6/2/2023

There was no report last week hope everyone enjoyed their Memorial Day weekend. Dairy markets this week are still reporting spot loads for milk going for 12 to 4 dollars under class. With an abundance of cheap milk out there price action continues to get depressed. This has been the over riding theme this spring, and as we go into the summer it is still controlling the market. I am not expecting much of a rally on milk prices until the discount milk goes away.

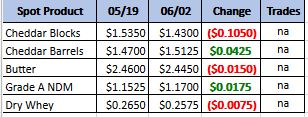

Weekly Spot Prices

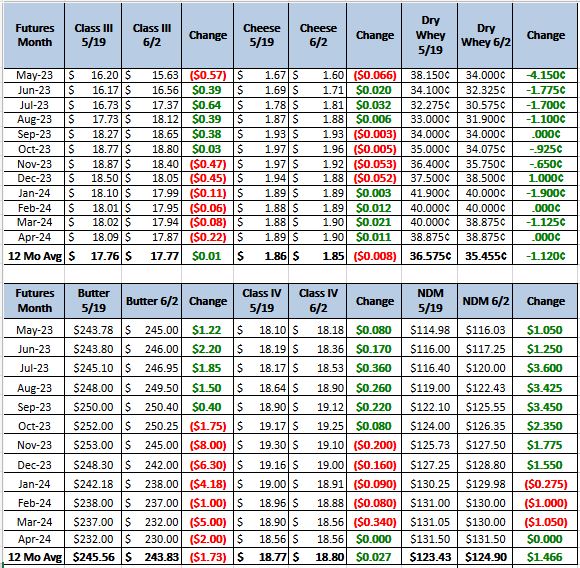

Weekly Future Prices

Cheese: Milk is available for cheesemaking throughout the country. Contacts in the Midwest report spot loads of milk moving from $12 to $4 under Class III. In the Northeast and West, cheesemakers report scheduled downtime for the recent holiday weekend. In the Midwest, cheese production is strong as some manufacturers in the region worked through the holiday weekend. Demand for cheese varies throughout the regions. Northeast stakeholders relay strong retail demand and moderate food service sales, while demand is mixed in the Midwest, and softening in the West. Inventories of cheese are strong in the Northeast, and some contacts report difficulty moving excess inventories of certain varieties. Cheese inventories are available to meet demand in the West, though block inventories are slightly looser. In the Midwest, cheese loads are moving somewhat briskly. (USDA Cheese Highlights)

Butter: Cream is available throughout the country. Some contacts in the West say plant downtime has contributed to more cream loads available on the spot market this week. In the Central region, butter contacts say warmer temperatures and increased Class II processing are expected to contribute to lighter cream availability as summer nears. Butter makers in all regions reported some downtime during the recent holiday weekend, though in the East and Central regions, stakeholders relay operating busy production schedules through the remainder of the week. Demand for butter is steady in the Central region. In the West, contacts note steady retail demand and strong to steady food service sales. Meanwhile in the East, demand is mixed with contacts reporting strong retail demand, but more moderate demand from food service purchasers. Bulk butter overages range from 0 to 10 cents over market value. (USDA Butter Highlights)

Dry whey prices moved lower on the top end of the range, and lower on the bottom end of the mostly price series. Brand specific loads are holding some firmness at or near the top end of the price range/mostly price series. Inventory is indicated as available to meet current contract obligations and moderate spot market interests. Demand from international purchasers is mixed, with industry sources indicating both slight upticks and slight downticks in activity. Class III milk volumes are strong and cheese manufacturers are running steady production schedules, making plenty of liquid whey available for drying. Some processors note demand for higher protein concentrates is improving, but prices have not followed suit, which is contributing to steady dry whey production. The CME daily cash call remains under the $0.30/lb mark this week and market tones are somewhat bearish. (USDA Dry Whey)

