedules due to scheduled maintenance in recent weeks. In the East and West, butter makers are running steady production schedules. Butter inventories are growing in the West, though availability varies by location and butter types. Inventories are steady in the East, while bulk butter buyers in the Central region relay tightness in the market. Demand for butter is steady from retail and food service customers in the East. Central region contacts report an uptick in food service sales and say retail buyers are active. In the West, domestic demand is solid, but interest is light from international purchasers. Bulk butter overages range from 0 to 10.5 cents over market value. (USDA Butter Highlights)

Dry Whey: Prices continued to slip on shaky market tones. Block volumes are changing hands at lower prices, while domestically prices are still trading in the mid- to mid/upper $.20s. Some Southeastern Asian purchasing activity is expected, as market prices continue to struggle out of what many contacts expect to be basement level pricing. Milk availability is slowly starting to tighten up. Milk is being hauled from the upper Midwest to the Southern U.S., where summer heat is playing a strong part in stifling farm milk production. Still, cheesemakers report that whey interests is week. Animal feed whey prices moved lower on both ends of the range on slow to steady trading activity. Market tones remain under notable pressure, but some contacts on the sell side are hopeful that seasonally lower milk output will eventually translate into heartier dry whey markets. (USDA Dry Whey)

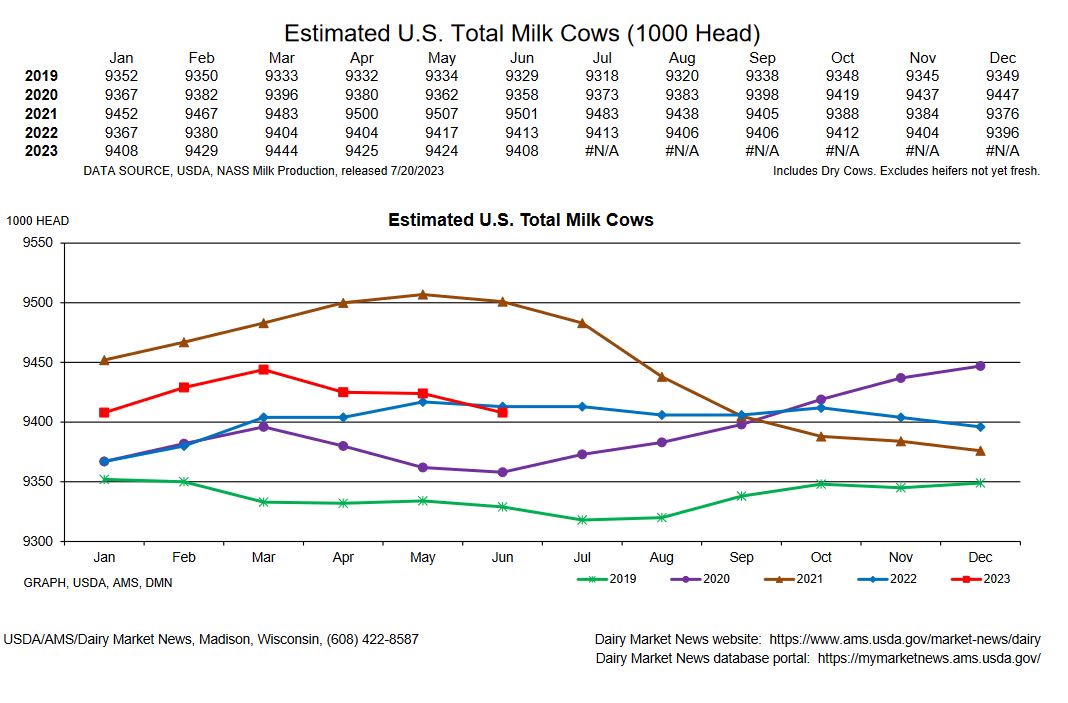

Cow numbers have truly started to drop. Milk production has flattened being up only .2 percent in June. I expect with the heat in July there should be a significant drop in production for July. All this saying it looks like Class 3 is finally starting to turn a corner. There still may be some bumps on the road with Cold Storage out this next week, but I do not see this market returning to its lows. Recommendation, by calls on pull backs. The market jumped hard this last week and sent option prices sky rocketing. I do not expect class 3 to continue this trajectory. With whey still in the mid 20s it is going to take 2.20 cheese to get back to $20 class 3. That is quite a bit higher the the rest of the world right now.