08/02/2019

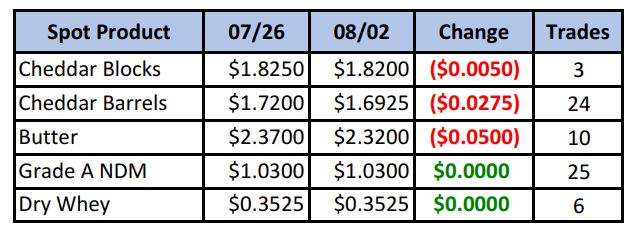

Spot cheese gave up some ground this week, settling at an average $1.76/lb. Blocks seem somewhat well supported with underlying bids in most sessions and just 3 trades, but barrel offers helped widen the spread on heavier volume of 24 trades. Spot butter was also weaker, hitting its lowest price since May.

Spot Market Recap

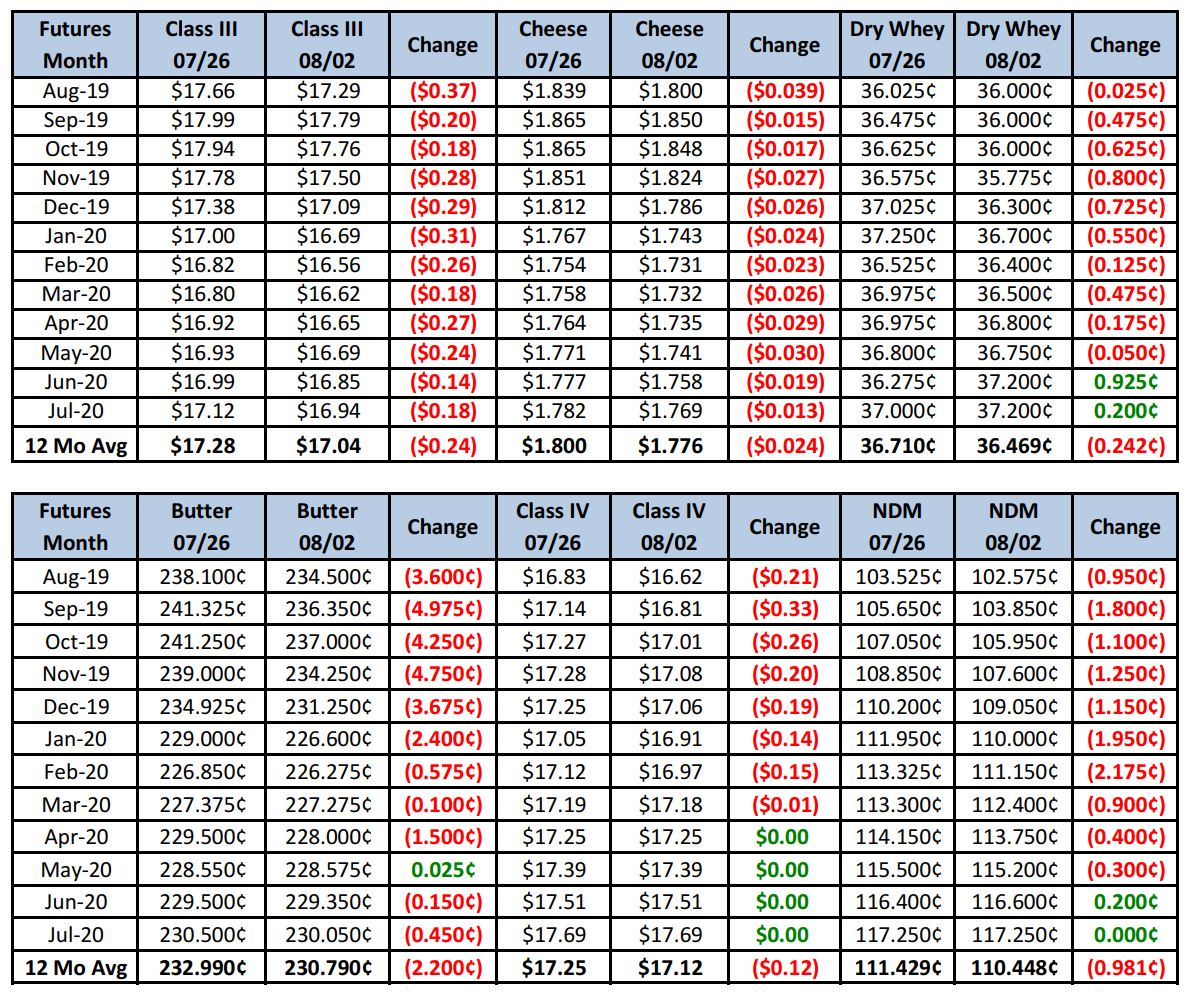

Futures Recap

Futures responded with heavy losses in most categories, though Friday saw a relief rally. It’s hard to say why the markets sold off this week, with fundamentals still mainly supportive.

