5/20/2023

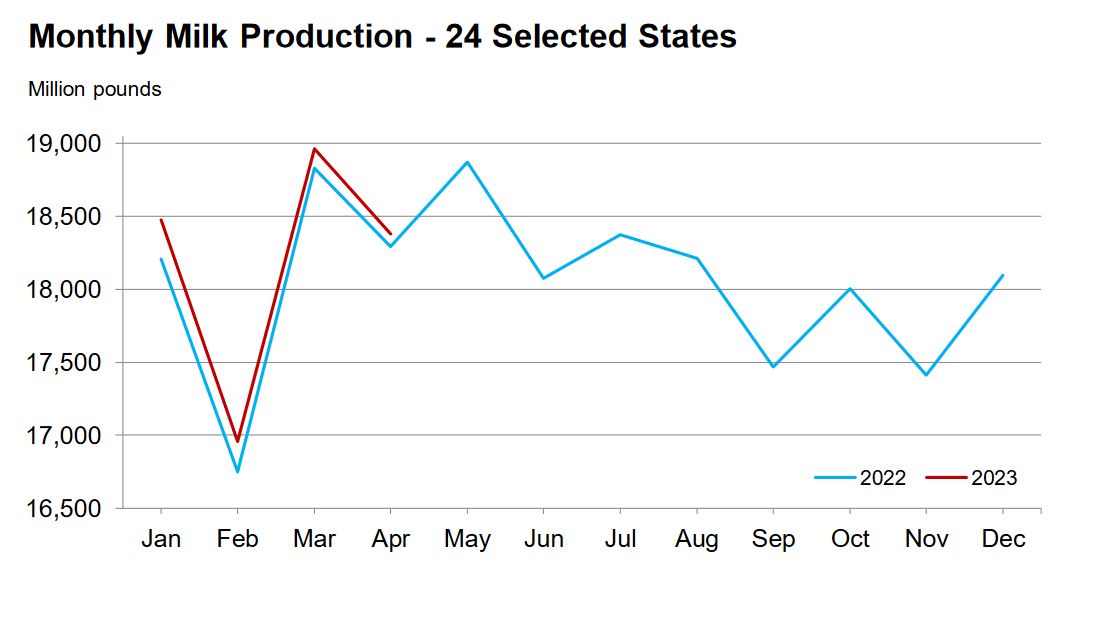

Spring flush is starting to ebb on the coasts but in the Midwest extra loads of milk are still trading at $4 to $11 under class. This has been the theme this spring driving the spot prices down and class 3 calculation to the $14 range. As grilling season starts and summer vacations get underway, I expect to see a slight uptick in demand. Although, to real move the needle there needs to be a drop in production. Production was up 0.5 percent for the 24 major milk producing states, and up 0.3 nation wide. This was inline with expectations and should be supportive at current prices.

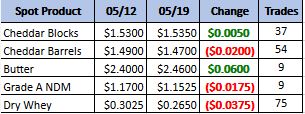

Weekly Spot Prices

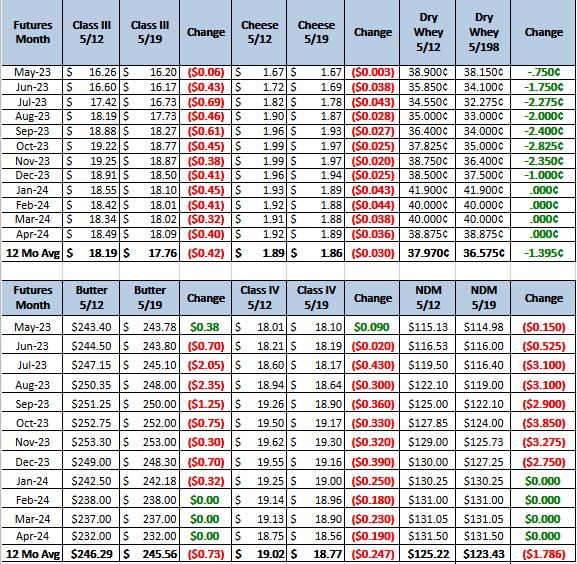

Weekly Future Prices

Cheese demand is mixed by region and by cheese variety, but more contacts are suggesting improvements in demand, particularly from the retail sector. Grilling season is noted as being a catalyst for improved retail sales. Midwestern cheesemakers say curd sales have yet to lift much, but processors are expecting some seasonal upticks to come near term. Milk remains widely available in all regions, particularly the upper Midwest, where spot milk prices ranged from $11 to $4 under Class III, compared to 2022 during week 20, when prices ranged from $2.50 under to $.75 over Class. Cheese market tones are under some continued bearish pressure. (USDA Cheese Highlights)

Butter: Cream supplies are heavy and readily available for production needs in butter making facilities across the regions. Manufacturers’ in-house cream supplies are prompting seven- day production schedules in some instances, but personnel shortages constrain plant production capacity in the West region. With the heavy availability of cream supplies, manufacturers are taking advantage of the opportunity to produce and store bulk butter, as the market currently see bulk overages ranging 0 to 10 cents above the market. Butter demand is steady for both domestic and export markets, as seasonal baking needs boost retail butter interest. Meanwhile, food service demand is seasonally steady. (USDA Butter Highlights)

Dry whey prices moved lower on the bottom of the range and top of the mostly series this week. Demand notes vary and there are potentially some bullish indicators in regards to export markets, however current demand is, at best, steady as supplies are noted as plentiful. Milk output has been mixed in the West, but plentiful in the Midwest for Class III operations. Demand notes for higher protein concentrates has improved according to some processors, but prices have yet to increase much, as inventories of WPC 80% have held somewhat steady this spring. Market tones, at least currently, remain under a somewhat persistent bearish raincloud as CME prices reached sub-$.30/lb this week. (USDA Dry Whey)

Going from last year at all time highs to this year of net losses on par with some of the worst years on record. What changed? Looking at the graph it should not be milk production, but that is part of the story. The last jobs report has the unemployment rate lower then last year. And reports on demand for dairy are similar to last year. Out look is the major change. Inflation has had another year to bite into everyone’s pocket book. Therefore, the perception that it does not matter what it costs we have to have it is gone. This has left end users with a bigger concern of sales, where last year it was inventory. This has turned the spot light on the over production which we had last year. Demand does not look like it is going to bail the market out this year, so it will likely take a production drop to move prices back into the profitable range. Summer heat is predicted but when it hits will be the million dollar question. Recommendation, buy puts in the front months, June – August.