08/07/2020

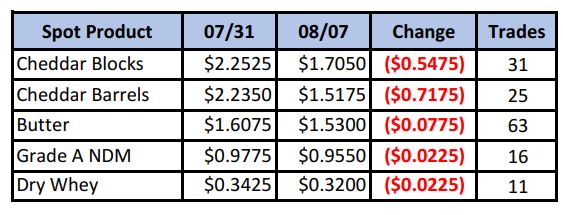

Apparently the spot market does not like roller coaster rides. Having gotten nauseous vaulting from a 17-year low in blocks to a new record high in 45 days, this week it continued to projectile vomit its way back down. Both blocks and barrels suffered horrendous weekly losses, bringing the block/barrel average down to $1.73/lb. Will we now finally find some support in this price range that showed previous consolidation? (see area in yellow box in graph below) We certainly don’t know.

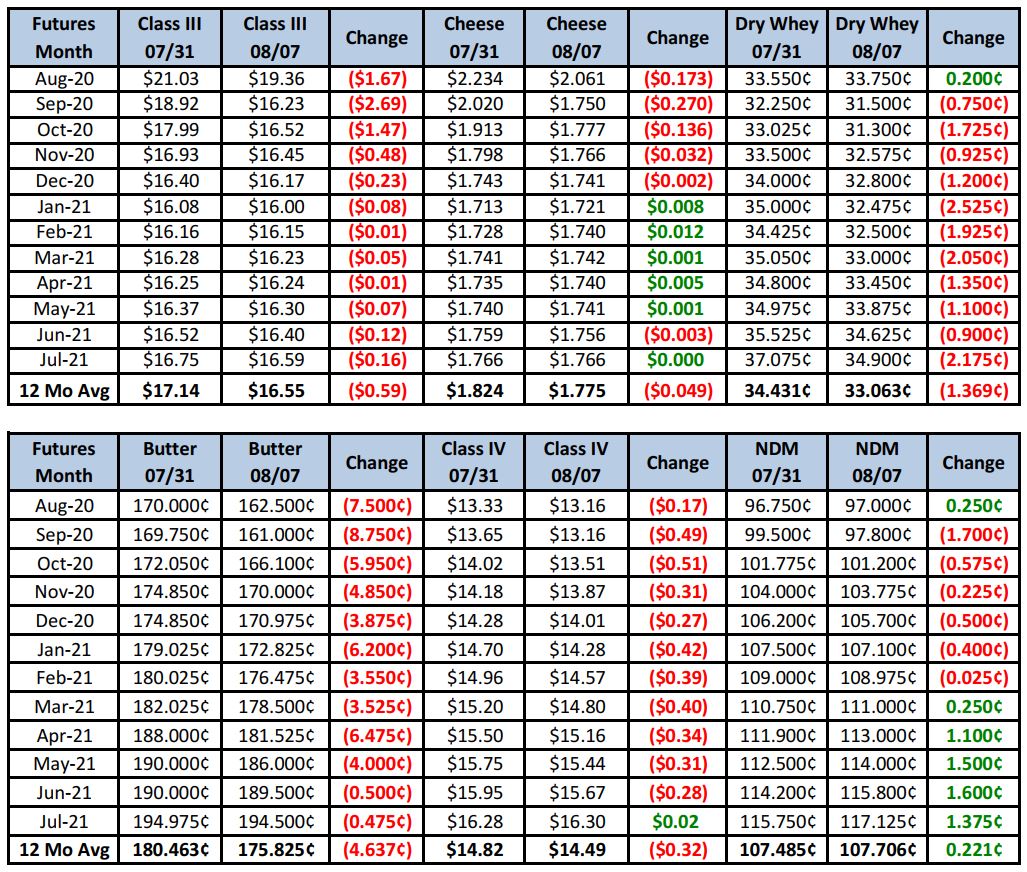

Spot Market Recap

Futures Recap

Last week we asked if the party was over. That now looks rather obvious, although the week didn’t start out that way. After the government announcement on Wednesday of a pre-solicitation for cheese to be delivered Jan-Dec 2021, Q4 Class III futures pushed higher. But as the spot market continued to be crushed, enthusiasm deflated. Actual solicitations won’t come out until September, too late to help the Aug/Sep contracts. And buyers really didn’t have an answer for the continued multiple offerings in each spot session. We ended last week’s comments with, “There is real downside risk Sep on out. Get something done.” Sep Class III futures experienced the worst of the declines, shedding $2.69/cwt from last Friday.

