04/24/2020

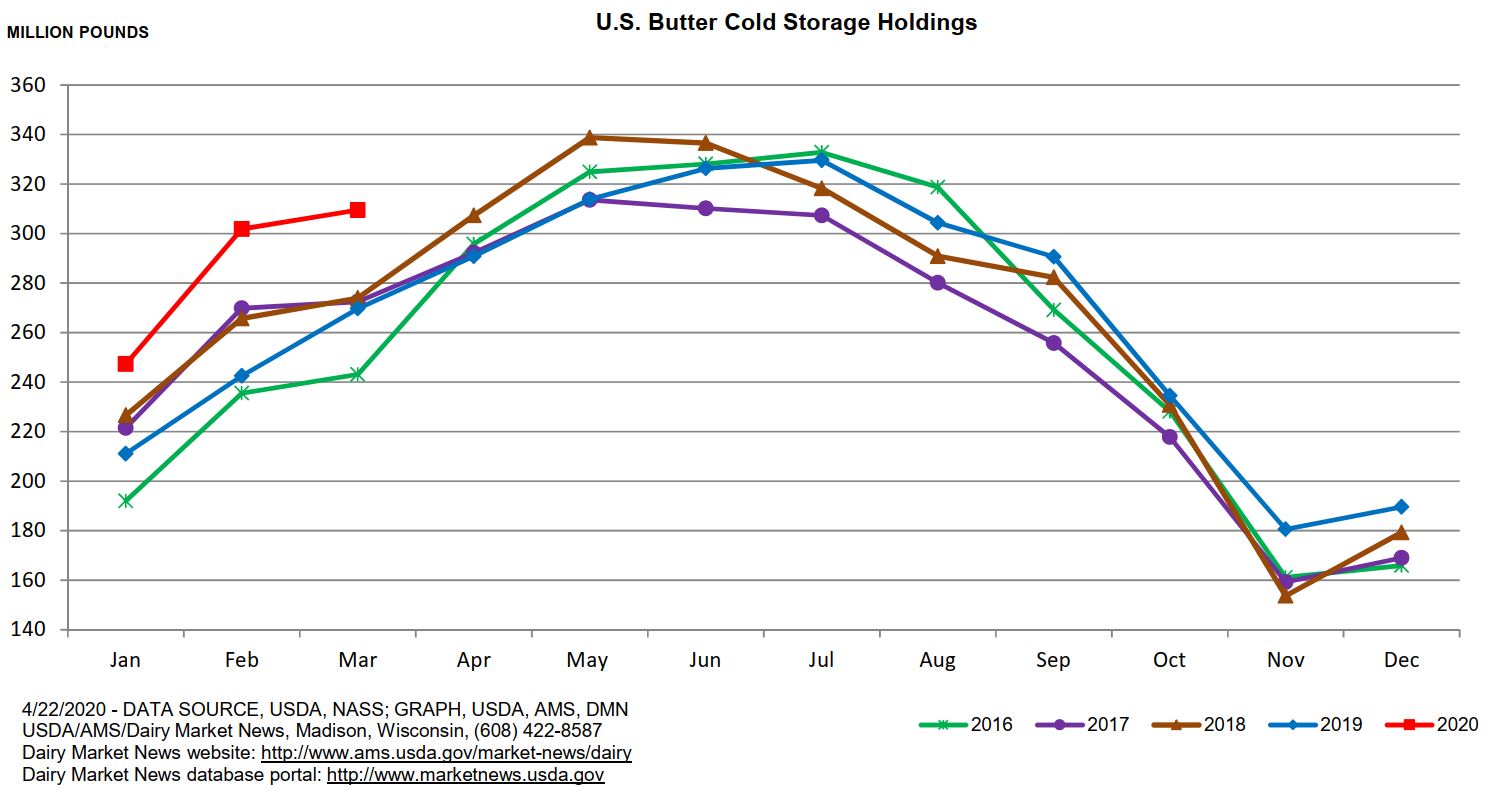

While still historically low, spot cheese prices managed to turn the rudder and finish the week with a small gain on very light volume. However, all other spot components gave up ground, with butter putting in fresh lows not seen since Feb 2009 (see graph below).

