2/17/2024

The NFL season is done and behind us. Typically the cheese buyers slow at this point as the next big demand bump is a couple of months away. However end user inventories are on the lighter side. The futures market has rallied some and prices are getting closer to cost of production. This year it is going to come down to consumer demand. Cheese production is likely to be lower then previous years so if demand picks up cheese supply will tighten.

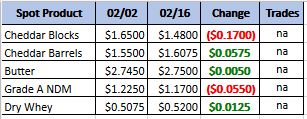

Weekly Spot Prices

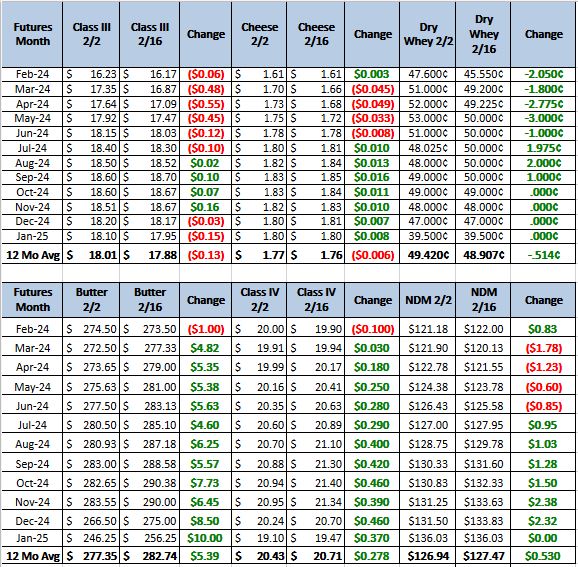

Weekly Future Prices

Cheese: Cheese plant managers relay seasonally steady production schedules in the East region. Contacts share block cheese inventories are growing. Cheese demand in the Central region is noted to be seasonally quiet. Contacts in the Midwest are focusing on building inventories for spring demand. Milk availability is tighter than predicted. During week seven of last year spot milk prices were $10- to $2- under Class III whereas below-Class prices for spot milk loads have yet to be reported this month. Some end users report tight milk availability in the West, while others suggest Class III spot loads are generally available when needed. Plant managers share steady

cheese production schedules. Spot cheese inventories are noted to be tighter than in recent weeks in the West. A block/barrel inversion has been in place on the CME since last Friday (USDA Cheese Highlights)

Butter: Retail demand is steady throughout the country. Food service demand is strong in the East region and steady in all other regions. Cream loads are readily available for butter makers to utilize throughout most of the country. Some butter plant contacts expect cream offers to be abundant for the remainder of the month. Butter manufacturers are running busy production schedules to build for anticipated spring demands. Stakeholders note unsalted butter availability is tight. Distributors relay inquiries from international customers have been more frequent recently. Bulk butter overages range from 4 to 15 cents above market, across all regions. (USDA Butter Highlights)

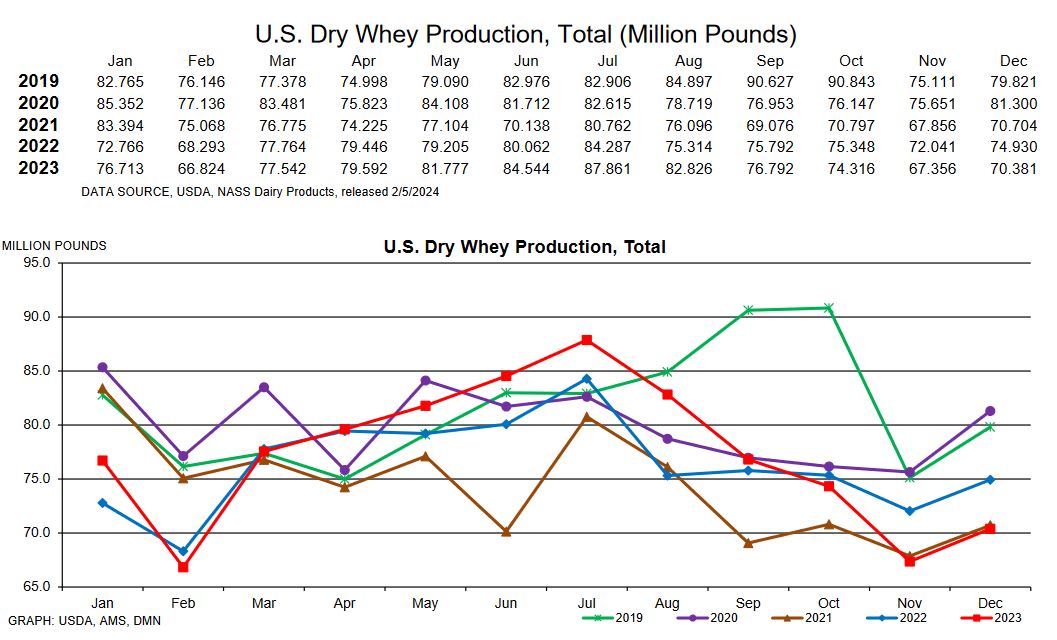

Dry Whey: Prices moved higher across all facets of the range and mostly price series in the West. Stakeholders note steady to stronger domestic demand. Export demand is moderate. Some manufacturers and distributors relay tight near-term availability for spot load buyers. A few producers anticipate tight bleached whey availability for spot load buyers through Q1. Plenty of liquid whey is being made by cheese makers for steady production schedules. However, some manufacturers continue to focus processing schedules on whey

protein concentrates, which have had a strong market in recent months. Contacts’ near-term sentiments vary from neutral to bullish. (USDA Dry Whey)

Worries about demand from the consumer has slowed the class 3 rally as the market lost some of its gains this week. Whey is starting to be a bright spot with some of the lowest production in the last 5 years. Every penny higher on whey is 6 cents higher on class 3. That is one of the factors that sent 2022 prices so high. With that said the updates this week indicate that demand has been slowing for cheese and there may be some down side before we see a sustained rally. Recommendation, buy puts up front and sell puts further out to pay for them. Give us a call for more personalized recommendations. We are closed Monday for Presidents Day, we will be back open Tuesday.