02/07/2020

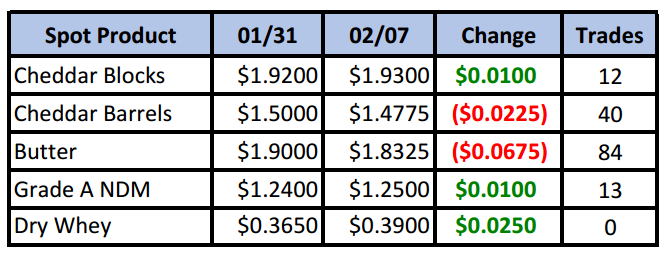

With the number of confirmed coronavirus cases tripling since last Fridaty and the death toll climbing, spot markets continued to drift lower in the beginning of the week. But block cheese eventually found a bid and settled the week a penny higher. Meanwhile, butter buyers decided the lower prices were a value and snapped up an eye-popping 84 loads this week. The barrel supply, however, still appears to be abundant, despite 40 loads exchanging hands. And the block/barrel spread reached a new record wide of 46¢ on Thursday, before retreating slightly to 45¼¢ on Friday.

Spot Market Recap

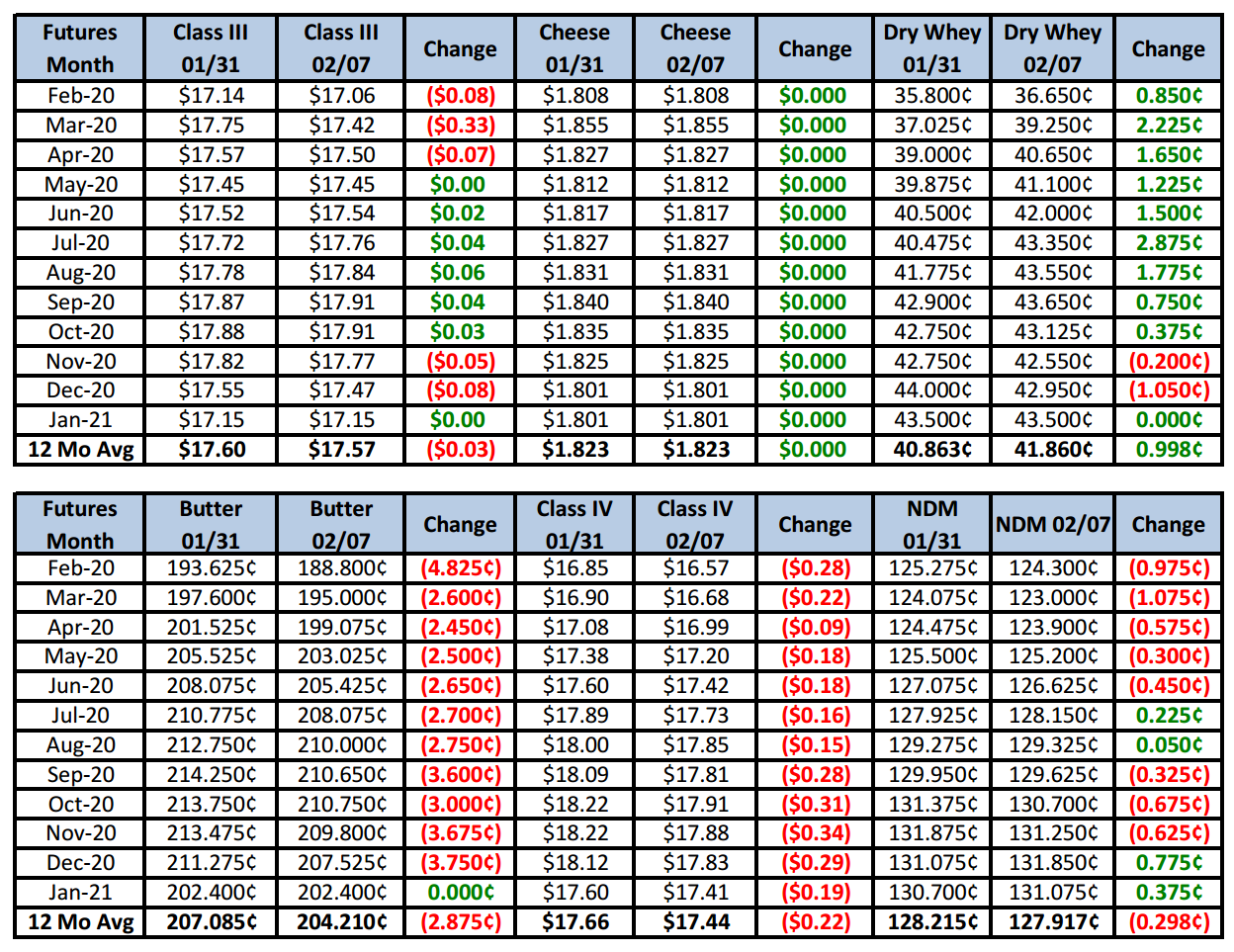

Futures Recap

The coronavirus continued to be the main market mover this week in everything from the stock market to commodities. However, news that scientists were having greater success in treatments helped reassure investors and most markets at least stopped their plummet. No doubt there will be some long-lasting economic consequences globally, but we’ll have to wait for preliminary numbers to see what affect it had on Q1. Meanwhile, milk production in the U.S. continues to climb seasonally and cream is abundant. Cheese output is strong but sales are good, keeping inventories from getting out of hand. The Dairy Products Report was released this week, with total cheese output in December up just 0.2% compared to Dec ’18, which was below expectations. Dec butter output was up a solid 4% over the prior year, however. Dry whey output jumped 7.5% with stocks on hand at the end of Dec up 2.1%. NDM output exceeded last Dec by a whopping 15.3%, but stocks on hand at the end of the month were 10.2% lighter than a year ago, indicating strong demand. That demand may have been a reason total U.S. dairy exports in Dec were up 17% vs. Dec ’18, according to the U.S. Dairy Export Council. WMP exports exploded, up 152%, while NDM/SMP exports increased 37%.

A shorter report this week as much of it was quiet, but bottom line is, spring flush is still in its early stages with unknown demand ahead. So far domestic interest has been good, but export interest could be hurt in the months ahead due to the epidemic. The solid price rally on Friday is technically supportive, perhaps indicating a near-term bottom has been put in, but it also could be a technical bounce before we head lower. 2nd half Class IIIs continue to hang in there and largely finished the week higher. That also is supportive longer term. Producers with price risk in the first half should look at a continued rally into next week to buy floor price protection. We just don’t know where this thing goes near term.

Have a great weekend!