10/16/2020

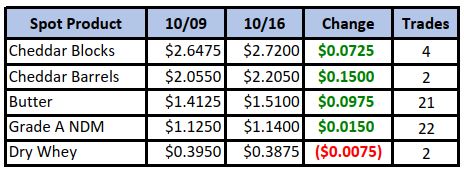

Barrels once again out-gained blocks in this week’s spot market, narrowing the spread to a still wide 51½¢. Considering the higher availability of barrels than blocks, we’re surprised that at $2.20+, those with any inventory are still refusing to sell. Just 2 loads of barrels traded this week, and a nearly-as-small 4 loads of blocks. Spot butter continued to impress with a solid gain on good volume, indicating a longer-term bottom may be in. Buyers are now jumping to get “cheap” inventory for the coming holidays. NDM saw good volume but little price change, while dry whey couldn’t do much of anything on almost no volume.

Spot Market Recap

Futures Recap

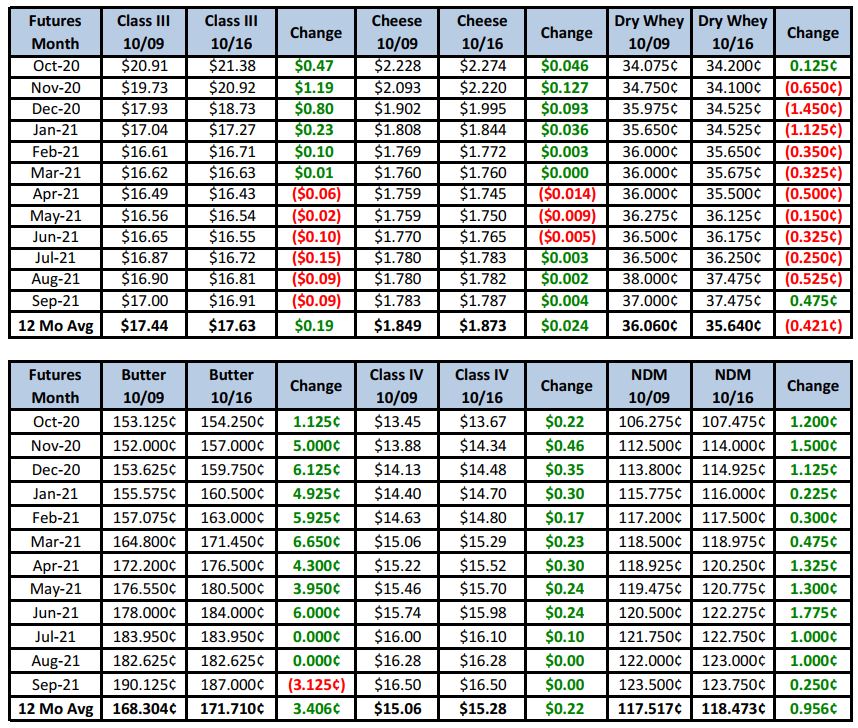

Sometimes you just have to admit you have no clue what’s going on; that pretty much sums up our feelings at the moment. Aside from strong government buying for the current round of the Food Box program, we’re a bit mystified by this week’s gains. Sure, we get it; spot prices currently work out to about $23.40/cwt and we begin the pricing period for the November Class III contract next week. But in order to settle there, we’d need to maintain current spot prices for the next 30 days. At $20.92, the November contract is still pricing in a spot break, but that hasn’t happened yet, and until it does, it will continue to be dragged kicking and screaming higher. We’re equally impressed with the December contract which hit a new life-of-contract high today of $19.00. As hedgers, we’d look long and hard about getting coverage at these prices. With milk output on the uptick now across the country, a large new cheese plant in Michigan coming online by the end of the month and continued government participation questionable after the election, it’s hard to see how these prices will be sustainable (part of the “no clue” feeling we’re having at the moment).

Dairy cow slaughter numbers this week were again significantly lower than year ago levels; just 57,800 dairy cows were removed from the herd, down 9.9% from the 64,200 head a year ago. The milking herd is growing.

Dairy Market News reports cheese is moving well in the East as strong retail sales are powered by consumers cooking and eating at home. However, cheese plants are running full schedules and supplies are beginning to potentially outweigh current needs. In the Midwest, plants are running hard, but bulk buyers are returning to refill pipelines. Even barrel producers report they have limited supplies to offer. But in the West, cheese manufacturers are running at or above designed capacity due to strong demand and plenty of milk. Demand from retail and the government is keeping the fresh block supply tight, though barrels are more available. Likewise, cheese makers do not want extra cheese on hand once government programs expire. There is growing concern that current high prices won’t last.

We couldn’t agree more. In summary, cheese remains tight for now, but once the current round of the Food Box Program is over, rising milk output and extra cheese making capacity will likely cause a significant correction. We would sell Dec above $19.00 all day. The Jan-Jun average picked up a few cents from last week, setting at $16.70. We continue to recommend getting coverage near the $16.90 level, maybe sooner. Q1 settled at $16.89. Consider selling Q1 at a $17.00 average if we get there. Q1 has settled above $17.00 just 3 times in the last 25 years (2008, 2013, 2014). Short of a dramatic improvement in exports or the help of mother nature, we’re quite bearish looking ahead, once the government buying party is over.