02/14/2020

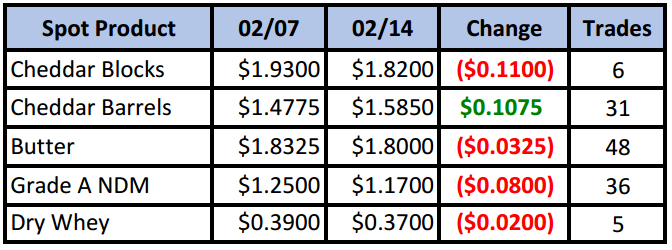

After peaking at an all-time record wide block/barrel spread of 46¢ last week, the market seemed determined to narrow it to a more reasonable number. And narrow it did, by nearly half, with the spread settling at 23½¢ on Friday. A combination of a decline in the block price to a new 2020 low and a jump in the barrel price on heavy volume accounted for the move. Aside from barrels, all other spot markets finished the week in the red, despite decent volume in both butter and NDM.

Spot Market Recap

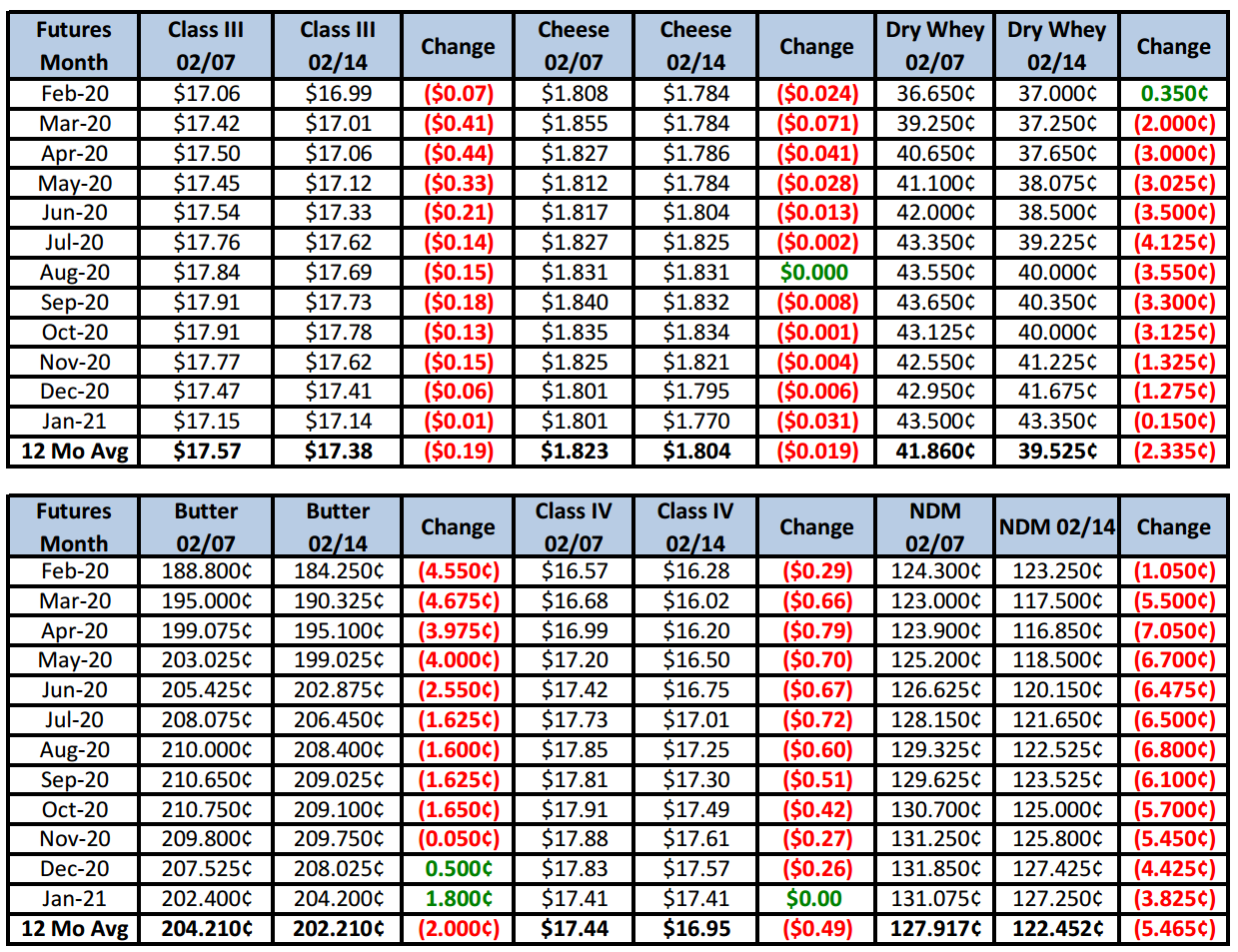

Futures Recap

With declines in the spot market leading the way, most dairy futures finished the week in the red. Mar-Jun Class III futures were hit pretty hard, as well as butter and NDM. The spot block/barrel average settled at $1.70, an area that has previously served as solid support (see graph below). With the current downward momentum in the markets, will it hold? Time will tell.

Dairy Market News reports fluid milk output in the NE has seen a slight uptick, with more milk heading to balacing plants. Mid-Atlantic milk output is flat, but processors are close to capacity. In the SE, milk production is mixed, though output in Florida is climbing. Cream is abundant across the region. The Central region is seeing an earlier than usual start to spring flush. Spot loads of milk are discounted as low as $5 below class. Bottlers are busy but cheesemakers are not looking for extra milk. In the West, CA output is increasing seasonally. AZ has plenty of milk for anyone who wants it, while NM output has jumped to levels higher than typical for this time of year. Output in the Pacific NW remains heavy, keeping plants filled to max capacity. Excess milk is moving out of the region at discounts up to $6 under Class IV.

With an abundant cream supply across the entire country, butter production continues apace with much output headed in to cold storage. Demand is fair to good.

The coronavirus has both the NDM and dry whey markets on edge. Production is ongoing and domestic demand is good, but fears of a demand slowdown from China have buyers hesitating, despite supplies being tight in some areas.

