03/15/2019

Futures Recap

| Futures Month | Class III 03/08 | Class III 03/15 | Change | Cheese 03/08 | Cheese 03/15 | Change | Dry Whey 03/08 | Dry Whey 03/15 | Change |

| Mar-19 | $14.97 | $14.94 | ($0.03) | $1.531 | $1.533 | $0.002 | 40.700¢ | 40.025¢ | (0.675¢) |

| Apr-19 | $14.80 | $14.88 | $0.08 | $1.516 | $1.539 | $0.023 | 40.175¢ | 38.275¢ | (1.900¢) |

| May-19 | $15.03 | $15.11 | $0.08 | $1.539 | $1.561 | $0.022 | 40.150¢ | 38.500¢ | (1.650¢) |

| Jun-19 | $15.40 | $15.44 | $0.04 | $1.582 | $1.600 | $0.018 | 39.700¢ | 37.750¢ | (1.950¢) |

| Jul-19 | $15.89 | $15.92 | $0.03 | $1.632 | $1.645 | $0.013 | 39.525¢ | 38.200¢ | (1.325¢) |

| Aug-19 | $16.15 | $16.15 | $0.00 | $1.660 | $1.675 | $0.015 | 39.575¢ | 38.025¢ | (1.550¢) |

| Sep-19 | $16.39 | $16.39 | $0.00 | $1.681 | $1.686 | $0.005 | 39.600¢ | 38.500¢ | (1.100¢) |

| Oct-19 | $16.37 | $16.35 | ($0.02) | $1.685 | $1.690 | $0.005 | 39.550¢ | 39.000¢ | (0.550¢) |

| Nov-19 | $16.25 | $16.24 | ($0.01) | $1.680 | $1.676 | ($0.004) | 39.025¢ | 39.000¢ | (0.025¢) |

| Dec-19 | $16.20 | $16.10 | ($0.10) | $1.675 | $1.666 | ($0.009) | 38.775¢ | 38.925¢ | 0.150¢ |

| Jan-20 | $15.85 | $15.81 | ($0.04) | $1.656 | $1.654 | ($0.002) | 37.175¢ | 37.375¢ | 0.200¢ |

| Feb-20 | $15.75 | $15.75 | $0.00 | $1.660 | $1.657 | ($0.003) | 36.750¢ | 38.000¢ | 1.250¢ |

| 12 Mo Avg | $15.75 | $15.76 | $0.00 | $1.625 | $1.632 | $0.007 | 39.225¢ | 38.465¢ | (0.760¢) |

| Futures Month | Butter 03/08 | Butter 03/15 | Change | Class IV 03/08 | Class IV 03/15 | Change | NDM 03/08 | NDM 03/15 | Change |

| Mar-19 | 227.525¢ | 227.525¢ | 0.000¢ | $15.79 | $15.79 | $0.00 | 97.225¢ | 96.825¢ | (0.400¢) |

| Apr-19 | 228.200¢ | 228.200¢ | 0.000¢ | $15.92 | $15.88 | ($0.04) | 97.025¢ | 97.100¢ | 0.075¢ |

| May-19 | 230.575¢ | 230.725¢ | 0.150¢ | $16.08 | $15.96 | ($0.12) | 98.725¢ | 97.975¢ | (0.750¢) |

| Jun-19 | 231.500¢ | 231.775¢ | 0.275¢ | $16.33 | $16.27 | ($0.06) | 100.850¢ | 100.250¢ | (0.600¢) |

| Jul-19 | 232.000¢ | 232.775¢ | 0.775¢ | $16.49 | $16.48 | ($0.01) | 102.925¢ | 102.000¢ | (0.925¢) |

| Aug-19 | 233.000¢ | 233.000¢ | 0.000¢ | $16.71 | $16.64 | ($0.07) | 104.525¢ | 104.250¢ | (0.275¢) |

