08/14/2020

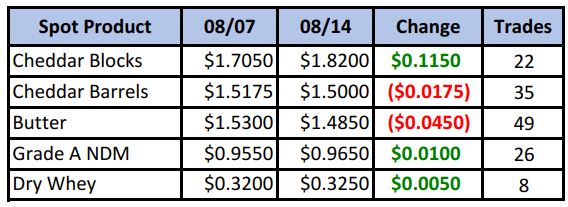

After bottoming out at $1.51 block/barrel average on Tuesday, bottom pickers finally started hitting spot blocks, lifting the average to $1.66 by the end of the week. Most of the work was done with a 12-cent gain for the blocks on Friday, pulling it in to the green. Barrels still felt week but volume picked up to 35 loads. Butter won the volume crown, however, with 49 loads exchanging hands, while NDM and dry whey edged slightly higher.

Spot Market Recap

Futures Recap

There was a lot of relief this week when spot prices finally stopped falling, and some optimism that perhaps a bottom has been put in, at least for the time being. We’re hearing through contacts that early holiday preparations have begun and thus demand for non-cheddar varieties is on the rise. Calls also started coming in block cheese as buyers who had been sitting on the sidelines, started to jump back in.

Dairy Market News reports fluid milk output in the Northeast is picking up a bit, with concerns noted over hybrid school openings and how that will affect the demand picture. Milk is more in balance in the Mid-Atlantic, and somewhat tight in the Southeast. Strong Class I demand is pulling milk in from other regions there. It’s hot in the southern reaches of the Central region. Areas like Texas note poor cow comfort. But in the Midwest, cooler weather is allowing for output to increase a bit, along with components. Heading West, output is in balance with demand in CA, AZ and NM, while plants continue to run full in the Pacific Northwest.

Butter output is active across the country, but ice cream demand is starting to ease as summer winds up. However, butterfat supplies remain tight across much of the country, and retail butter sales continue to be strong.

Cheese contacts in the NE report some foodservice sectors have pulled back on ordering as restaurants are not serving at full capacity. Cheese inventories are growing and starting to outweigh demand. Plenty of milk in the Midwest is cheese plants running hard. Curd orders are strong but barrel demand is stead, resulting in a weaker tone to the markets. Western cheesemakers report export interest has perked up a bit with lower cheese prices, but most domestic buyers remain hesitant with the whip-saw action of the spot market. Plants are pushing extra loads of milk away in order to keep cheese supplies manageable.

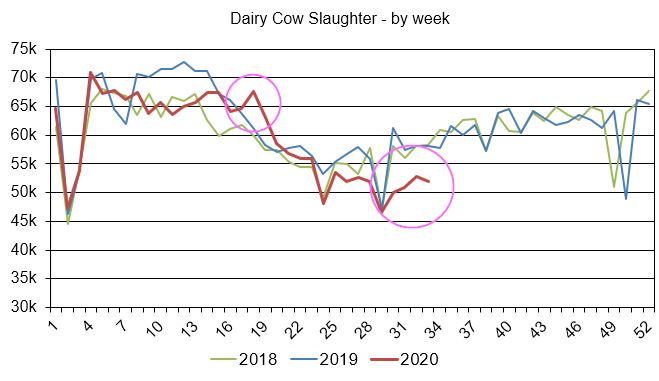

Technically, the strong move on Friday portends further upside next week, but don’t expect another run to $3 cheese. There is plenty of milk around, partly because farmers have really cut down on culling. Week 33 saw 51,900 dairy cows go to slaughter, down 10.8% vs the same week in 2019. It marks the 13th week in a row of lower cull numbers, putting the YTD cull down 81,000 vs. a year ago. What a difference a few months make! As can be seen in the graph below, we began the year with fairly normal numbers, which then spiked higher during May, only to fall dramatically lower the prior years now.