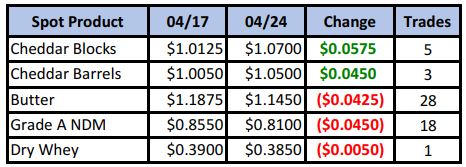

Spot Market Recap

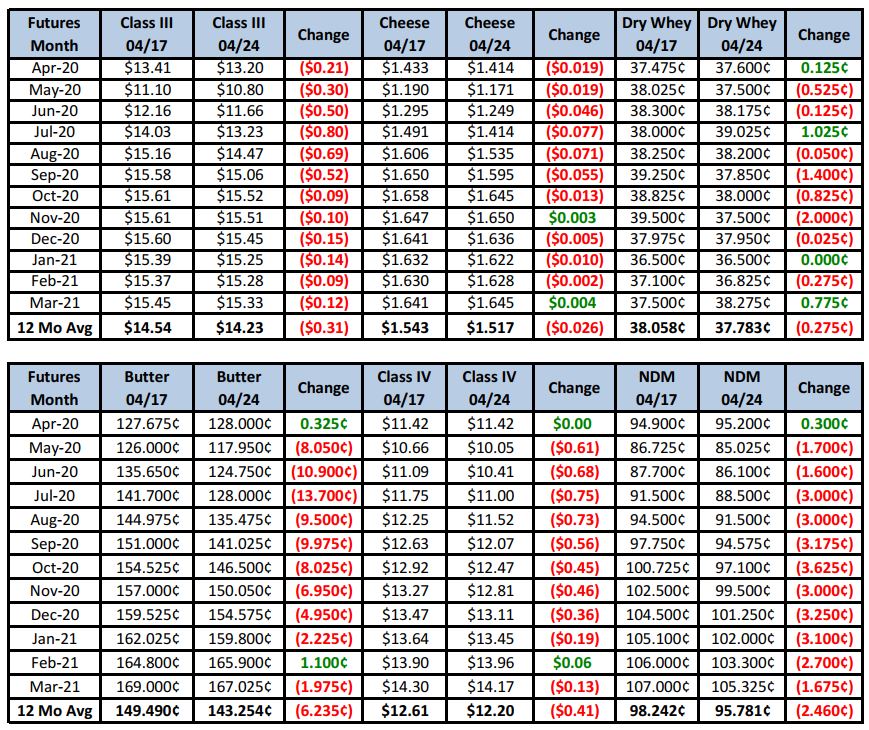

Futures Recap

Just about every futures contract finished the week in the red as demand destruction continues to weigh on the markets. There was some hope very early on as a USDA press conference with Sonny Perdue last Friday evening promised $100 billion in monthly dairy purchases to be distributed by non-profits for needy families. However, early government tenders for bids seem to indicate the earliest deliveries requested are for mid-June, by which time both May and June futures contracts will be priced in. That said, bids were definitely stacked up for both blocks and barrels during most spot sessions, but seemed content to hang below the market and not aggressively bid.

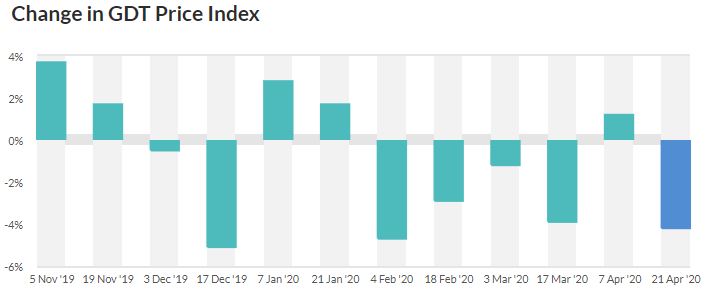

Much data was released this week, so let’s get to it. On Tuesday we had a GDT auction, with the Dairy Price Index falling back in to negative territory at -4.2%.

AMF led the way lower with a decline of 7%, while SMP was down 4.9% and butter down 3.6%. Cheddar cheese in Oceania continued to see a bid, increasing 1.9% to a U.S. equivalent $2.03/lb. With the milking season winding down in Australia and New Zealand, cheese has become laughably tighter in that part of the world. Perhaps it will stimulate some export business from the U.S. at nearly double the price. We’ll see.

