10/11/2019

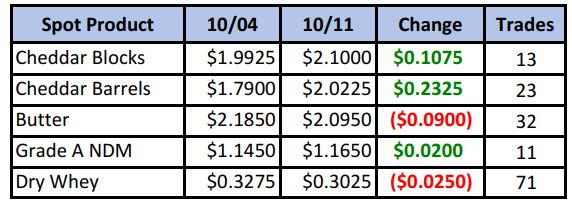

Barrel cheese was the star this week, gaining 23¼¢ and settling above $2/lb for the first time in 5 years. Block cheese was solidly higher as well, putting the block/barrel average at $2.06/lb and tightening the spread to just 7¾¢. That’s the narrowest it’s been since July.

Spot Market Recap

Futures Recap

While it was exciting to see barrel cheese jump above $2/lb this week, it does beg the question as to what is really behind this market. Fundamentals? Did the barrel supply tighten, the loosen, then tighten again to justify these moves? Not from what we’re hearing. On Aug 26th, spot barrels settled at $1.66½/lb, then rallied 27½¢ to close at $1.94/lb on Sep 16th, before plunging 32¾¢, settling at $1.61¼/lb and finally rallying 41¢ to reach $2.02¼/lb today; all told, a $1.01¼ move round-trip. The price swings were bigger each time, so who’s to say the next swing lower might be even stronger? Why these wild gyrations? We honestly don’t have an answer, other than it feels like big players moving the market because they can.

With the strength in spot cheese, Class III futures finished the week up big in the front months. But they kind of had to. The November contract begins pricing in a few days, and spot prices work out to about $19.65/cwt, not including basis, which probably puts it closer to $20 if not above. At $18.71 settlement today, it’s still trading a steep discount to spot, but we’ll see if spot can hold for a week or two and keep Nov futures headed higher, or if the market’s decision to trade at a discount to spot is justified by yet another barrel collapse.

The U.S. Dairy Export Council released August numbers this week. Total dairy exports were down 14% by volume, but up 3% to a 5-year high in value. Cheese exports were down 6% compared to last year, the fifth consecutive month of declines. However, part of that is due to a strong domestic market consuming available cheese. Total dairy exports accounted for the equivalent of 14.2% of U.S. milk production, down from 16.8% a year ago.

Highlights from Dairy Market News this week as as follows:

On the international front, milk output in Western Europe is declining seasonally, but looks to begin picking back up in the months ahead, at higher than year-ago levels. Cheese demand is very good and stocks are highly committed. Suppliers are demanding higher prices, but the potential for a 25% import tariff by the U.S., starting Oct 18th, could negatively impact their market. The U.S. is a major importer or EU cheese.

August milk production in Australia was down 5.9% YoY. Drought has left many pastures in poor condition. Expensive feed and the ongoing water shortage has resulted in active herd reductions, with stockyards packed with unwanted dairy cows. However, New Zealand has generally good pasture conditions and milk output is expected to above year-ago levels

Heading to the U.S., milk output in the Northeast is on the rise, whereas it continues to decline in the Southeast. Strong Class I sales are keeping milk out of manufacturing. In the Southeast especially, milk available for processing is very tight. In the Central region, milk output is mostly steady, with improved components. Spot loads are going for $0.75 to $1.25 over Class III. Milk continues to be transported to the Southeast, forcing cheesemakers to use more condensed skim and NDM to fortify their vats. Milk is still plentiful in the West, keeping most processors on heavy schedules.

Butter output across the U.S. is active as cream remains affordable and available. Stocks have been declining in some areas, but are plentiful in others. Dry whey offers and inventories are plentiful, keeping a buyer’s market in play. Prices continue to weaken. But NDM remains on a tear as even higher prices have not hurt demand yet. Inventories are being trimmed lower, while demand continues to be firm. Mexican buyers are very active. NDM plants in the NE are operating well below capacity, meaning only contracted customers are being serviced.

Cheese orders are steady in the NE, with some mozzarella producers stating they are mostly booked for the rest of 2019. Midwest cheesemakers report sales continue to be positive, with curd sales continuing at unexpected levels for this late in the season. Buyers are looking to secure and contract product in 2020, while process cheese manufacturers are reporting active buying interest. Western cheese sales could be better, but they are enough to keep inventories in check. Plants are running full and cheese stocks are heavy, but not burdensome.

Moving on to other news, on Friday the Trump administration announced a substantial Phase 1 deal with China, which includes $40-50 billion in agricultural product purchases. This is indeed good news, as the threat of ever more tariffs appears less likely now. That and supportive USDA crop revisions and ongoing wet weather put a strong bid in the grains. Feed costs once again look to be on the rise.

Overall, we still lean towards higher milk prices in the short to medium term. Strong domestic demand from a good economy, trade talk progress and flat milk production support our reasoning. We still remain concerned about the erratic barrel price behavior and what it will do going forward, but it’s beyond our control. Let it be a reminder though, that markets can and will change on a dime. Hedgers should have a plan and orders in place to be executed. Looking much further out, we’re wondering if profitable milk prices through the first half of 2020 could set up the second half for a fall. The current Jul-Dec 2020 average settled at $17.32 today. If you have a good handle on your inputs / feed costs that far out, you might want to consider selling up to 10-15% of your milk at $17.40 or higher, assuming that is a base price that is profitable for you. Just a thought.

Things are looking more positive up front, in our opinion. We would stick with PUT options Nov-Mar.

Have a great weekend!