| Sep-19 | 234.000¢ | 232.925¢ | (1.075¢) | $16.77 | $16.75 | ($0.02) | 105.125¢ | 105.000¢ | (0.125¢) |

| Oct-19 | 233.000¢ | 231.800¢ | (1.200¢) | $16.85 | $16.72 | ($0.13) | 106.000¢ | 106.025¢ | 0.025¢ |

| Nov-19 | 232.000¢ | 231.000¢ | (1.000¢) | $16.88 | $16.75 | ($0.13) | 107.000¢ | 106.800¢ | (0.200¢) |

| Dec-19 | 229.750¢ | 227.525¢ | (2.225¢) | $16.75 | $16.64 | ($0.11) | 107.500¢ | 106.900¢ | (0.600¢) |

| Jan-20 | 225.000¢ | 225.000¢ | 0.000¢ | $16.55 | $16.55 | $0.00 | 109.100¢ | 108.425¢ | (0.675¢) |

| Feb-20 | 222.525¢ | 222.525¢ | 0.000¢ | $16.55 | $16.55 | $0.00 | 109.500¢ | 109.250¢ | (0.250¢) |

| 12 Mo Avg | 229.923¢ | 229.565¢ | (0.358¢) | $16.47 | $16.42 | ($0.06) | 103.792¢ | 103.400¢ | (0.392¢) |

Spot Market Recap

| Spot Product | 3/8 | 3/15 | Change |

| Cheddar Blocks | $1.5350 | $1.5600 | $0.0250 |

| Cheddar Barrels | $1.3650 | $1.4925 | $0.1275 |

| Butter | $2.2675 | $2.2800 | $0.0125 |

| Grade A NDM | $0.9750 | $0.9675 | ($0.0075) |

| Dry Whey | $0.3400 | $0.3200 | ($0.0200) |

Spot Market Trade Volume

Fluid Milk Output

Balancing plants in the Northeast remain at or near capacity this week, though output is lower than expected in some parts of the region. With Class I sales still slowed by spring break, there is still plenty of milk available for manufacturers, however. Milk output in the Mid-Atlantic is unchanged from a week ago, with a few operations under capacity. Nearly the same is true in the Southeast, where milk receipts to manufacturers is about unchanged. Florida is nearly at its peak, with warmer weather coming. Winter weather is finally showing signs of releasing its grip in the Upper-Midwest. Warmer temps are expected to improve cow comfort and thus milk production. In the mean time, farm closures continue at a steady pace. In the South-Central area, milk output is inching higher. More milk is moving into processing/drying, and spot loads of milk were trending more towards $2 under Class. Heading west, California milk output is trending seasonally higher, with processors getting sufficient volumes to meet demand. Expectations are for Class IV demand to increase in the near future as spring holiday preparations begin. Arizona saw a decline in milk output due to heavy rains early in the week. Total output remains below year ago levels. Favorable weather across much of New Mexico is helping improve milk production. Class I requests are down, but milk sales are up. Farmers in the Pacific Northwest are still dealing with herd issues related to the blizzard that hit last month. Some cows have been slow to recover and others have had to be culled. Hospital pens are full in some instances. Several large operations have sold their herds, reducing milk receipts to some processing plants. Overall though, there is plenty of milk for most operations.

Butter

Cream demand has declined slightly in the East. Loads are accessible and several spot offers are available. Some butter manufacturers have pulled back a bit, but inventories are still stable to growing. Churning remains very active in the Midwest, as cream supplies continue to roll in, some from the West. Manufacturers continue to add to their spring/fall inventories. In the southern part of the region. churning has slowed a bit. Interest has improved for both salted and unsalted varieties. In the West, cream supplies are described as solid, but not overbearing. Production of holiday items is picking up, while some bulk butter buyers are not easily finding any discounted pricing.

