05/08/2020

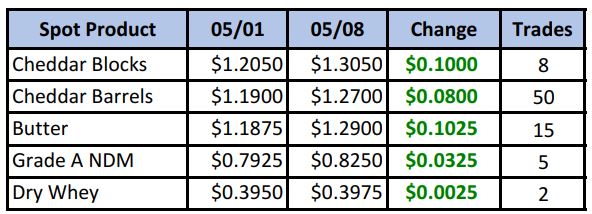

Spot barrel buyers came to play this week, taking on 50 loads and moving prices up 8¢. Block and butter bidders weren’t able to secure as much product, but pushed prices up a dime. What’s going on? A growing consensus that the U.S. literally cannot afford to remain economically closed much longer, combined with warmer weather and a population that wants to get out after weeks of “safer at home” is motivating even reluctant state governments to begin the reopening process.

Spot Market Recap

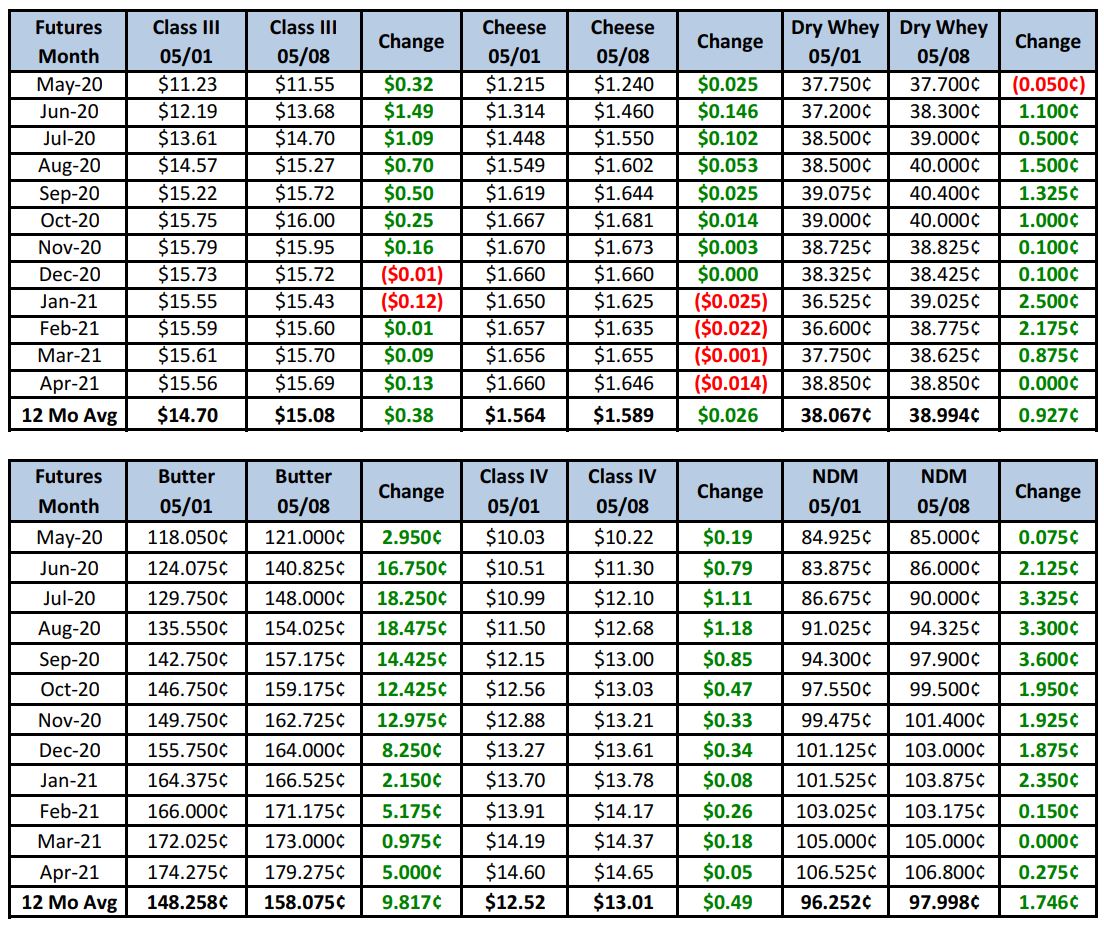

Futures Recap

People we talked to this week pointed out a jump in food service demand as restaurants prepare to refill coolers. At the same time, ice cream production has started in earnest and is helping to mop up surplus cream. Dairy Market News (DMN) reports that as recently as last week, processors were eager to sell cream at discounts, but are now holding on to the cream to meet new butter demand from restaurants. And butter demand at the retail level has stayed stronger than expected. Some butter plants have not yet started building fall inventory.

