10/09/2020

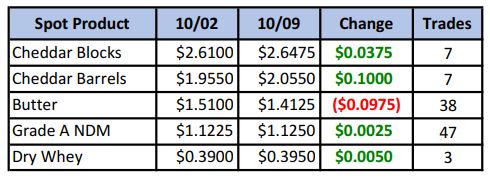

After reaching $1.01¼ on 09/21, the block/barrel spread has been steadily decreasing as barrels have made stronger gains vs. blocks. This held true again as barrels picked up 10¢ vs. blocks gaining just 3¾¢, closing the spread to 59¼¢. With government programs currently favoring barrel cheese, the spread is likely to close further in the coming weeks.

Spot Market Recap

Futures Recap

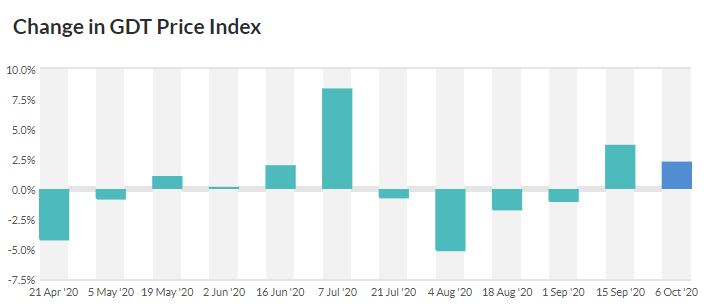

Taking a look at the international picture first, this week’s GDT auction saw the Dairy Price Index increase 2.2% from the previous event. Gains were led by butter milk powder, butter and AMF.

Dairy Market News reports weather in the EU has been favorable for milk production, with increases reported in recent weeks. Concern is growing over the potential global milk supply with increases also expected in the U.S. and Oceania. Cheese manufacturers are running busy schedules, but finding it hard to keep up with current demand. Some delivery times are being delayed. In Oceania, milk output in Australia is projected to be the best in three years, while New Zealand output is off to a strong start. That said, cheese demand has increased with more of the population staying home, causing some supply tightness expected to last through November.

In the U.S., milk supplies have tightened a bit in the Northeast as more milk is heading to schools, while milk is traveling from other parts of the U.S. into the Southeast for Class I needs. Output is steady in the Central region, but demand is increasing as more schools reopen. Cheese makers are getting a bit short on milk, with spot loads now all priced above Class. California output is steady, able to keep most manufacturers near full capacity. Milk is in balance in Arizona, but in New Mexico, demand jumped for Class I, II an III, tightening the supply. There is still plenty of milk available in the Pacific Northwest, but generally is in good balance with processing needs.

Cream is more available now that ice cream season is wrapping up, except in the Central region where supplies have tightened. Manufacturers are reviewing the inventories in light of the year-end holidays. Butter supplies are readily available.

Dry whey prices have edged higher as strong exports to China and other Southeast Asian countries have held inventories in check. Some manufacturers indicate stocks are mostly committed in the near term, giving a bullish tone to the market.

NDM sales have been solid to Mexico, Southeast Asia and domestic markets. This is limiting spot load availability and causing prices to continue to rise. Cheese producers are still active buyers as they look to fortify yields.

Cheese inventory is tightening across the country, even as some customers have stepped back due to current prices. Manufacturers are confident they will return when their supplies get low. Fulfillment of government contracts is also contributing to the shrinking cheese supply. Meanwhile, the milk supply has tightened from a few weeks ago, as schools are pulling more milk away from manufacturing. This is giving a bullish tone to the cheese market..

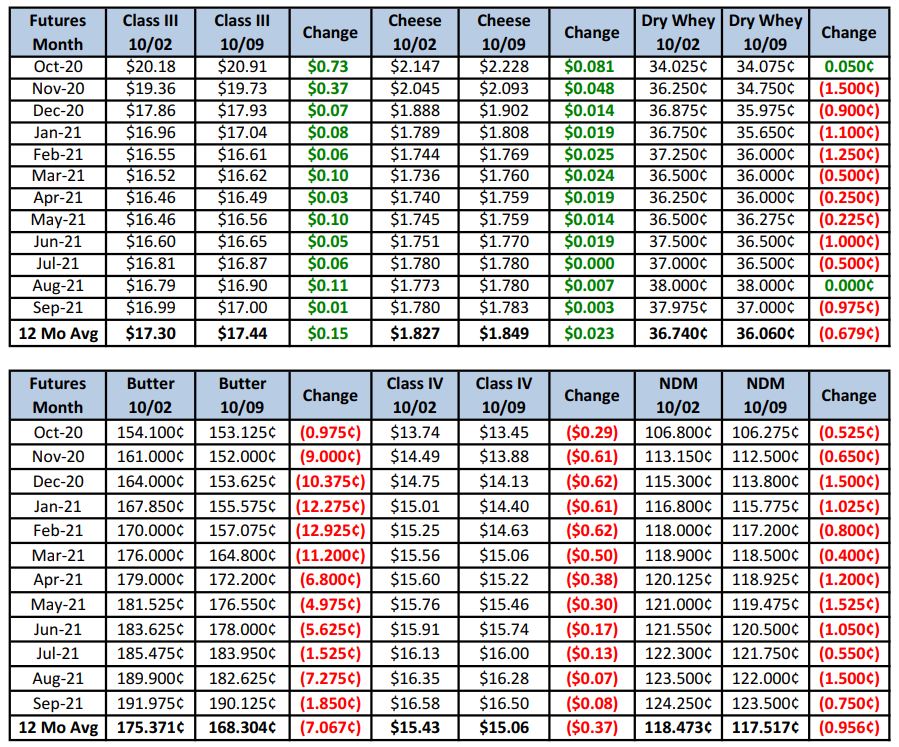

The Dairy Products Report was the only major release this week, and it had little affect on the market. Butter output in August jumped 7.8% compared to a year ago, while cheddar cheese output increased just 0.5%. Total cheese output declined 2.1% vs. Aug 2019.

We still maintain that the market is setting itself up for a major correction, but in the near term, it looks like the path of least resistance may be to the upside in the nearby months. Class III 2021 contracts weren’t all different from last Friday, with most of the gains seen in the Oct/Nov contracts. With the U.S. government still actively seeking cheese, a tightening milk supply in the Midwest and growing tightness in the cheese supply, we’d expect bidders to return during next week’s spot market, seeking physical product. Just seven loads of blocks and barrels exchanged hands this week, so buyers weren’t all that successful. With October finishing up its calculation period next week, all eyes will be on the November contract as it currently is sitting at a significant discount to spot, which calculates out to about $22.40 Class III. Unless buyers suddenly disappear, November Class III will be forced to close that gap.

Hedgers should continue to look for opportunity to get coverage in the first half of 2021, which settled today at a $16.66 average. Consider marketing some of your production if we near the $16.90/avg level.

Have a great weekend!