Dry Whey

The market is still soft in the Eastern region as buyers continue to hold off on purchases. Customer interest is described as lackluster. Central region prices continued to decline this week as producers continue to face exporting hurdles. More whey from the West is stuck in the country, putting a drag on prices. However, with lower cheese output in the Midwest, local trades are holding relatively firm. Western whey prices were lower this week as well, in light of the aforementioned issue. Some industry contacts believe buyers in Southeast Asia and Mexico have enough whey on hand and are only interested in discounted loads. Inventories are gradually increasing locally.

Nonfat Dry Milk

NDM market conditions continue to soften in the East. Spot loads are available but buyers aren’t making purchases. Prices decreased this week as a few manufacturers began selling on the spot market. Output is steady and inventories continue to inch higher. Central NDM prices were under pressure this week as increased availability, steady output and buyer hesitancy all helped bring prices lower. The weaker bias is keeping buyers on the sidelines. In the West, few shipments are heading to Mexico as they are currently in their spring flush and have adequate supplies. Exports to China are almost zero due to tariffs, while the stronger U.S. dollar is making export products costlier. Market contacts are hopeful domestic demand will be boosted via baking season. Stocks are flat to increasing slightly.

Cheese

Cheese makers in the Northeast are receiving ample volumes of milk to keep both cheddar and Italian lines on busy schedules. Supplies are mainly stable, but there are reports of increasing cheese orders from numerous customers. In the Midwest, cheese orders remain quiet, but curd and barrel producers report spot interest is on the rise. Local contacts report inventories are manageable, due to plants limiting their schedules so far in 2019. There is an expectation that production lines will increase as demand picks up into spring. The cheese market tone is described as “bullish” this week, with the barrel price closing the gap with blocks. Western cheese output is active as increasing milk production makes its way to the vat. Cheese inventories are heavy. In order to balance supplies, more cheese is being put into aging programs. In addition, strong demand is reported at the retail level, along with a few export channels.

International

Milk production in Germany and France the past two weeks has been higher than year ago levels, according to Dairy Market News. Conditions are favorable for continued strong milk production in the coming weeks. EU butter prices weakened due to a decline in demand and balanced stock levels. Domestic cheese sales are good and export interest is strong. Many processors have sold out their cheese in advance of producing it.

In Oceania, many New Zealand producers have transitioned from two milkings a day down to one, as the season winds down. Butter prices have strengthened and the market tone is firm. Demand is very good, while butter output is declining as the current milk production season ends. Buyers know this, and are thus more motivated to make purchases. Butter stocks are tightening. Cheddar cheese stocks are also getting tight as buyers try to close deals. Prices increased this week to a U.S. – equivalent $1.79/lb. Supplies of both SMP and WMP have suddenly gotten more scarce than expected, which has sparked buying interest and firmer prices.

Commentary

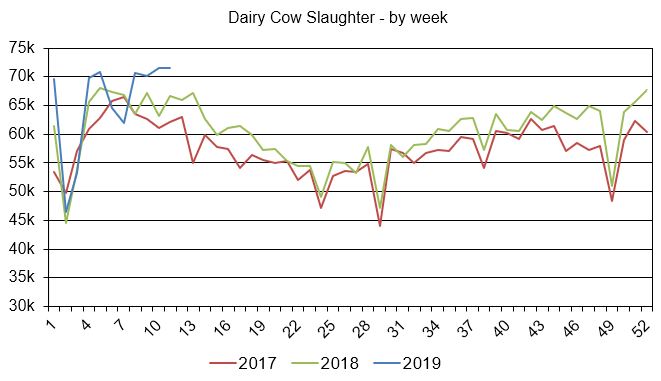

Weekly dairy cow slaughter numbers continue to impress. 71,500 head were removed from the herd for the week ending 03/02, up 7.2% vs. the year prior. In only the first 11 weeks, an additional 32,000 head have been culled compared to last year.