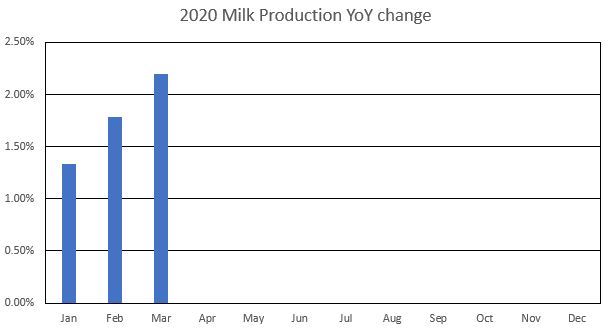

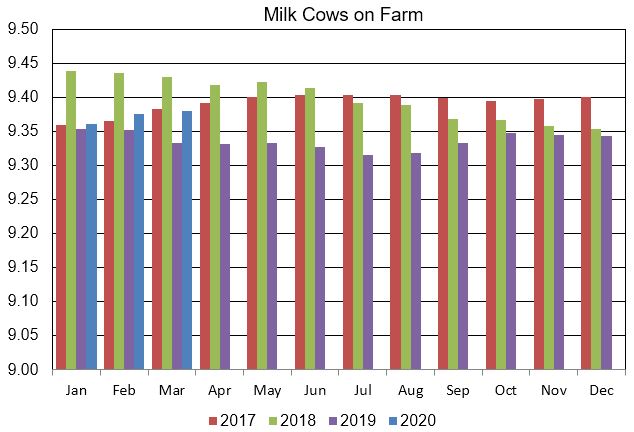

On Tuesday afternoon the Milk Production Report was released. U.S. output in March was up 2.2% vs. a year ago, while the number of milk cows was 47,000 head higher. In addition. USDA revised Feb cow numbers up 5,000 head, yet March cow numbers showed another 5,000 head monthly gain, for a 10,000 head increase to the milking herd since Jan.

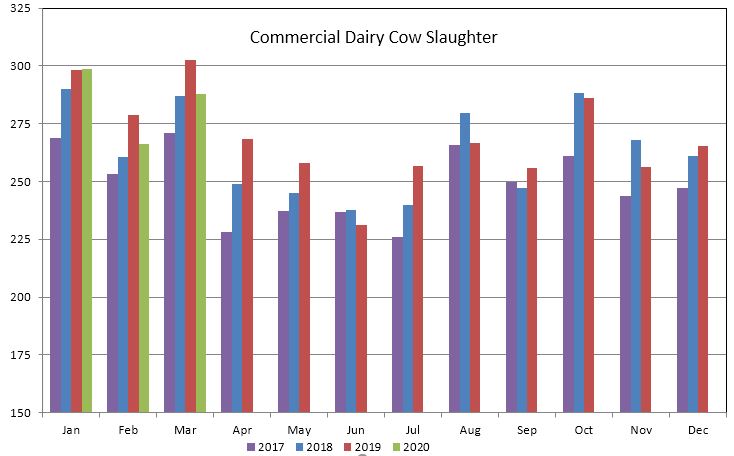

Gains were led by TX – up 8.6%, CO – up 7.5%, SD – up 6.8% and ID – up 5.2%. CA was up 1.3% while WI was down 0.1%. We expect declines to be arriving soon as private plants and co-ops begin to implement reduction incentives introduced this month. Prior to the devastating effect on demand COVID-19 has had, data into March shows growth in both milk production and the size of the herd. On Wednesday USDA released the Livestock Slaughter Report. 288,000 dairy cows were removed from the milking herd in March, but that was down 4.8% (14,400 head) vs. last March.

Weekly numbers are finally starting to show an uptick in the slaughter rate, however. For the week ending 04/01, 64,600 dairy cows were culled, up 1.4% vs. the same period a year ago.

