11/06/2020

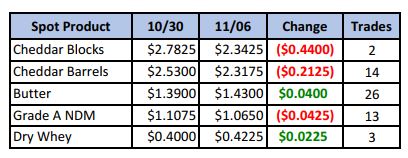

Less than a week after spot barrels hit a new all-time record high, the rug was pulled out and both blocks and barrels took a dive. The block/barrel average went from $2.66 last week, to $2.33 today, and with the more dramatic drop in blocks, caused the block-barrel spread to close to just 2½¢. At the rate it closed, we could very well see barrels premium to blocks by next Friday.

Spot Market Recap

Futures Recap

There was a GDT auction this week. The Dairy Price Index experienced its first decline in 3 events, falling 2%, led by SMP, down 4.4%. Cheddar cheese lost 0.8% to a U.S. equivalent $1.72/lb. U.S. cheese is still the most expensive in the world. Dairy Market News reports milking conditions are good for Australian producers. Adequate moisture is allowing for good hay growth, and prices are cheaper than last year. Exports to Southeast Asian countries beyond China are going well. September milk output in New Zealand increased 1.8% YoY, though there is growing concern over dry conditions and lack of migrant workers.

Heading to the U.S., milk production is generally steady to rising in most regions. Increasing retail sales is limiting manufacturing in the East, but there is still plenty of milk available for processing everywhere else. Spot loads of milk fell to $2-3 under class for the first time in a while. Cream-based holiday items are pulling strong volumes across the country, limiting churning in some instances. Export interest for NDM has been declining recently, putting pressure on prices as dryers remain on busy schedules. About the only thing bullish is the dry whey market, where buyers are scrambling for additional loads in the East, competing with healthy export demand for available supplies. Loads aren’t impossible to find in the Central region, but producers are less willing to sell as cheese plants have been cutting production. Western dry whey supplies are tight, due to steady domestic and export demand, as well as diverting output to higher whey protein concentrates.

USDA released the Dairy Products Report this week. Butter output in September was up 5.4% compared to last year, while Cheddar cheese saw a 7.7% increase. Total cheese output increased 1.1% over the same period. One surprise was dry whey output, which plummeted 17.3% vs. Sept 2019, and down 4.9% from August. This would help explain the current strength in the whey market.

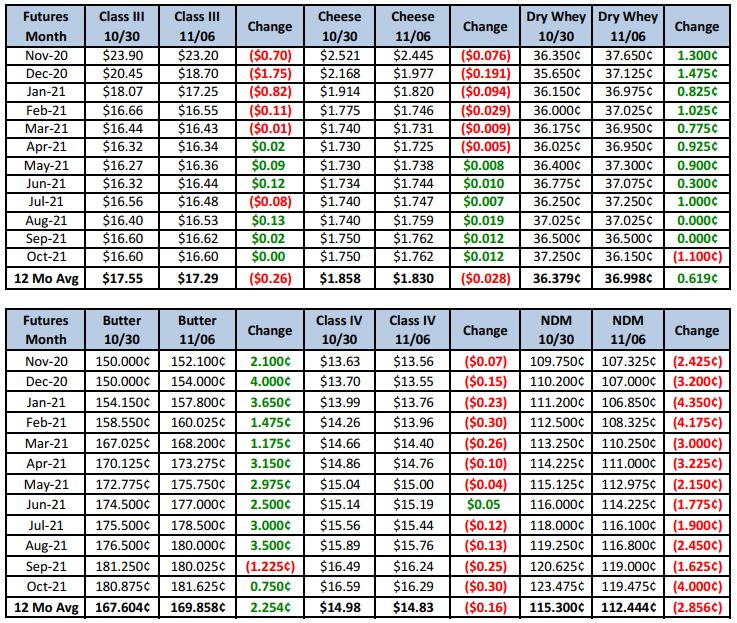

Despite the lack of any major reports, Class III futures saw plenty of volatility. The announcement last Friday’s of a 4th round in the Food Box Program saw limit up moves that day, followed by a strong Sunday evening open, with follow-through buying on Monday. The December contract settled an expanded limit up 83¢ that day. But then the bottom fell out as sellers got extremely aggressive when spot cheese appeared to stall. Tuesday saw red ink across the board with the Dec contract now an expanded limit down 76¢. Wednesday was wilder still as selling was relentless going into the spot market session at 11:00am. The November contract, being in it’s calculation period, was particularly affected, with early spot offers bring it to an intraday low of 21.80, only to see bids for cheese arrive partway through the session and a massive short-covering rally ensue. Over 1,000 Nov contracts traded, with over a $1.00 intraday move from low to high. Spot sessions the rest of the week continued to see barrel bids and a less frequent block bid, but it was enough to cause Nov to settle at $23.90 on Friday, a full $2.10 off it’s low on Wed. Amazing. The Nov contract might not be done. With half its calculation priced in and current spot numbers working out to about $25.35, the gap between Nov futures and spot will continue to close if spot can hold or go higher next week. Hang on.

Aside from the Nov contract though, most Class III contracts saw fairly heavy losses by week’s end. We have to admit we feel somewhat vindicated in our advice to get more milk price coverage in the 2021 contracts. We’re not always right and admit when we’re wrong, but the market is telling us something here. Case in point is today’s settlement, with the Nov contract up 62¢ and Dec up just 7¢. The market is saying this latest government involvement will be short-lived, and when it is, we will have plenty of milk. The herd size and cow numbers are both rising. Unless there is a strong increase in exports, help from mother nature or continued skewing of normal market signals due to government programs, $16 milk may look pretty good in the not too distant future. The Q1 average went from $17.25 last week to $16.98 today. The Jan-Jun average went from $16.92 average last week to $16.68 today. Those were opportunities which we may not see again. Consider whether you should be getting more protection in place for 2021.

Weekly slaughter numbers continue to show a large decline in dairy cow culling. For the week ending 10/24, 58,200 head were removed from the herd, down 6.4% vs. the same period a year ago.