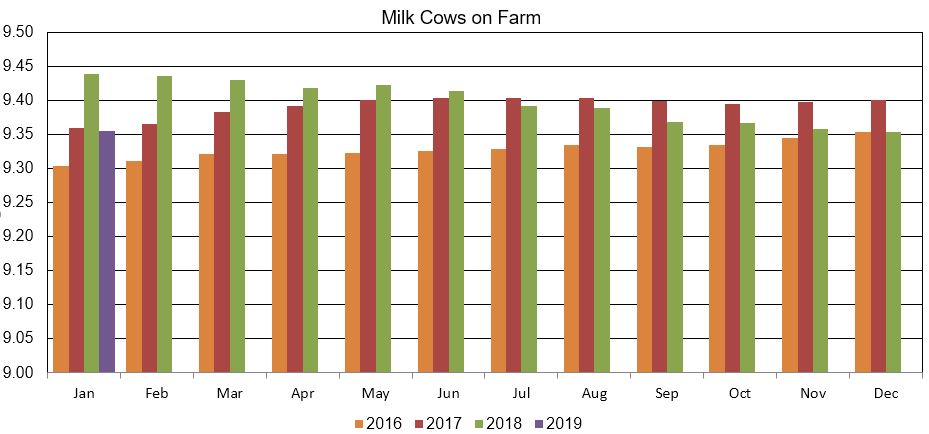

USDA released another Milk Production Report this week. It was a mixed bag. January milk production was up a higher-than-expected 0.9% vs. a year ago, and cow numbers increased 2,000 head from December. But the herd size at 9.438 million head was the lowest for the month since 2016.

On Thursday the Dairy Products Report was released. January butter output exceeded expectations with a 4.2% increase over last year. American cheese output was up a more modest 1.2% while total cheese output increased just 0.4%. Dry whey output fell 10.1% vs. Jan ’18, with manufacturers’ ending stocks down 12% at the end of the month. This helps explain some of the recent price strength in spot dry whey during the first part of the year. NDM output jumped 7.7% but manufacturers’ ending stocks were down 7.6% at the end of the month.

Demand and supply are slowly coming in to balance. Between more aggressive culling in the U.S., a tightening milk supply in Oceania and improving demand, the stage is getting set for firmer prices. It may already be starting to happen. Spot cheese had a strong week, with the block/barrel average settling at $1.53/lb, the highest in six months. Interest for barrels is improved, helping the now typical wide spread narrow to just 6¾¢. Over the first 11 days of March, cheese stocks at USDA-selected storage centers fell an anti-seasonal 2% (1.7 million lbs). Typically stocks are building at this time of year. With the higher spot cheese prices, Class III futures finished the week higher. But Friday left us a bit perplexed as the market sold off in the afternoon. Current spot prices (using April dry whey) works out to about $15.00/cwt. Adding the NDPSR survey basis puts it closer to $15.40-15.50. With April Class beginning its calculation soon, its settlement today at $14.88 leaves it at a significant discount. Perhaps the 12¾¢ jump in the barrel price this week is all smoke and mirrors; who knows? But spot cheese prices will need to start coming down in order for futures to stay where they are. We’re hearing blocks are a little on the snug side, so downside seems somewhat limited there. And while we haven’t hit peak production yet in the U.S., some of the southern and western regions of the country are near or at peak output now. As the weather warms over the coming weeks in these areas, milk and components will begin to drop. In addition to weather, a determining factor in where prices go from here will be the EU. They had been struggling with weather and feed issues in Q4, but output has started to climb again. That could put a damper on things. Overall, we still believe the lowest prices of 2019 are already behind us in the Jan and Feb settlements. Finally, on a macro level, commodities as an asset class are moving higher. They are historically cheap compared to the stock market, which is once again near all-time highs. Money is flowing back in. Grains are finding a bid. Soybean meal rallied nearly $10/ton this week. The CRB Index is a basket portfolio of all the major commodities, from energy to agriculture to precious metals to building materials, etc. After falling all of 2018, it is now on the rise in 2019.

Producers would be wise to look at covering upside risks to milk already locked in with plants or sold on the exchange.

Have a great weekend!