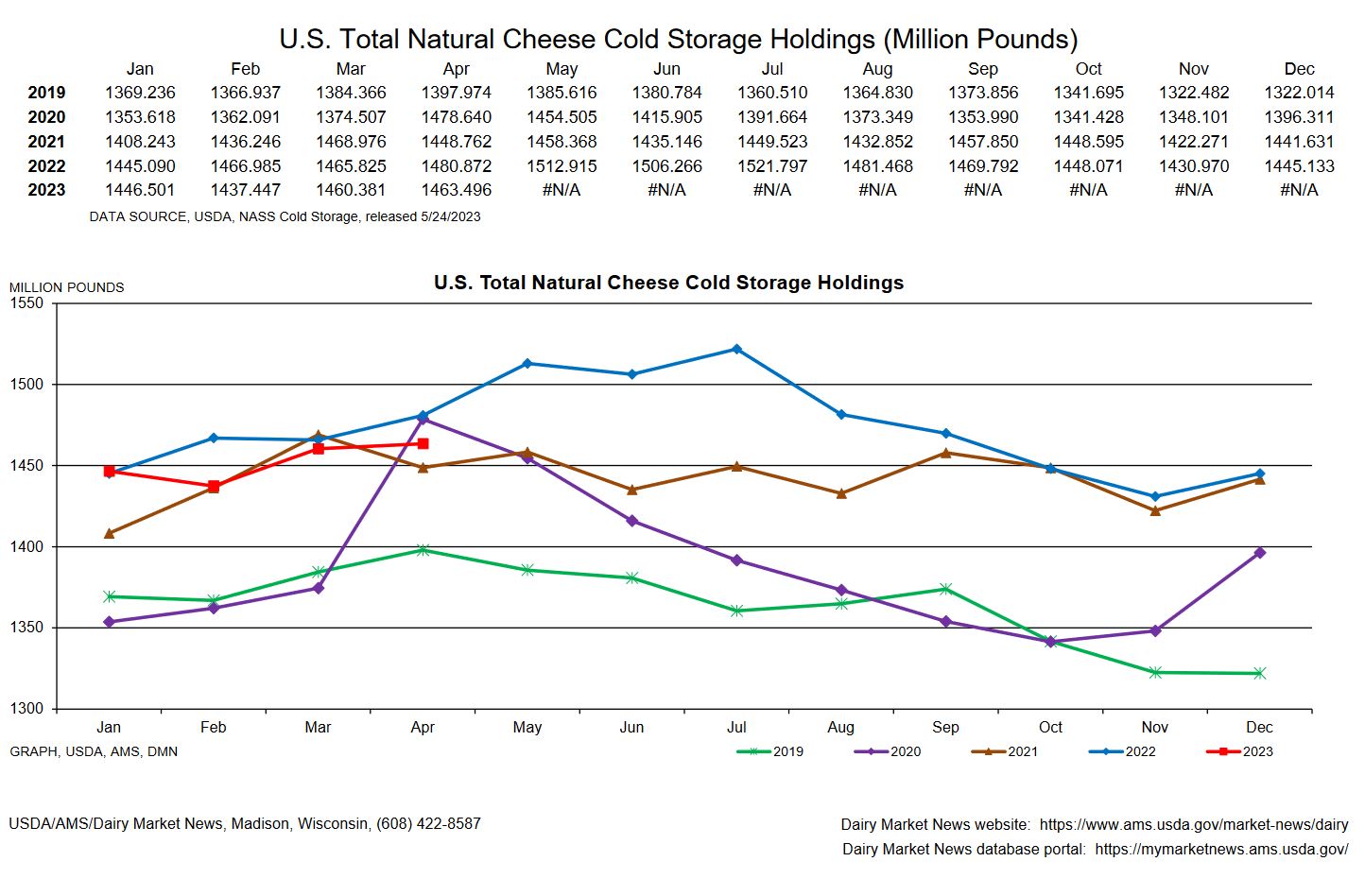

The market is just not able to break out of this bearish trend we have been in this year. There have been a few false starts but those have been brought back down with discount cheese getting dumped on the market. The good news of not sitting on that cheese is that cold storage is still bellow last year. That means demand is using up the cheese we are producing and all it will take to move the needle in the other direction is for this excess milk to dry up. Recommendation this week is to by put spreads to keep the market from moving lower with out spending to much.