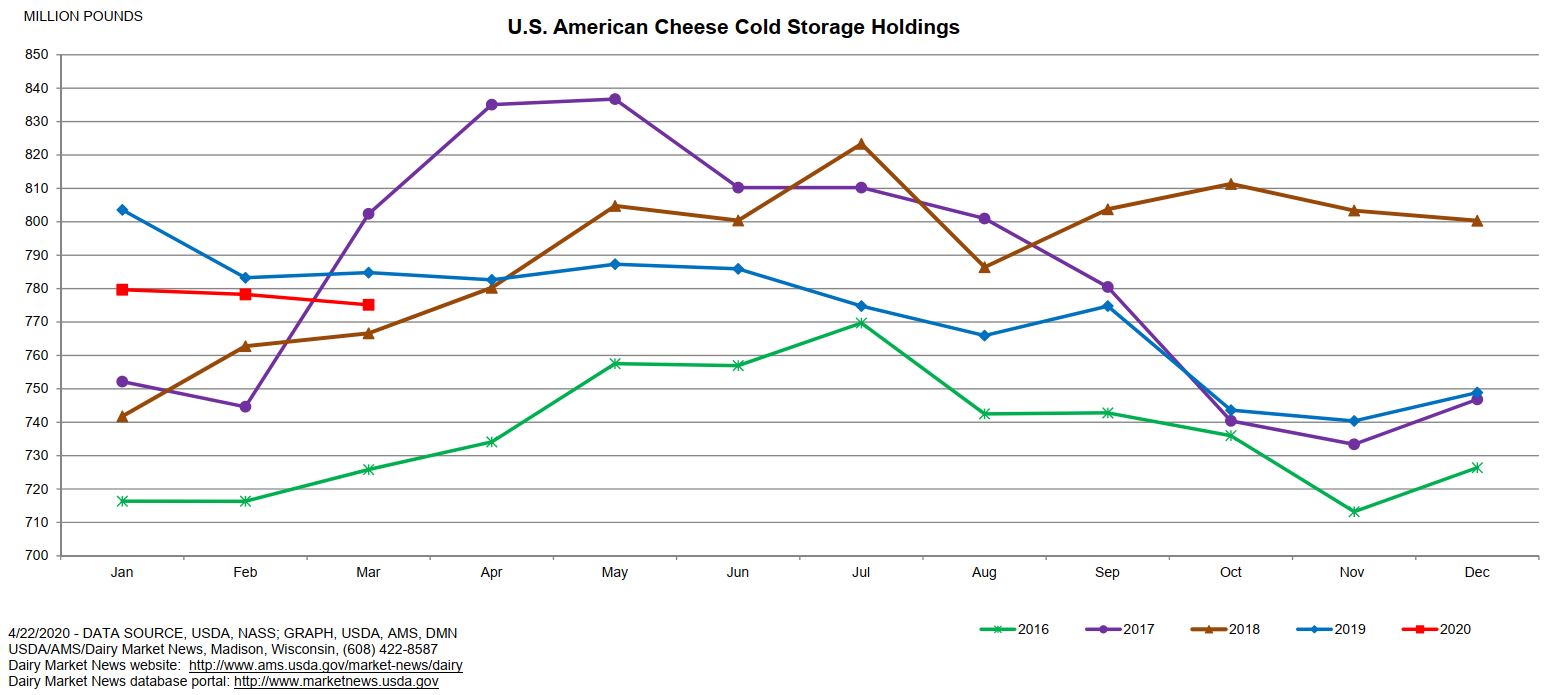

Finally, the Cold Storage Report also came out on Wednesday, with a bit of a surprise. While there was a 15% YoY increase in butter stocks at the end of March, American cheese stocks actually fell 1%, along with total cheese stocks. The jump in the butter supply was expected, but the small decline in cheese stocks was not. However, we still need to remember that demand in March was still largely unaffected domestically.

Trying to guess the price direction in the short term is pretty much impossible. Technically, spot cheese looks like it’s trying to carve out a bottom. But realistically, how much can it recover? Over production penalties and increased culling are going to help, but it will take time. Meanwhile, milk output across the country continues to increase towards the peak unabated. Plants are full in most parts of the nation. Cream continues to slosh around without any meaningful demand from ice cream producers. Butter is being packed away in storage, but warehouses are getting very full. More states appear to be planning a gradual reopening, but others are extending “safer at home” timelines. Current spot prices work out to just about $9.95/cwt; with basis call it $10.50/cwt. With June Class III settling at $11.66 today, it’s factoring in a decent increase before it starts its pricing period in a few short weeks. Are the lows behind us? We don’t know. Longer term, herd reduction and a gradual resumption of normal activities has us somewhat more optimistic, but that too is already reflected in 2nd half Class III’s, which are mostly over $15/cwt. We would continue to focus on getting upside protection in place Aug-Dec for sales already made at higher prices. Call us to discuss possible strategies.

Have a great weekend!