5/14/2023

The good the bad and the ugly. Not just an old Clint Eastwood movie, this also describes the dairy market lately. The good; demand, domestic demand has held strong and exports are moving pretty good volumes out of the country. The bad; production, for most of the spring there has been record discounts on milk because of over production. The ugly; price, the class 3 price has dropped to a level that most dairy farmers are lousing money. At the end of the movie the good does prevail but it is a long move. As the cull rate goes up and spring flush starts to subside we should see production come down and then the price will move higher as long as demand stays standing strong. It may take a little longer though.

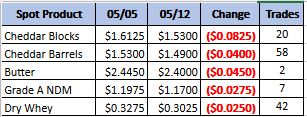

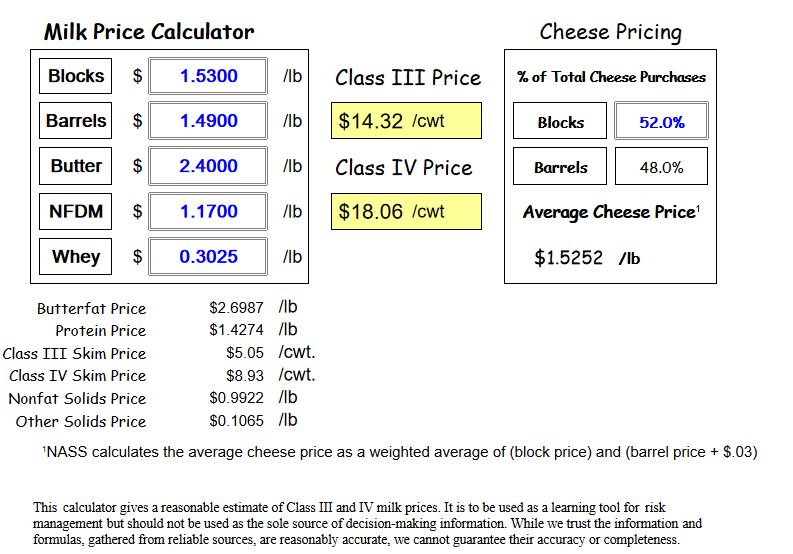

Weekly Spot Prices

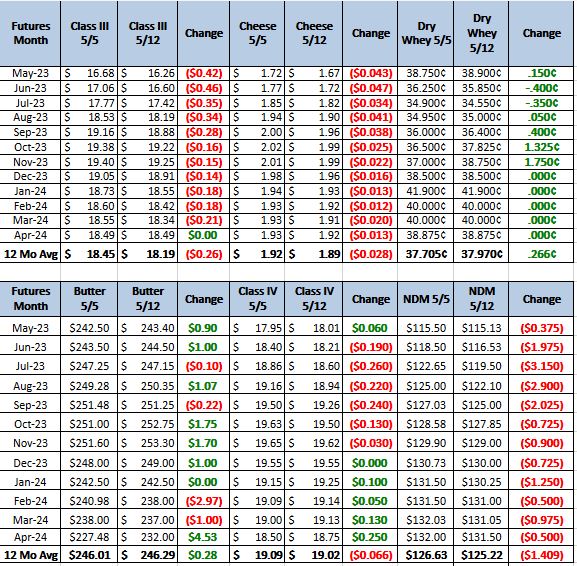

Weekly Future Prices

Cheese: Milk remains widely available for cheesemakers throughout the country. Spot milk prices reached $12 under Class III for Midwestern cheesemakers. Last year, during week 19, the spot milk load price low was $2.50 under Class. Some milk sellers say processors will not take on spot milk offers unless the price is below $7 under Class. Cheese demand is variable. Food service ordering is expected to slow down later this spring, as school districts begin their hiatuses. Grilling season is coming on soon, though, which is expected to benefit some retail focused cheese processors. Some plant managers continue to report scheduled downtime, while others are busily running through notably available milk stores. (USDA Cheese Highlights)

Butter: Butter manufacturers have plenty of cream available to keep butter churns busy, with some manufacturers operating seven days a week. Inventories reportedly continue to grow in the East. However, a few contacts report production is being limited due to personnel shortages in the West. Retail and food service demand is firm overall, with steady draws on inventories from contract sales. That said, some central stakeholders report demand as lackluster. Loads are available to accommodate current spot market demand. Some stakeholders report production schedules shifting from unsalted butter into salted butter production, while others report more bulk butter moving into the freezer. Bulk butter overages range from 0 to 12 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: prices continued to slip in most facets this week. There are some brand preferred loads trading hands at and around $.40, but most trading is now taking place throughout the $.30s. Traders are reportedly actively buying loads at current rates on the CME spot call. Specifically branded loads are still being offered in the low/mid $.40s. There is plenty of milk for processing, and moving through Class III plants. Animal feed whey trading is moderately active as prices moved lower, mirroring those of edible grade whey. End users are reportedly taking a sideline role to wait out further price pressure. Clearly, bears are overshadowing bulls on dry whey market tones. (USDA Dry Whey)

Spot price hit numbers this week that we have not seen for a couple of years. With cost of production still at elevated levels these numbers will do some serious damage to the dairy industry if reached. With that in-mind staying at these levels is unlikely. Recommendation this week, by puts on the front months and switch to call as you move out. I like the Aug 1900 call for 40, Sep 1950 call for 40.