08/09/2019

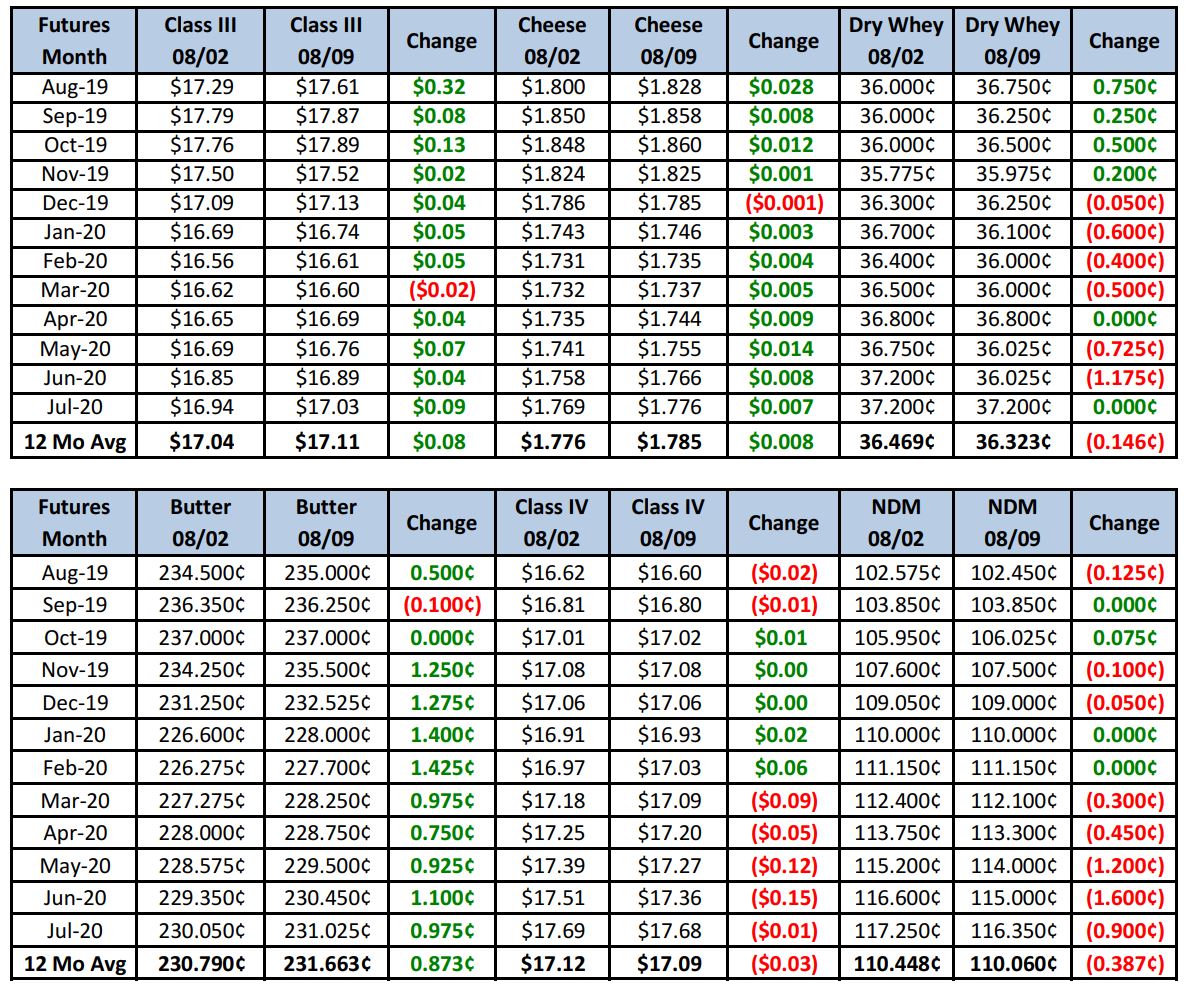

Spot cheese swung back to the positive this week, with blocks settling at a price not seen since Nov 2016. Barrels lagged behind, keeping the spread wide and the block/barrel average at $1.79.

Spot Market Recap

Futures Recap

Cheddar cheese fell 2% to a U.S. equivalent $1.74/lb. As Oceania gears up for their next milking season, many eyes will be watching for YoY production trends in both New Zealand and Australia.