Cheese demand in the NE is good, with increased sales to restaurants. Cheese plants are receiving more milk, but inventories are not burdensome. In the Midwest, cheese sales are meeting expectations so far in 2020. Inventories are available but being held in check. Western cheese is readily available, with cheap cheese being made with heavily discounted milk. Excess barrel offers are common, but retail demand for blocks has been solid, with some block stocks highly committed for the next few months. Positive demand is reflected in this week’s cold storage holding, with USDA reporting cheese stocks at selected storage centers down 3% (2 million lbs) over the first 10 days of February.

Moving to the international side of things, a mild winter is helping EU milk production increase seasonally. Despite the increase in milk supply, cheese output is straining to keep up with very firm demand. Cheese is moving well within the EU as well as through export channels, to the point that most production is committed. Industry contacts expect prices to remain firm and then increase heading in to March.

Milk output in Australia is moving towards the season low. Feed remains tight, with the long–term effects of the wildfires yet unknown. Most of New Zealand is very dry. Dairy officials expect output to be negatively impacted. Oceania cheddar supplies are tight, with buyers looking for whatever they can get their hands on for the coming months. Cheddar cheese averaged a U.S. equivalent $1.96/lb this week.

With Oceania cheese going for nearly $2/lb, a scarcity of cheese in the EU, and cheese demand robust globally, we wonder just how long U.S. prices will continue to see pressure. Certainly a flood of milk during the flush will result in increased cheese output, but at some point it would seem our product is the global value leader. Much of the weakness in butter/powder appears to be uncertainty over the coronavirus and what impact it will have not only on dairy demand, but on the global economy. No one really knows at this point, although most experts agree it will be a drag on all economies of the major nations. For dairy producers, we would be cautious to sell milk at these prices. While we could continue to head lower in the short term, maybe even substantially, longer term fundamentals suggest a price recovery. Commercial users of dairy products as an input should consider the current weakness as an opportunity to cover input costs.

Note: Our offices will be closed on Monday in observance of President’s Day. Markets will be closed.

Have a great weekend!