10/23/2020

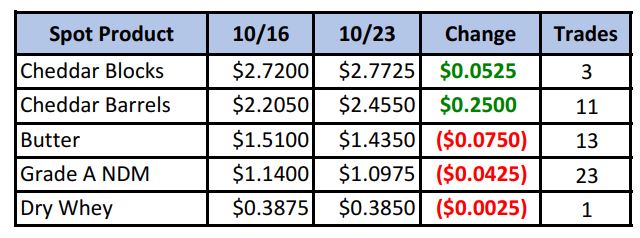

For the third week in a row, barrel prices rose much more than blocks, with the spread now down to 31¾¢, and now we might know why. Fresh blocks remain tight due to current government buying, but barrels have now tightened up a bit, as those plants that could, switched from barrel to block production due to higher returns. In addition, there has been a reluctance to over-produce cheese at these prices, as plants are wary of current prices and don’t want to be stuck with high-priced inventory. While cheese prices made gains this week, spot butter and powder lost ground.

Spot Market Recap

With the big gains in the spot barrel price the past few weeks, the block/barrel average now sits at $2.61/lb. Could it be set to challenge the high set this summer? It sure looks that way.

Futures Recap

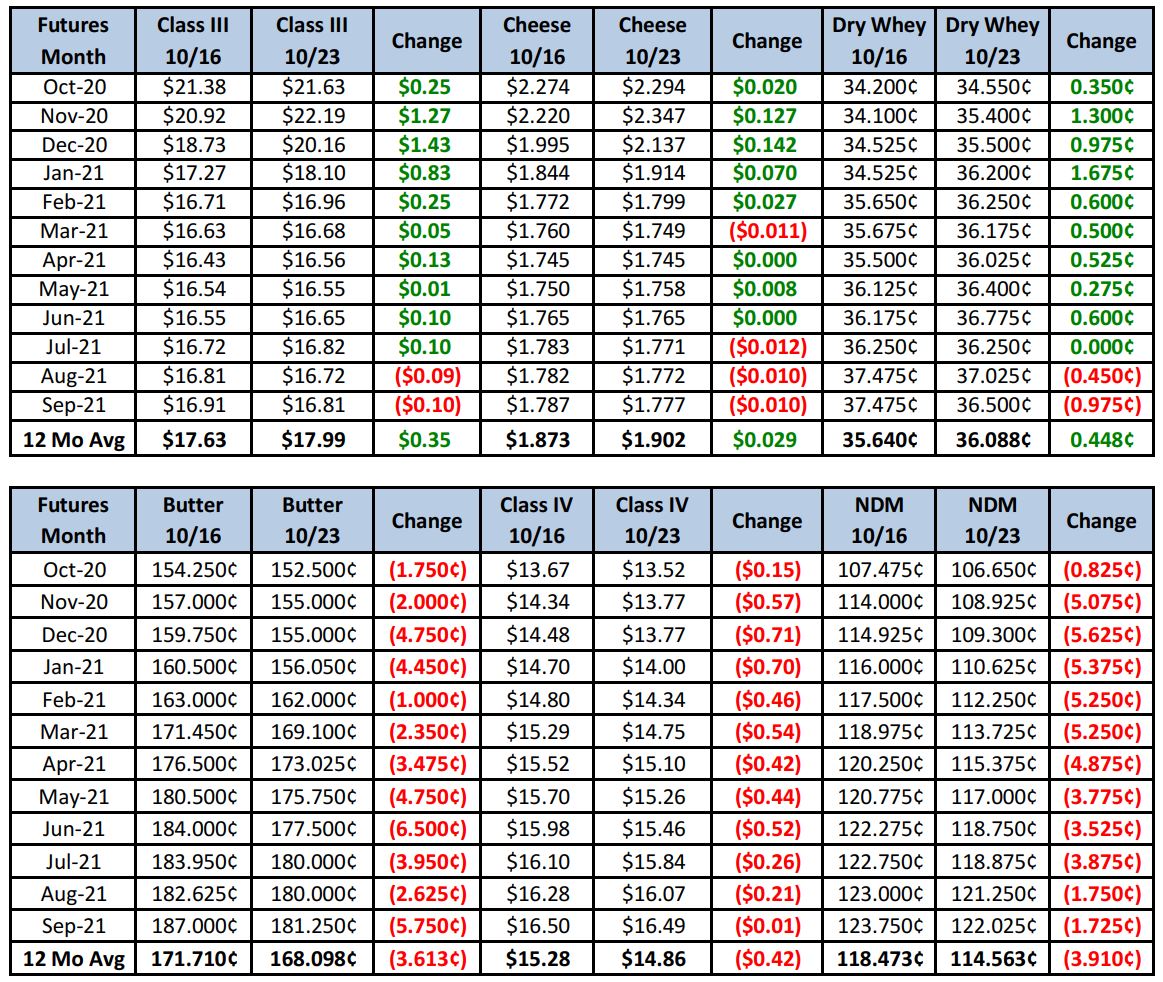

You may recall last week we admitted to being mystified by the market, especially the spectacular gains in the December Class III contract, which continued again this week. Now we know. This afternoon USDA announced a new round 4 of the popular Food Box Program, authorizing $500 million for purchases of products to be delivered Nov 1st through Dec 31st. While the sum isn’t as large as previous rounds, it should go some way to keeping the cheese supply on the tighter side for the next several weeks. Seeing the market rally for a few weeks now though, it does give us pause that this information was “known” prior to general public release. It’s hard to imagine why the market should have been so strong otherwise.

