05/01/2020

Has spot cheese put in a bottom? After being basically flat the past couple weeks, both blocks and barrels finished solidly higher, though volume was quite light. Butter and dry whey managed to pick end the week higher as well, though NDM was not so fortunate, settling below 80¢ for the first time since July 2018.

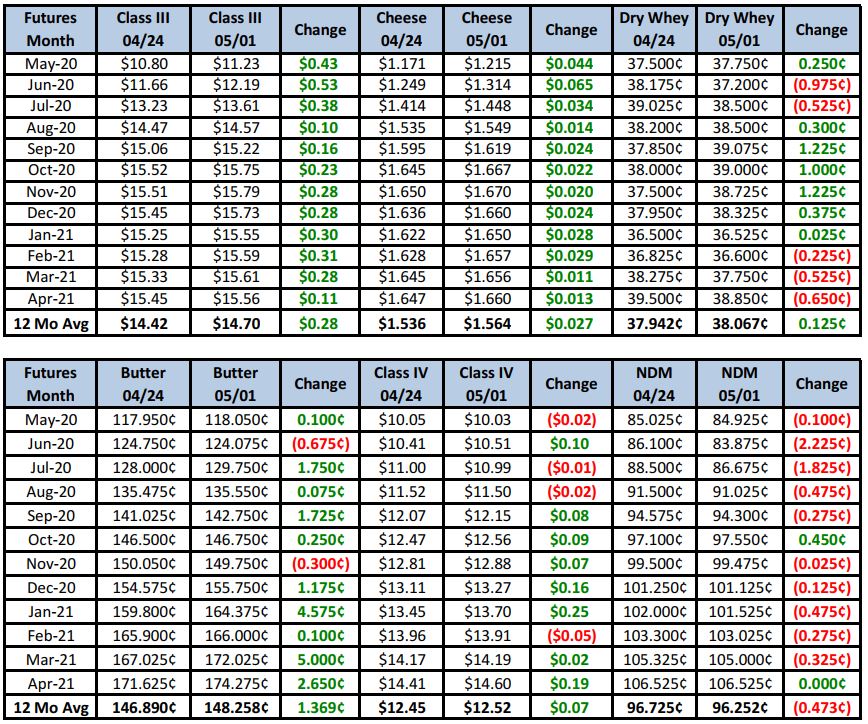

Spot Market Recap

Futures Recap

After a report and data-filled last week, the markets felt fairly calm this week in comparison. Trade volume in the spot market was very subdued, though the decent gain in spot cheese helped propel Class III futures higher. Are the lows in? April Class III was announced at $13.07/cwt, the same as March, and the lowest settlement since May 2016. But current May Class III is nearing the end of its pricing period and will most definitely be lower, with little chance of it reaching even $12.00. That would put it at the lowest settlement price since August 2009. But beyond May, there’s more premium/hope being built into the market, suggesting that will be our low. Is the worst behind us?

Dairy Market News reports this week that, while milk output continues to grow nationally, there are pockets that are now past peak output and even starting to decline. In the Southwest, milk output in AZ and NM is trending lower, while FL is likely past its peak as well. Spot loads of milk can still be found at discounts, but not as steep, with some even trading at Class. The cream market is in better shape as ice cream production is finally getting under way. Lower cheese output is keeping dry whey inventories tight. And the first signs of improved foodservice demand is motivating some cheese plants to increase output. Finally, more cows are going to slaughter. For the week ending 04/18, 67,700 dairy cows were removed from the herd, up a strong 11% vs. the same week last year, and the highest weekly total Feb. Mandates by co-ops and plants to lower milk output is taking root. However, we’re not out of the woods by any stretch. The cumulative weekly cold storage holdings report sheds some light on just how bad the situation is in regards to lost demand. Over the period 04/01 through 04/27, cheese stocks at USDA selected storage centers shot up 19% (14.6 million lbs) while butter stocks jumped 10% (7.8 million lbs).

Everyone understands that the lost demand from foodservice/restaurants is not coming back overnight. It will be very gradual. So it is going to take both an increase in demand from current stagnant levels and a decline in milk output to see any type of price recovery. That’s beginning to happen, but where the guessing comes in is how fast and when. The job of futures is to predict the future and serve as a mechanism for price discovery. Currently, cheese futures are predicting a jump to the low $1.30’s for June, $1.40’s for July, $1.50’s in Aug, and finally $1.60’s/lb Sep on out. Time will tell how accurate that is, but it looks reasonable for now.

Spot prices a week ago had Class III in the sub $10 area, but have since risen and now have us at about $11.20 Class III. Adding basis pushes that to about $11.70. June Class III is pricing in a premium with it set to start its pricing period in a couple weeks. The incremental pickup in demand and decline in cow numbers reported this week could be enough to hold prices there, if not head somewhat higher.

Producers should continue to look at ways to mitigate upside risk on deferred contracts for milk already sold. If nothing else, put in some low-ball offers on call options above the current market. Volatility is one of the pricing factors involved in premium. With the markets settling down some and volatility declining, options premium should begin to decline with it.

Have a great weekend!