08/16/2019

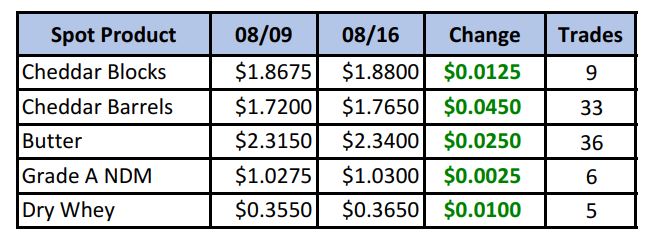

Dairy spot prices all settled higher on the week, with the block/barrel average setting a new multi-year high at $1.82/lb. We haven’t seen an average cheese price that high since November, 2016. Barrel and butter buyers got out their checkbooks, taking on a combined 69 loads. Dry whey continues to carve out a bottom, threatening the high at 37¢ from May. Prior to that, one has to go back to Feb for a higher whey price.

Spot Market Recap

Futures Recap

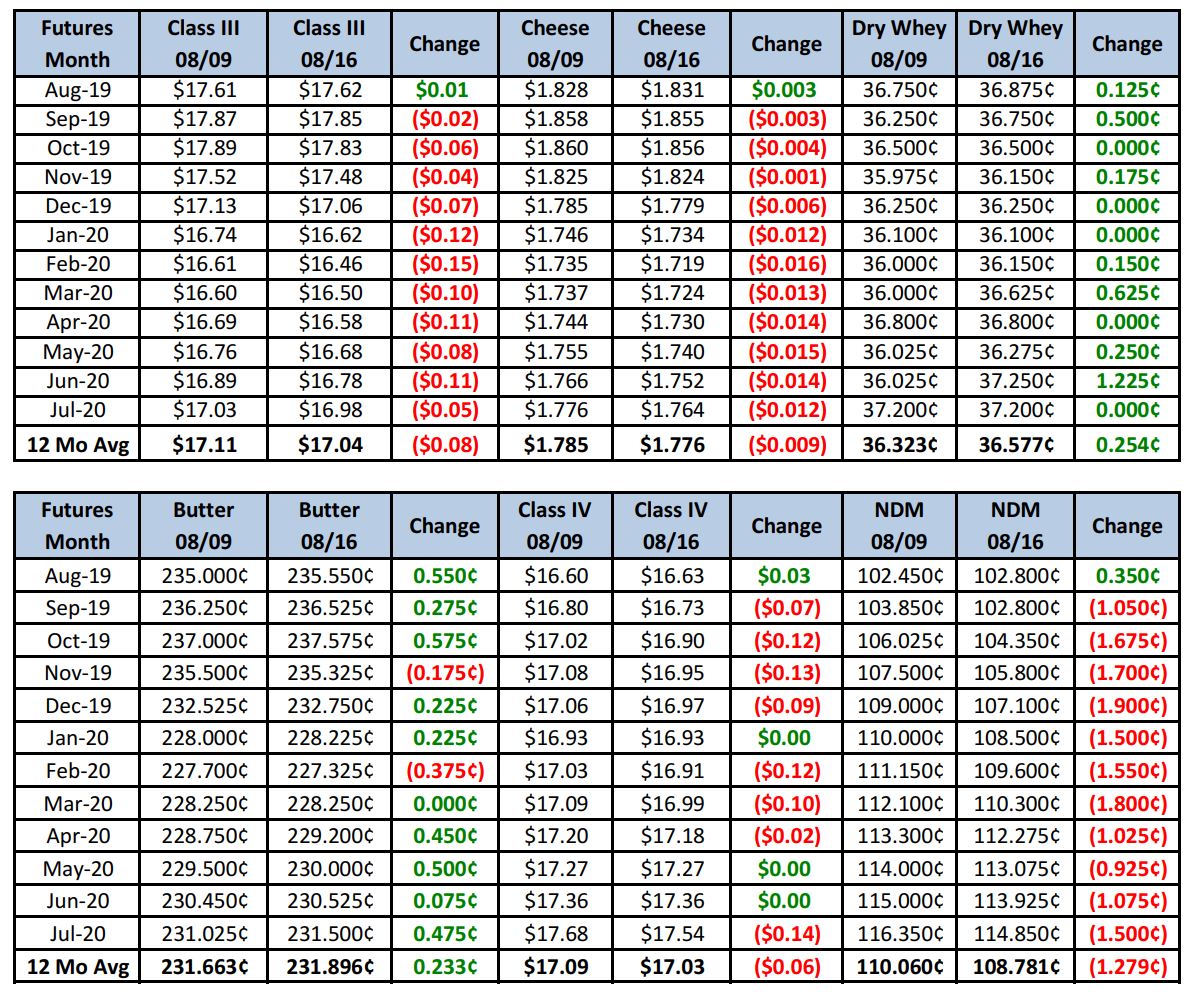

Despite the solid moves higher in spot prices, Class III, Class IV, Cheese and NDM futures were all mostly lower. Current spot prices plus Sep dry whey futures gives us a Class III price of about $17.70/cwt. Assuming the continued positive NDPSR basis, that puts Class III above $18/cwt, so futures are trading a discount to spot at the moment. There may be some anticipation out there of future weakness in spot, but it’s hard to say. Cheese feels well supported right now, with bidders moving the barrel price higher to narrow the spread a bit. Demand is currently strong and food service ordering is on the rise as schools reopen. There’s a bit more milk available, but nothing steeply discounted, and those loads are expected to disappear once more schools are fully in session. Cheese stocks seem to be in better balance than in year’s past.

Fluid output continues to decline seasonally, while milk piplines for the upcoming school year are being refilled. Balancing plants in the East are running under capacity or not at all. The Southeast remains a milk-deficit region and milk production is still declining. Milk output is basically in balance with demand in the Central region, and seasonally lower in the Southwest. Milk from other regions is being shipped to AZ to meet demands there. The Pacific Northwest remains the sole region with heavy output. Plants continue to run near capacity there.

Domestic demand for butter is good, but cheap imports are hurting sales of U.S.-sourced product. Prices are somewhat range-bound, but industry contacts are hopeful a fall pickup in demand will help move more product.

Dry whey sales across the U.S. are slow and export interest is weak. Inventories are growing and warehouses are beginning to fill.

On the international front, heat in the EU has put a damper on milk production. Cheese output in Germany is down and stocks are at a low point. Cheese demand is increasing, with some buyers trying to contract supplies for the first half of 2020. This is giving a firm tone to the market.

Oceania has begun it’s new milking season. Australia is starting out with very limited hay supplies. However, New Zealand is off to a strong start, with output catching some by surprise. With China being a major export destination, there is growing concern over the potential of a slowing economy.

With limited milk production growth over much of the globe, our long-term view is still for steady to higher prices. Cheese stocks at USDA-selected storage centers have fallen 3% over the first 12 days of August, with butter stocks declining 2%. The start of football season and school/university openings should limit the amount of milk available for manufacturing. Grains got a whole lot cheaper and there was room for technical correction, but if spot cheese makes new multi-year highs in the weeks ahead, we think Class III’s will reverse this week’s lower trend and move back up again. Producers should take advantage of lower feed prices and book some feed/ration needs. There is still much uncertainty over what yields will look like, despite USDA’s bearish numbers. Finally, ongoing trade negotiations, or lack thereof, could continue to put a drag on the Ag sector for some time, so higher prices are not a given. However, with the potential for higher prices in Q4, producers should look at call options to cover any upside risk they may have. Q4 settled at an average $17.45 today. The Q4 18.00 call options can be purchased at an average premium of 16¢ each.

Have a great weekend!