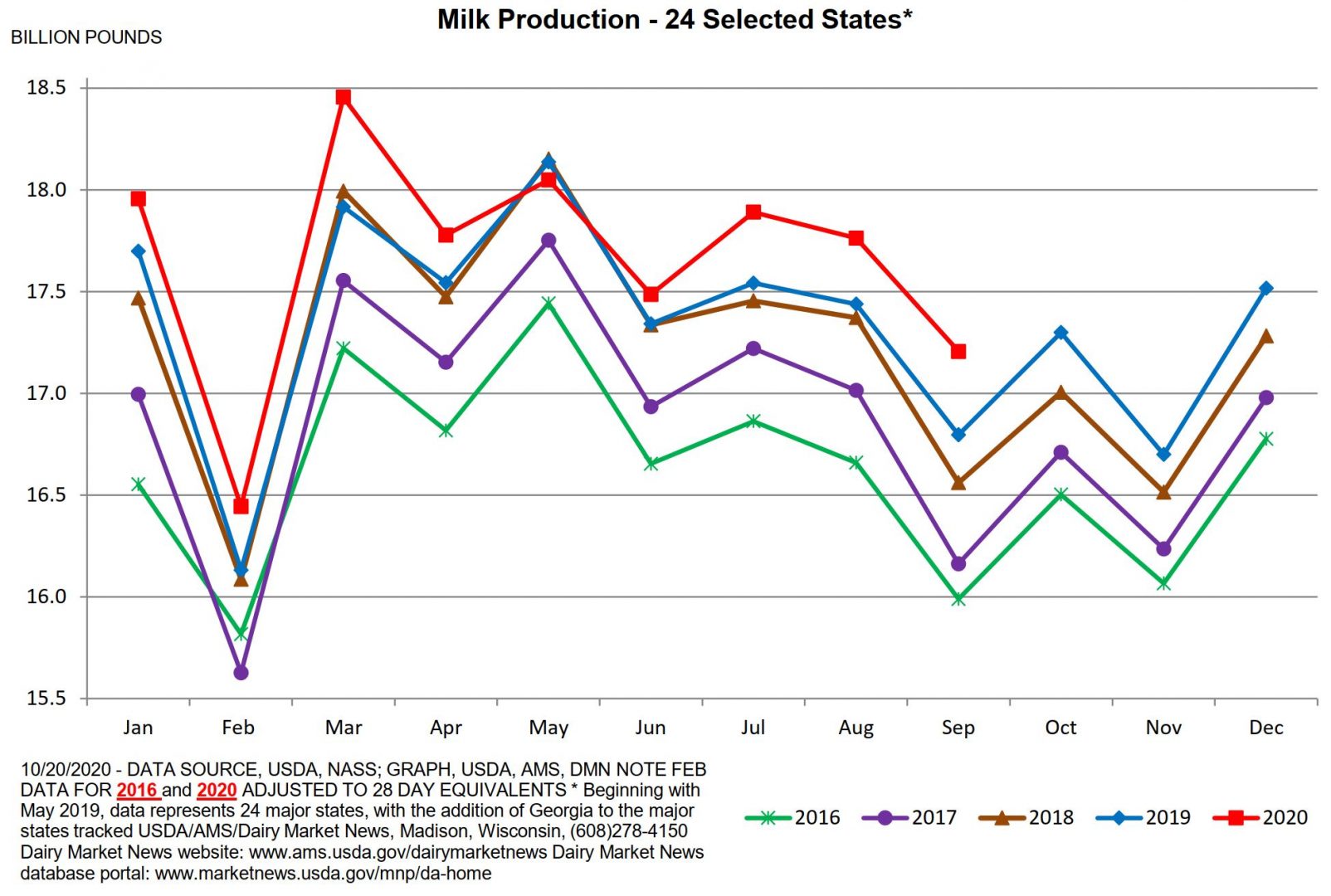

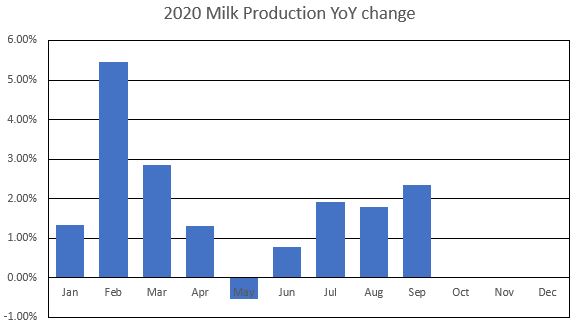

Indeed, Tuesday’s Milk Production Report resulted in a strong sell-off Wednesday as September milk output in the U.S. was up a strong 2.3% compared to a year ago, and cow numbers increased 5,000 head from August (which was revised higher). The 2.3% increase is the largest monthly gain since March.

likely see continued support as it tries to close the gap with spot. Short term, December Class III looks to move higher as well, with government buying now leading into November. Consider hedging Dec in 50-cent increments above today’s settlement.

Have a great weekend!