04/17/2020

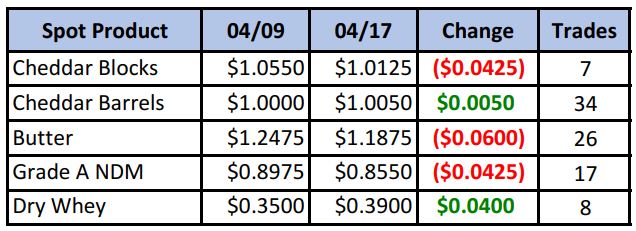

Spot cheese prices were held firmly in check near the $1 level this week, and both butter and NDM gave up further ground. However, spot dry whey has been making a steady climb as of late and is now right up against long-term resistance near the 40-cent level (see graph below).

Spot Market Recap

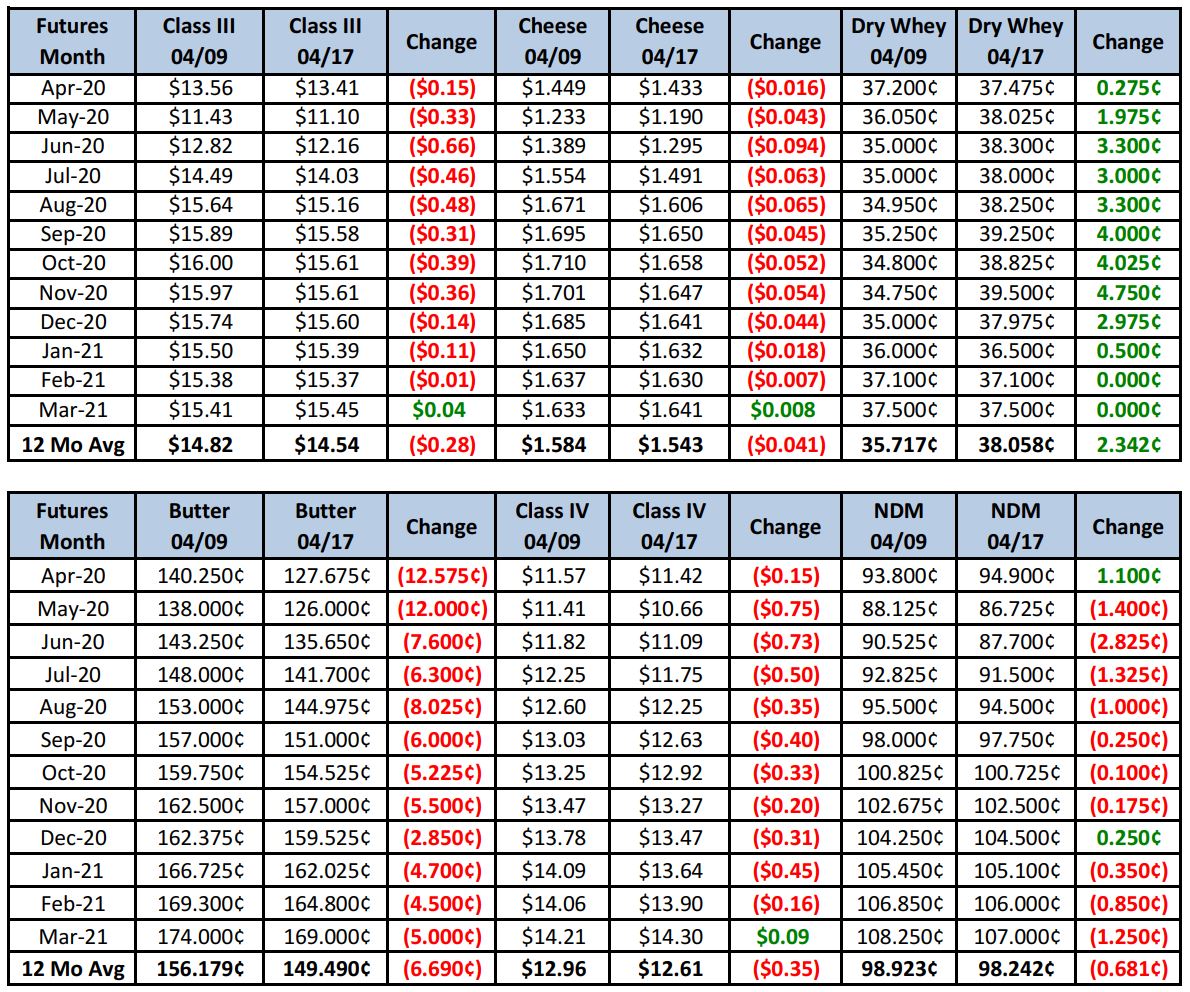

Futures Recap

Producers may want to consider upside risk insurance for these months on milk they have already sold. The current efforts to reduce the herd/milk output could result in a sudden shortage should demand see even a reasonable recovery from current levels. A multi-dollar move higher is a possibility. Selling out of the money put options and using the premium collected to buy call options would be one way to accomplish this.

On the feed side, grain markets have continued to move lower but at a slower rate. It may be wise for those producers who buy feed inputs to get some coverage. Lower ethanol production has taken a toll on corn demand, but also resulted in less DDG output, and inventories are shrinking. This is bolstering soybean meal prices.

Corn: Consider buying $3 Sep corn put options at 7¢ (contract size is 5,000 bushels, or 135 tons). Initially this will protect the value of your grain and silage corn you will be growing, but can also be used to cover downside risk if you decide to lock in with a physical purchase from your supplier.

Soybean meal: Use a similar strategy, buying your physical needs, then protecting against lower prices with an August meal put option. For example, you could place a buy order with your supplier at $275-280/ton, then buy the $280 put for $5/ton premium (100 tons per contract).

Call us if you need help offsetting some risk in either dairy or grains, or both!

Have a great weekend!