4/01/2023

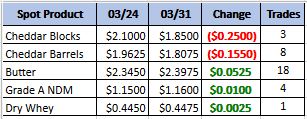

The good time are here to stay forever. Sorry, bad April fools joke. The spot market came crashing back down this week. The blocks gave up 25 cents and the barrels gave up 15.5 cents. That is a major move for one week, especially as there were no major reports for dairy this week. Inexpensive milk is making cheap cheese which is allowing manufacturers to bring cheese to the market with less concern to what price they are getting for it. This is making for a very volatile market.

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk is available for strong cheese production in the Northeast and West. In the Midwest, milk remains accessible, though availability varies in different locations. Cheesemakers in the region are running active production schedules, and some say they are operating six to seven days a week. Demand for cheese varies throughout the Midwest. Domestic demand for cheese is steady in the West, and contacts report strong sales to customers in Asian markets. Some western contacts note export demand to other regions is steady to softer, as cheese produced domestically is priced uncompetitively compared to cheese produced in Europe and Oceania. In the Northeast, demand for cheese is steady to strong from both retail and food service customers. Cheese inventories are steady in the Northeast and available to meet current spot purchasing demands in the West. (USDA Cheese Highlights)

Butter: Cream is available for butter production in the Central and West regions, while availability varies in the East. Contacts in the East say spring flush will relieve the current tightness of cream for butter makers present in some parts of the region. Butter production is mixed in the East as some manufacturers say they are steadily churning, and others say labor shortages are causing them to operate reduced production schedules. Butter makers are actively churning in the Central region, while production is steady to strong in the West. Demand for butter is softening in the Central region following more active sales in late February and early March. A combination of strong production and softening demand is contributing to growing inventories in the Central region. In the East, demand for butter is steady to increasing from both retail and food service customers. Contacts in the West report steady retail demand but softening food service sales. Asian purchasers are actively ordering loads of butter from the West. Bulk butter overages range from 0 to 10 cents above the CME market value, across all regions. Across all regions, bulk butter overages range from 0 to 10 cents above market. (USDA Butter Highlights)

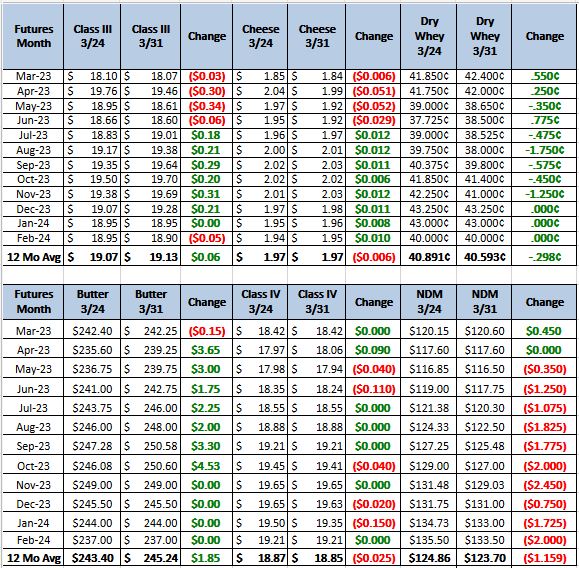

Dry whey: The bottom of the range moved lower this week. Stakeholders continue reporting higher inventories. Additional loads are available for contract sales, but stakeholders note lighter interest for contract volume past Q2 thus far. Spot markets kept moderate activity. Market tones have not pulled away from a slightly bearish outlook. The dry whey price on the CME decreased by less than 1 cent for the second week in a row, since March 15, to $0.4425. Overall, export demand from Mexico and Asian countries remains steady to light, despite industry sources indicating February was less active compared to January. Current prices and inventory levels for high protein whey concentrates keep some stakeholders shifting production schedules into dry whey. Plenty of liquid whey is available for drying from cheesemakers running strong to steady production schedules. Dry whey production is steady. (USDA Dry Whey updates)

Cheep milk continues to flow into manufacturing. This has jumped the cheddar cheese production and created a lot of volatility on the spot market. Cheddar cheese production form December 2022 to January2023 is the biggest jump in the last 5 years for the same time of year. The expectation for 2023 is that milk production will come down and therefore, the cheap milk that is making some of this extra cheddar cheese will not be there. Recomondation, buy calls on drops in the class 3 future prices. $21 calls from June 23 to December 23 in the 30 to 50 cent range. There will be no report next week for the Easter Holiday weekend.