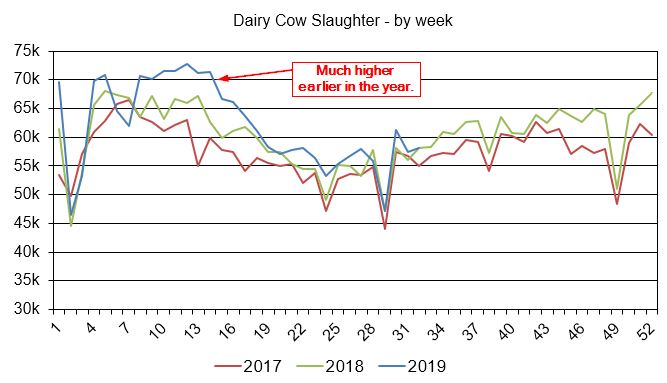

Dairy cow slaughter for the week ending 07/27 totaled 58,200 head, unchanged from a year ago. The sharp herd declines due to aggressive culling we saw earlier in the year appear to be over. Though we continue to hear about farm closures, they are scattered and now less common, indicating the size of the herd is most likely bottoming out. That doesn’t mean we will see a rapid rebuild, however. Replacement animals are not as available, nor are cash pockets every deep to enable expansion.

Dairy Market News updates this week continue to paint a mixed picture, with milk tightening up everywhere but the far West and Pacific Northwest. Output in the Northeast and Mid-Atlantic is down, with balancing plants no longer at capacity. Spot milk is tight and Class I sales are up. In the Southeast and Florida, schools are opening with a corresponding increase in Class I orders. Heat is still a factor, making cows uncomfortable. The region is in a milk deficit situation, drawing supplies from other states to meet demand. Cream and condensed skim prices are also on the rise, with buyers having to pay up for spot loads. Production is stable in the Midwest as temps have cooled, but components are still lower and milk is moving out of the region to the East. Cheese plants are no longer receiving spot offers as loads are priced at Class to $1.75 over. Small to mid-sized farms in the upper Midwest are still struggling with a feed shortage. Out West, California is at a low point in milk production, while milk demand has begun to increase in preparation for school openings. Output in Arizona is declining more than usual as monsoon humidity affects cow comfort. Milk from out-of-state is being imported to meet their needs. In New Mexico, milk production is down from last week, but Class I and III demand is up. Milk production remains strong in the Pacific Northwest, however, with plenty of milk for most processing needs. Many plants are running near full schedules. ID, UT and CO remain near peak levels, with manufacturers in those states unable to take on any more milk. Discounts of $4-5 under Class are common. Contacts are hoping the start of schools in the next two weeks will help relieve some of the pressure on supply.

Butter plants in the NE have reduced their churning schedules this week as there are fewer cream offers available. Plants in the Midwest were quiet this week due to the cost of shipping cream in, but hope to increase production next week with more affordable cream. Demand is only so-so, and bulk supplies are readily available. Buyers are currently on the sidelines due to recent price declines. August butter sales in the West have been sluggish at the retail level and buyers have been on the sidelines. Cream is available but churning has slowed as manufacturers would rather sell off the cream.

The dry whey market remains quiet across the country. Sales remain slow due to African Swine Flu and warehouses contain ample product. This is keeping prices from making any kind of rally. However, NDM prices in the East saw an uptick this week, as high temperatures are tightening the condensed skim supply and shortening drying output. It was quieter in the Central region, the drying there was also lighter and prices increased a bit at the top of the range. NDM sales are quiet in the West but the market is stable. Stocks are available, but not burdensome.

Cheese production in the Northeast is steady, but supplies are growing. Some contacts report weaker export demand, but on the domestic front, demand is stable, and some expect orders to pick up in the near future. Midwest cheesemakers, on the other hand, are contending with limited production rates due to milk loads heading East and spot loads pricing a premium to Class. Most are running just 5 or 6-day schedules. Specialty cheese is seeing demand that is stronger than average, while curd and barrel producers also report demand has been better than the two previous years. But, there is plenty of milk to make cheese in the West. Cheese sales have been decent, but not strong, so some manufacturers are heavily promoting cheese locally in hopes it increases sales. Inventories, however, remain generally under control.

With more school openings ahead and a milk situation that is tighter than it has been in a few years, we still have an upwards bias on prices. Block cheese hitting a multi-year high certainly bodes well for the near term. With some indications that barrel demand is picking up and the Midwest tight on milk, the current block/barrel spread of 14¾¢ could see barrels rally vs. blocks decline. It’s hard to say though as a lot of barrel production comes from the Pacific Northwest, where there is an excess of milk. Current spot components work out to about $17.35 Class III. Adding NDPRS basis brings it closer to $17.80 or so. If barrels can make a run higher, Sep and Oct Class III could once again see themselves above $18.00. For producers looking to sell milk,the $18.50 level looks like a good place to enter some orders for these months. Be prepared to make some sales in Nov and Dec as well, should those targets hit. We would still hold off selling much 2020 milk.

Have a great weekend!