10/30/2022

Three weeks of negative pressure has turned class 3 milk into a bear. We had cold storage out this week which it was still up from last year but a good draw down from last month. Europe’s milk production has moved higher despite reduced feed and environmental hurdles they are having to jump over from governmental regulation. This has cooled international prices and even though exports are still good, this has helped pressure the US market lower.

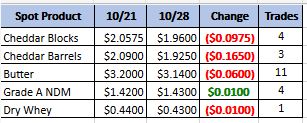

Weekly Spot Prices

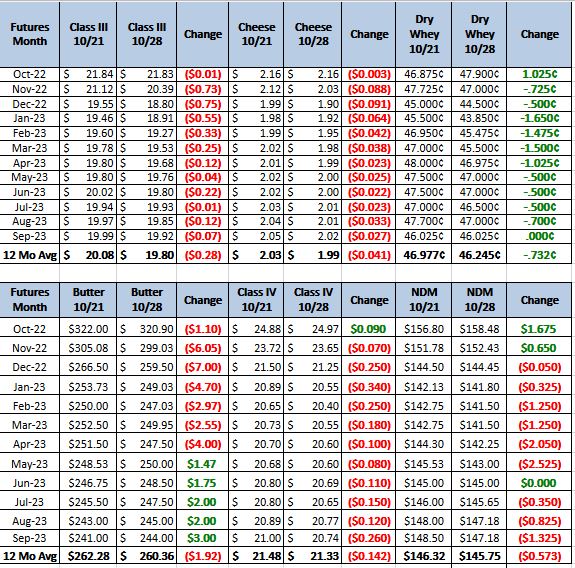

Weekly Future Prices

Cheese: Cheese production is steady in the Northeast and West, though some plant managers in these regions say they are running below capacity due to supply chain delays and staffing shortages. In the Midwest milk production is increasing, seasonally, which some cheese makers say will increase availability in the coming weeks. In the Northeast and West, food service demand is steady though retail demand is noted by stakeholders as softening. Cheesemakers in the Midwest say demand is strong for retail cheddar and Italian style cheese. Export sales of cheese are strong in the West, where stakeholders say Asian buyers are purchasing loads to ship in Q2 of 2023. Some Northeastern cheese contacts say internationally produced loads of cheese are becoming cheaper, and they relay a concern that this may negatively impact export demand. Spot loads of cheese blocks are available in the Northeast and West. In the Midwest, some cheesemakers say their inventories are committed through the rest of the year. Meanwhile, some process cheese manufacturers in the region say inventories are becoming more available. Some cheese makers in the West say increased barrel production and spot availability have contributed to lower CME market prices since last week. (USDA Cheese Highlights)