Fluid milk output across most of the U.S. is declining from peak levels. Stronger culling and output reduction incentives are having the desired affect. Dairy Market News reports milk in the East is tightening up, while Class I needs are increasing. This is pulling milk out of manufacturing in some areas. Output and components are lower in the Central region as well, with the result being the dumping of milk has essentially stopped. Milk production is still strong in the West, but spot loads are not as available. Output in AZ and NM is dropping, but increasing in the Pacific Northwest.

Cheese orders are picking up in the Northeast, according to DMN; everything from restaurants to specialty retail stores to pizzerias. In addition, milk loads are not as burdensome at cheese plants, In the Midwest, purchasers for food service are assuming a bottom is in and are now actively refilling pipelines, even if they are to lower than pre-virus levels. All cheese types are seeing a resurgence in demand, which is giving the market a bullish stance in the near term. Western buyers have been taking on cheese, which even at current prices, is seen as an opportunity to take on a physical hedge.

NDM is not in such a great situation. A weak Peso relative to the USD is hurting NDM exports to Mexico, which is leading to higher inventories.

On to the data:

63,000 dairy cows were slaughtered during the week ending 04/25, up 8.1% vs. the same week a year ago, and the highest total for this week going back at least as far as 2007.

The Dairy Products Report was released this week, but was mostly neutral to the market. Butter output in March increased 7.5% compared to a year ago, lending evidence to recent weakness in prices. Cheddar cheese output increased 1.1% YoY, while Total Cheese output was up just 0.2% vs. March ’19.

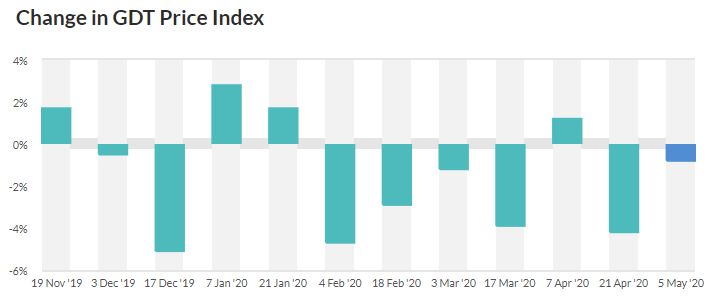

We had a GDT auction Tuesday. The Dairy Price Index declined a modest 0.8%. Butter milk powder was the main culprit, falling 10.3%. Cheddar cheese was down 6.8% to a U.S. equivalent $1.87/lb.

There was some good news on the international front though. While this data mostly pre-dates the COVID-19 demand crash, USDEC reported that dairy exports in March increased for the seventh straight month, and the highest volume since May 2018. Gains were led by a 164% increase in WMP exports. Total dairy products exported accounted for 15.1% of total U.S. milk production in March.

While there will likely be bumps along the way, we’re hopeful that the worst is behind us. The sense of optimism is growing. Even the stock market shrugged off an unemployment rate of 14.7% to rally strong on Friday. Will we see a “V” shaped recovery (quick) or more of a “check-mark” recovery (gradual) or neither? The debate is still out there, and the economic price the country has paid may still reveal itself. But for now, the market believes a quick recovery is under way. The decent dairy export numbers in March could mean after a poor April, export demand may bounce back quickly in May/June. And if more people begin to get back to work and frequent food service establishments, dairy prices could be in for quite a rally after seeing many farms reduce their herds to fit within lower production guidelines.

Dairy operations with upside price risk should get more aggressive in covering that risk using call option spreads or other options strategies. Call us if you would like help protecting what you’ve already protected!

Have a great weekend!