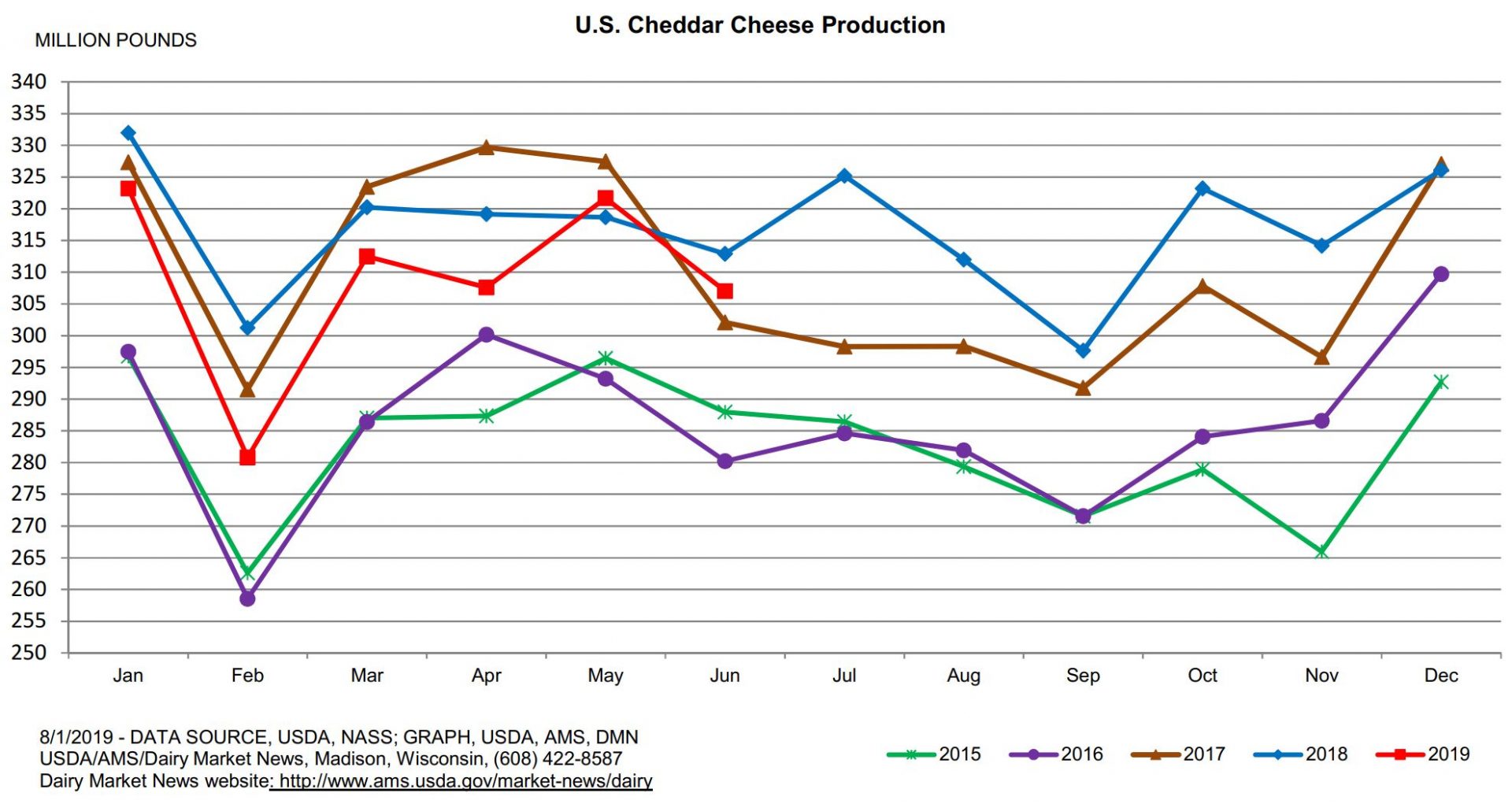

The Dairy Products Report was released with week with a mixed bag of data. On the positive side, cheddar cheese output during the month of June was down 1.9% compared to a year ago.

Weekly cold storage updates indicate cheese stocks at USDA-selected storage centers declined a strong 5% (4.6 million lbs) during the month of July. Combined with lower output in June, that should support cheese prices.

On the international front, Dairy Market News reports milk output in the EU was affected by the recent heat wave, but expectations are that it will only be a brief set back. Cheese sales are reported as strong, with inventories on the lighter side.

Have a great weekend!