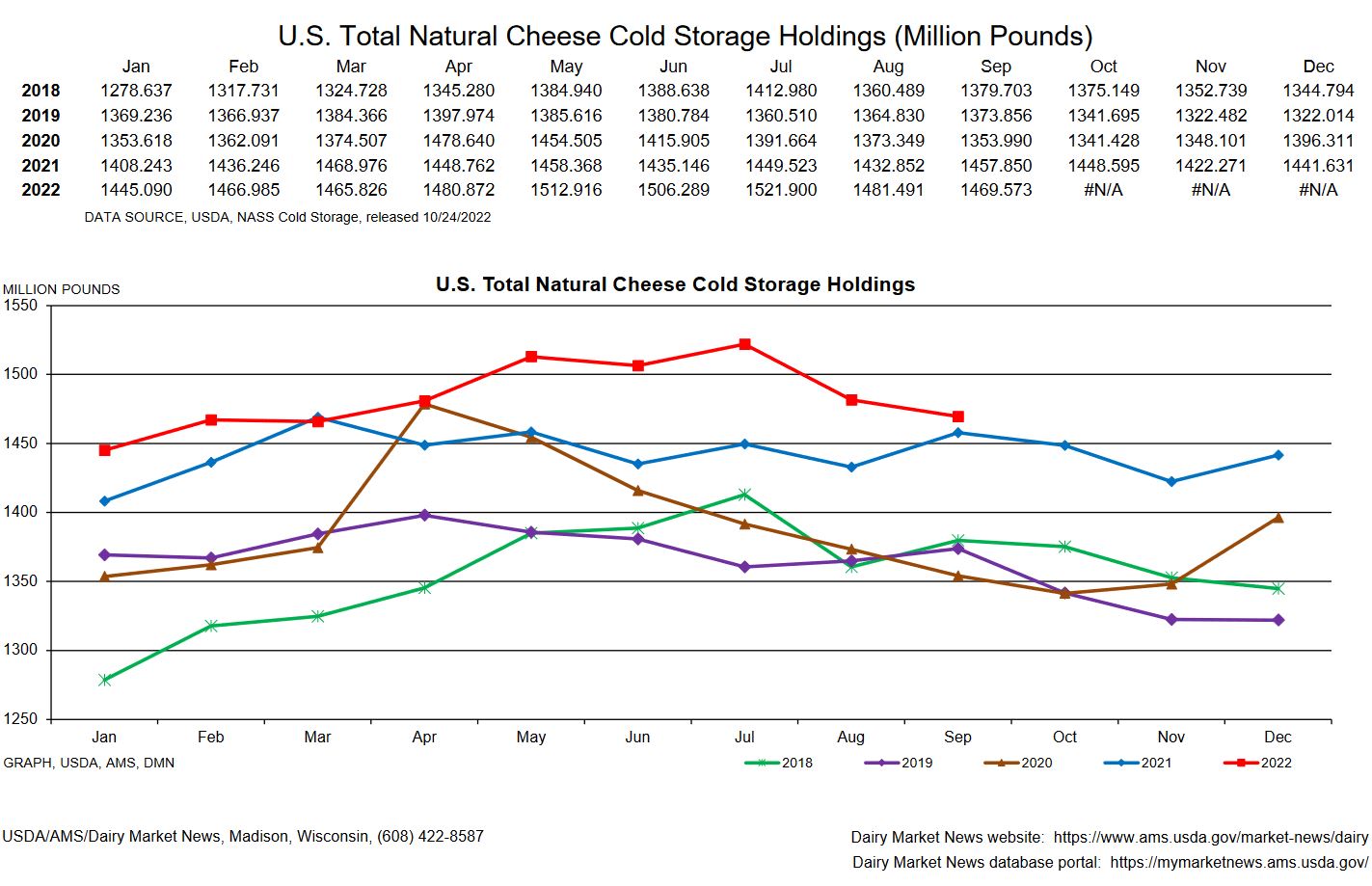

Butter: In the Northeast and West, cream is becoming more available for butter churning. Contacts in the Central region say cream availability is down from the last two weeks, but handlers say they anticipate cream to remain available through the end of the year. Butter makers are increasing their churning in the Northeast and Central regions. Butter production is steady in the West. Some butter manufacturers in the Northeast say they have no extra butter currently. Butter inventories remain tight in the Northeast and West. In the Central region contacts say butter inventories are growing. In the NASS Cold Storage report released October 24th, September inventories were noted as down 4% from August. Some contacts in the West say this decline was smaller than they expected and may contribute some bearishness to domestic butter markets. Central region butter makers say demand is strong even while butter has reached near-record prices in the last month. Retail and food service demands for butter are strong in the Northeast and West. Bulk butter overages range from 5 to 20 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: The dry whey price range and mostly price series were unchanged at the top. The bottom of the range moved higher, while the bottom of the mostly price series moved lower. Dry whey demand is steady in domestic markets. Some stakeholders say interest in dry whey is below previously forecasted levels. Contacts report steady to lower demand from international purchasers, as increased COVID restrictions are limiting some exports to Asian markets. Dry whey production is steady but limited, as some drying schedules are prioritizing the production of higher whey protein concentrates and permeate. Some plant managers also say labor shortages and delayed deliveries of production supplies are preventing them from running full schedules. Spot inventories of dry whey are available for purchasing. (USDA Dry Whey updates)

Cold Storage

Cash has dropped hard in the last couple of weeks as both blocks and barrels pushed under $2. This has also produced a drop in the futures price as December is now under $19. Fears on a weaker domestic and world economies and higher production in Europe have all contributed to the price drop. As far as the weekly updates go we are still hearing good export demand and domestic demand has not dropped off that much either. If you still need to get covered in the first quarter I would look to puts and put spreads. Avoid limiting the upside as we could see an uptick in demand over the holidays and be right back up in the 20+ range.