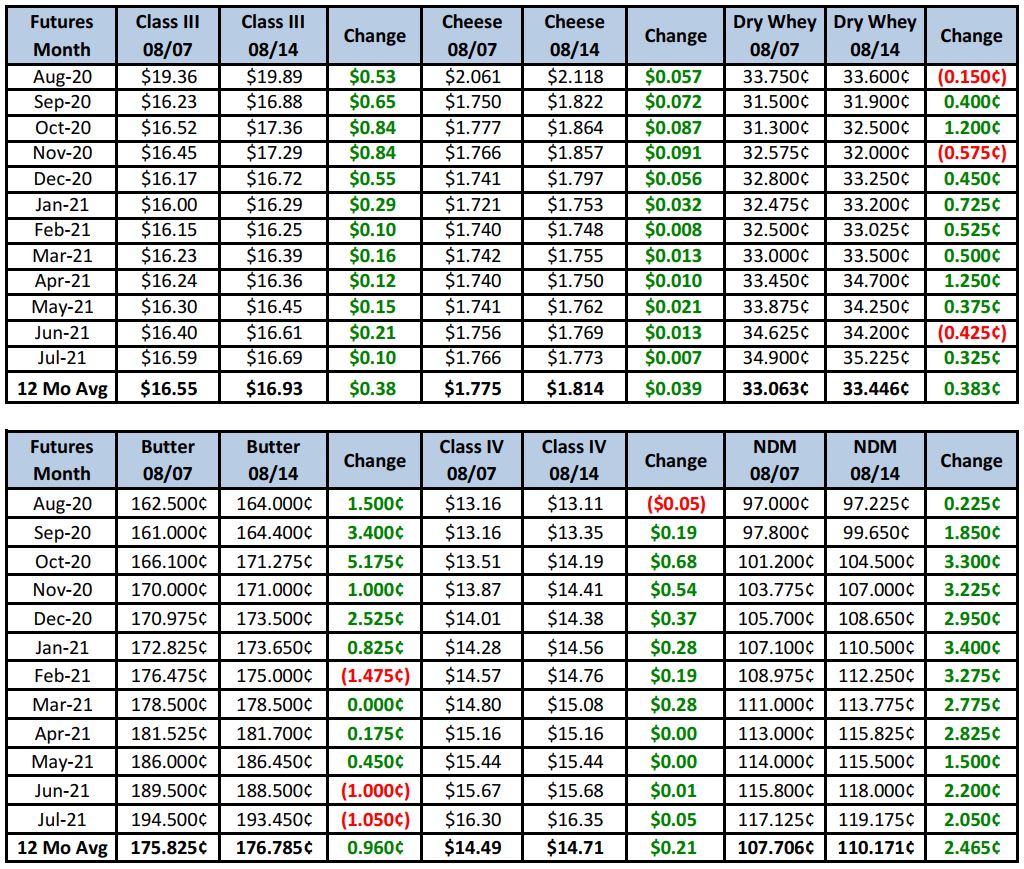

With everyone still waiting on the government for new solicitations, there is a lot of speculation as to what will be the product make up. We already know that less than $500 million will be spent, compared to the previous rounds of $900 million and $1.4 billion. We heard some chatter about it being more Class I focused than Class III. We have no idea, but it makes sense if we have a lot of extra fluid milk available due to much lower demand from schools. We would wait until some of these solicitations come out before making any major hedge decisions. The market is likely to remain volatile and could give you some better hedge opportunities later. Or put in some blue sky target orders Oct-Dec, say $18.40 Oct, $17.85 Nov and $17.40 Dec. 2021 contracts are an interesting case. While the first half has been range-bound since June between the $16.00 to $16.50 area, the July-Dec contracts are quietly and consistently making new life-of-contract highs, settling at an average $16.63 today (see graph below).

Once again it’s hard to say where we go from here, and we don’t think anyone really knows. September Class III begins its calculation period on Monday and is currently trading north of a $1 premium to spot. There is therefore anticipation that spot prices will continue to rise. Indeed, Sep cheese futures settled today at $1.82. It could be an interesting week ahead of us.

Have a great weekend!