Dairy Market News reports cheese stocks on the coasts are growing, while still mostly committed in the Midwest. But milk is widely available, with balancing plants running full schedules in the Northeast. The uncertainty of school openings appears to be having a negative affect on the market. With COVID-19 concerns still on the forefront of the nation’s collective conscience, more and more schools have announced they will open in either a distance-only or hybrid model, and that means a lot fewer milk cartons will be needed for school lunch programs. Some districts are moving fall sports schedules to spring; that means high school football in May. Such a strange year. The same holds true for colleges and universities. The milk that was destined for fluid consumption will now be channeled into manufacturing.

Meanwhile, dairy operations have continued to hang on to cows. For the week ending 07/25, just 52,800 head were culled, down 9.3% compared to a year ago, By means of lower attrition, the U.S. is quickly rebuilding its herd.

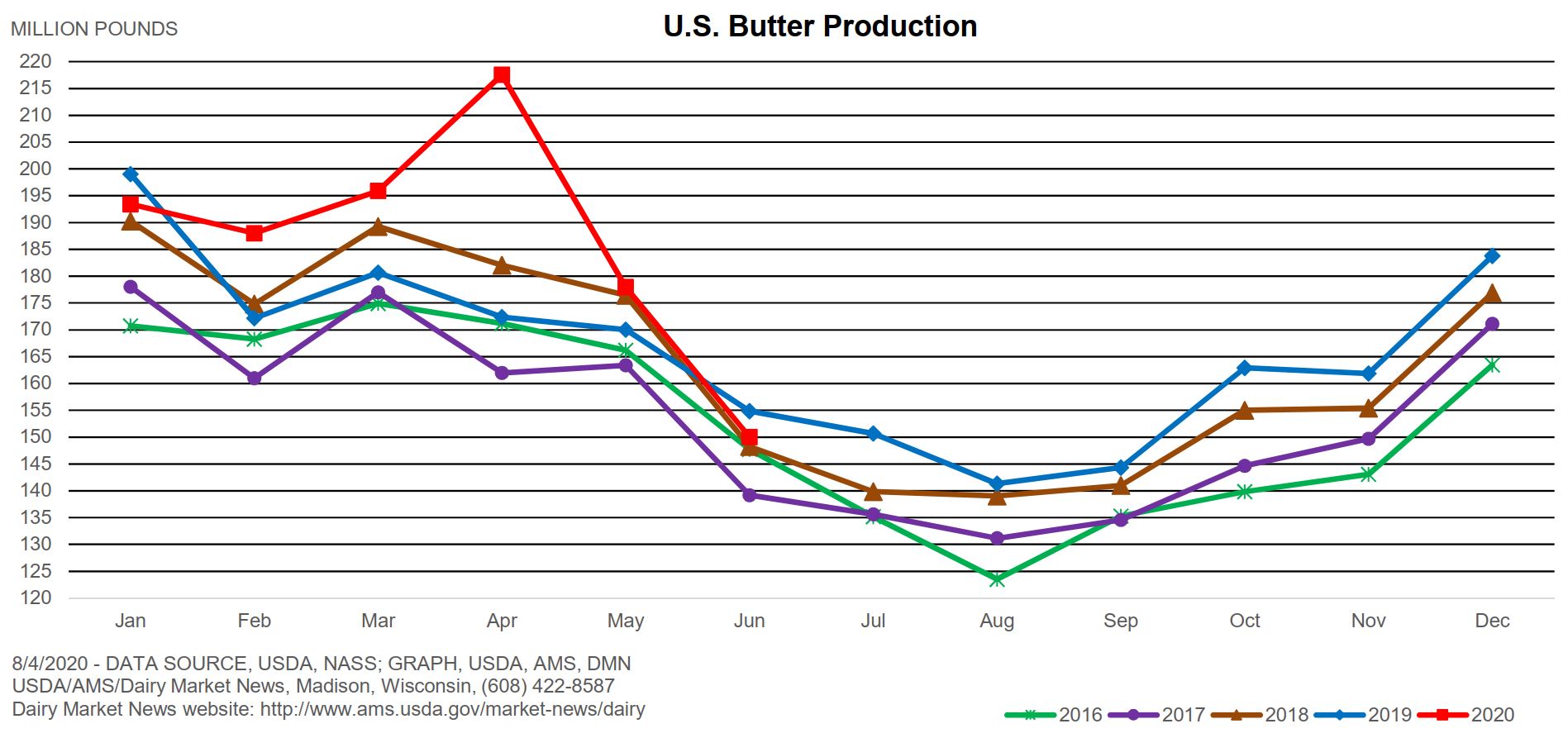

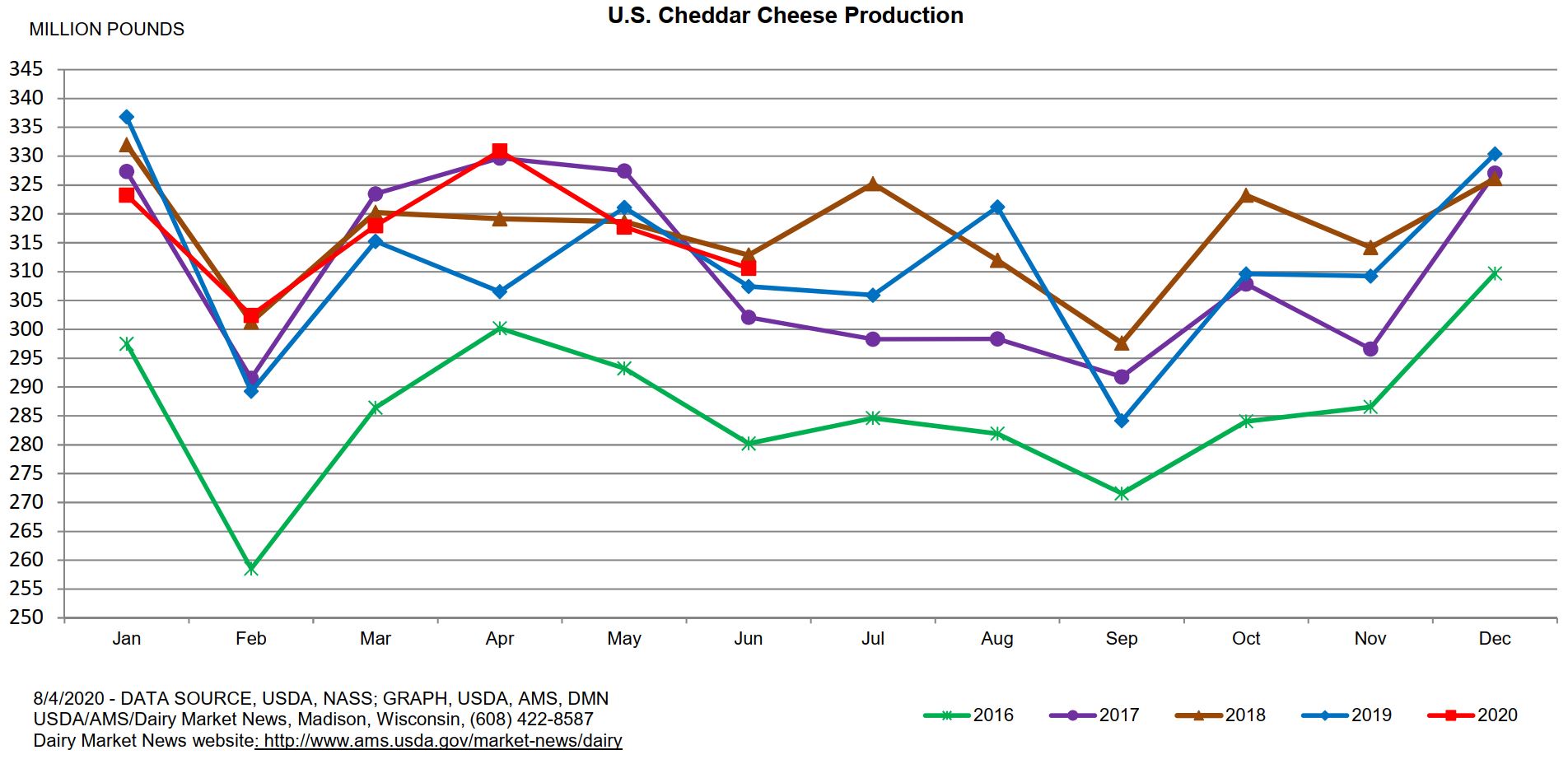

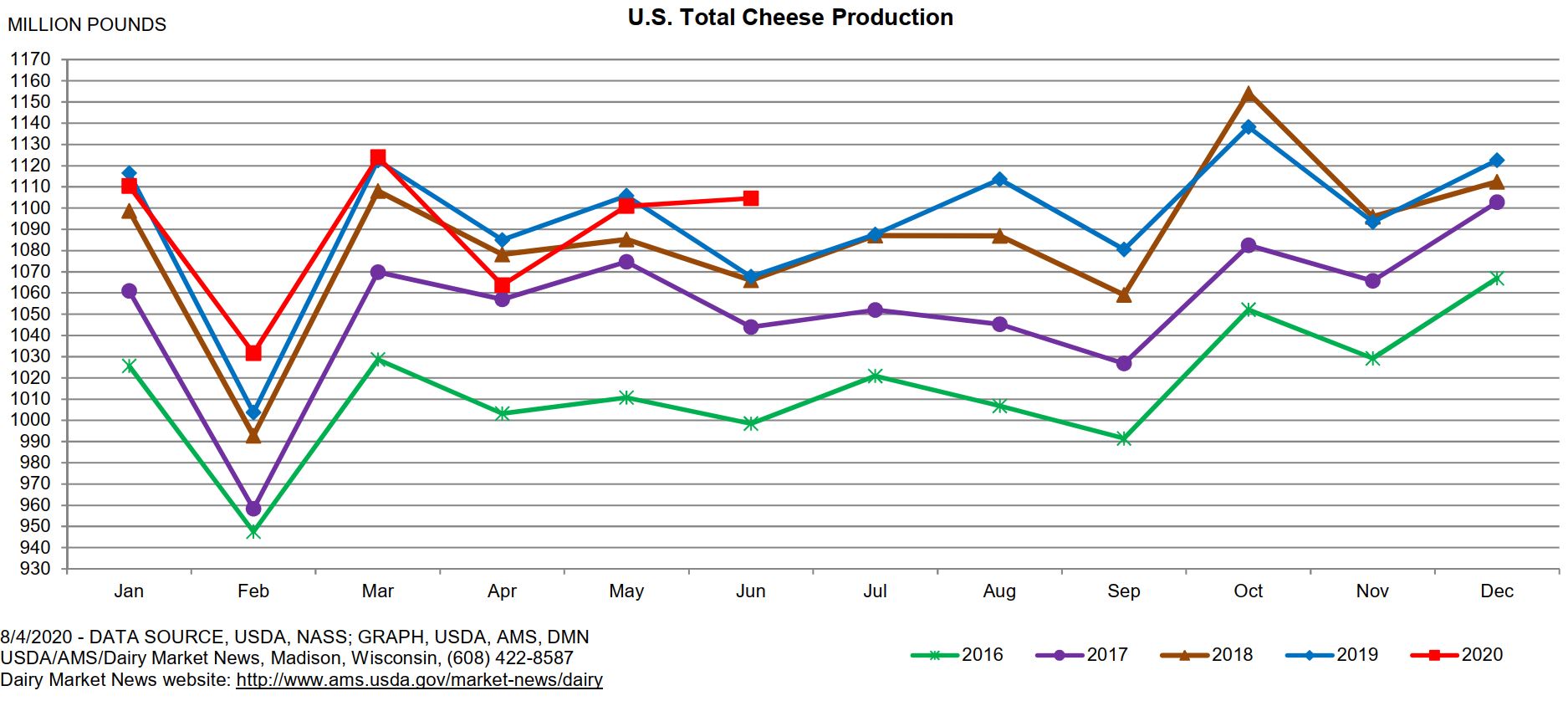

Just one major report came out this week; the Dairy Products Report, which was mainly neutral to the market. Butter output in June was down 3.1% vs. a year ago, but cheddar cheese output increase 1% and total cheese output was 3.5% higher than June 2019.